Regulated vs. unregulated investment platforms: what every investor should know

When choosing an investment platform, most investors compare returns.

10%, 12% or 15%?

But there is another question that deserves just as much attention:

Who is supervising the platform behind those returns?

Two platforms may offer similar investment opportunities, yet operate under completely different standards. One may be regulated by a financial authority, while the other follows only its own internal policies.

Understanding that difference can help you make a more informed investment decision.

What does “a regulated platform” actually mean?

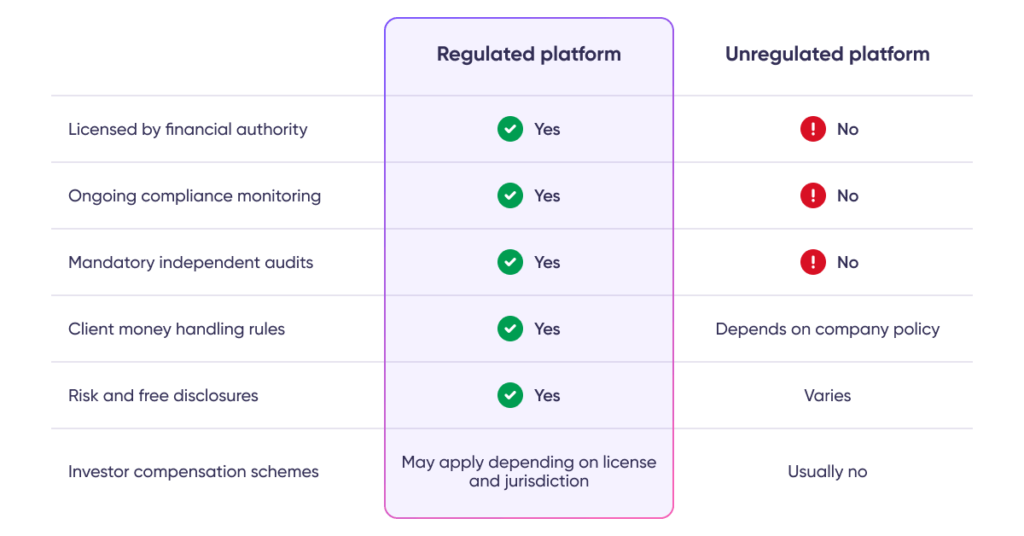

A regulated investment platform operates under the supervision of a financial authority.

To receive and keep its license the company must follow strict rules covering areas such as:

- protecting client funds,

- preventing money laundering and financial crime,

- verifying investor identity,

- maintaining operational and financial controls,

- reporting regularly to regulators.

Regulation is not a one-time approval. Licensed firms are continuously supervised and must demonstrate that they continue meeting regulatory standards.

What regulation means in practice

Here are some of the protections investors typically benefit from on a regulated platform.

Client money is handled separately

Regulated investment firms are generally required to keep client money separate from their own operational funds.

Why it matters: If the platform experiences financial difficulties, there are legal rules governing how client assets should be handled instead of relying solely on the company’s internal policies.

Greater transparency

Regulated platforms must provide clear information about investment risks, fees and how they operate.

Why it matters: You can make investment decisions based on transparent information instead of marketing claims alone.

Ongoing supervision

Licensed firms remain under the supervision of financial authorities and must continue meeting regulatory requirements.

Why it matters: The platform cannot simply create or change its own rules without oversight.

Independent controls

Regulated businesses are expected to maintain compliance procedures, internal controls and risk management processes. Many are also subject to independent audits.

Why it matters: Multiple layers of oversight reduce the likelihood of operational mistakes or misconduct going unnoticed.

Investor protection mechanisms

Depending on the jurisdiction and the firm’s license, regulated investment platforms may participate in statutory investor compensation schemes.

Why it matters: These schemes are not designed to protect against investment losses or guarantee returns. However, they may provide protection in situations defined by law, such as when a licensed investment firm cannot return client assets.

The exact protections depend on the regulator, the firm’s license and the country where it operates. That is why it is always worth understanding how a platform is regulated before investing.

Regulated vs. unregulated platforms at a glance

An unregulated platform is not necessarily unsafe. Many operate responsibly.

The difference is that investors rely primarily on the company’s own standards rather than an external regulatory framework.

Why this matters for investors

Regulation cannot eliminate investment risk or guarantee positive returns.

Markets can change. Borrowers can default. Investments can lose value.

What regulation does provide is confidence that the platform itself operates within a framework of clear rules, ongoing supervision and accountability.

That allows investors to focus on evaluating investment opportunities rather than questioning how the platform itself is managed.

What regulation means at Debitum

Debitum is a regulated investment platform that operates under European Union financial regulations such as MiFID II. Debitum is authorized and supervised by the Latvijas Banka.

For investors, this means the platform follows established regulatory requirements throughout the investment process, including:

- Investor identity verification (IDV) and Know Your Customer (KYC) review,

- Anti-Money Laundering (AML) compliance,

- Suitability Assessment Questionnaire (SAQ),

- Additional verification to increase deposit limit,

- Ongoing regulatory oversight,

- Operational controls and compliance monitoring.

These processes are part of every investor’s onboarding journey. While they may take a little extra time, they help protect both investors and the integrity of the platform.

The bottom line

Every investment carries risk, whether the platform is regulated or not.

The difference is that regulation creates a framework of accountability, transparency and oversight that helps protect investors throughout their investment journey.

When comparing investment platforms, do not look only at the advertised return.

Also ask:

- Who supervises the platform?

- What rules does it follow?

- How are investors protected?

- How transparent is its operation?

Those answers may become just as important as the interest rate itself.

This is a marketing communication and should not be interpreted as investment research, advice, or an endorsement to invest. The historical performance of financial instruments is not indicative of future outcomes. Investing involves risks; the value of investments may fall as well as rise. Be sure to assess your knowledge, experience, financial situation, and investment goals before investing.