Tag: Bondora default rate

What are the risks of investing in short term loans on P2P/P2B platforms

What are the risks of investing in short term loans on P2P/P2B platforms

Risk/reward ratio is at the heart of each type of investment. A rule of thumb remains the same, the higher the risk, the greater the reward, the lower the risk, the lower the reward. Institutional investors seek the type of investment options that offer the highest return with the lowest risk. Risks may vary and some investments may have so many of them that it may be unwise to even consider them. A relatively new way to invest is P2P/P2B platforms. Despite criticized by the mainstream these alternative finance platforms have gained more and more popularity in recent years. Let us look and see how risky they are and how those risks can be reduced, and profit increased.

Not all alternative investment platforms are created equal

Even within the alternative lending/investment platforms, there are significant differences that may impact your risk/reward ratio. Some platforms offer personal loans to invest in, other real estate projects, others such as Debitum Network, focus on investing in short term loans for businesses (invoice financing and business loans).

Obviously, the percentage of defaults on the platforms vary greatly too. One of the leaders in the alternative lending/investment market Zopa has around 0.6% of defaulted loans, while another prominent player in the field (according to independent research) may have around 30%. In the 9 month period of existence, there has not been a single defaulted loan on Debitum Network platform. Commercial banks typically have around 1%-2% of defaulted loans.

Online platforms that offer users to invest in personal loans or payday loans may have high-interest rates: 15%-35%. However, taking into account that on some of the platforms 1 out of 5 investors may lose money, the average net return on them will go down to around 10%. It is obvious that the aspect of safety should be taken more seriously while talking about investments and returns on the platforms.

What are the risks and how can they be reduced?

A borrower may default on its’ obligations to pay off the loan and it is the biggest risk for an investor who has put money into such an asset. The invested money can be lost and never repaid.

To avoid such a scenario, a lot of (not all) platforms have implemented a buyback guarantee, which basically means that if the borrower is late with his repayments by more than 30-90 days (60-90 on Debitum Network platform. The actual number depends on the loan originator that issued a specific loan), the broker/loan originator will have to buy back the specific loan with the outstanding principal and interest. So, if a specific loan defaults, the investors’ risk is reduced to the minimum.

Another risk, that has much less likely probability of happening is when the loan originator goes default. This happens from time to time. When Eurocent loan originator (on Mintos platform) went broke, investors that invested in the assets of the loan originator, lost their money. Despite the fact, Mintos is doing everything in their power, there is little hope for investors to regain their invested balance and the interest earned on it. That’s why the buyback guarantee is as good as the loan originator that provides it. A proper selection and thorough screening of loan originators are necessary before onboarding them on an investment platform. Debitum Network selects loan originators carefully as well as their assets that are placed on our platform for investment. Due diligence parties as well as risk assessing companies do thorough risk rating defining the probability of default of the borrowing company and the loans uploaded on our platform.

Extra measures to ensure the safety of investors’ funds

Debitum Network solely focuses on loans for businesses as businesses have a higher chance of repaying the loan than private individuals. Businesses will unlikely borrow at such high-interest rates that some P2P lending platforms offer. Offering extra guarantees and taking extra risks borrowing at 20% is something that SMEs will hardly ever do. Private individuals that may take a loan for a car or a home will have to undertake very high risks that they are not very skilled at handling, thus increasing the likelihood of a potential default and consequently loss of the investors’’ money in the given loan.

P2P platforms similarly use other protection methods for investors funds. Collateral from borrowers or real estate can serve as a guarantee that in case of default, it will be used to repay the investors. However, even sold the collateral may not be enough to compensate the entire invested amount, to say nothing of the outstanding interest. Real estate in the same fashion can be an illiquid asset and it may take a lot of time to sell it to repay the investors (with no assurance that they will get the full invested amount back or due interest). In that respect, a buyback guarantee is a far superior method for protecting investors’ funds and profits and the loan originator (in case of default of a specific loan) buys back both outstanding principal and interest.

Personal guarantees from the owners of the borrowing businesses are yet another protective measure to ensure the safety of investors funds. By the guarantee, the owner of the business guarantees, that if the business fails to pay off the loan, he/they will pay it off. It is typically not tied to a specific asset. In the event of non-payment, the lender can go after the personal assets of the guarantor.

Some platforms employ third parties to do risk assessment and due diligence services. This ensures transparency and quality of services as no conflict of interest is involved. Our own Debitum Network takes these service providers from countries where borrowing parties reside and thus, risk assessment or due diligence services are more accurate due to the specialization of the party doing the services and the knowledge of the local market.

Want to invest in low-risk assets in Debitum Network?

On Debitum Network we apply all available security measures to ensure investors funds’ are safe. Last week we onboarded a new loan originator Aforti Finance, who is the leading non-bank lender in the Polish market. This enables us to provide new investment opportunities, flexibility, and options to choose from for our customers. The first assets from the loan originator have already been uploaded on Debitum Network platform and you can start investing in them. They have attractive interest rates and a buyback guarantee. Check them out!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What if the repayment is late?

What if the repayment is late?

Delayed and non-performing loans is an inevitability even on the safest p2p lending platforms. If an investor has a lot of loans in his portfolio, he will occasionally have a defaulted or delayed loan. Commercial banks typically have 1-2% percent of defaulted loans. Percentages with different loan originators or p2p platforms differ greatly: from 0.6% on Zopa to around 30% on Bondora. This is precisely the reason why investors must be careful while choosing a p2p platform to invest with.

Borrower’s default may be the biggest risk to an investor on a p2p platform. A delayed repayment on a loan can also be a cause for concern. Invested money may eventually be lost, and waiting for the positive outcome (for the borrower to repay the loan) can be quite a psychological drag as an uncertainty over the security of funds can erode investor’s trust in a given loan originator or a platform.

Buyback as a form of protection

Most of the p2p platforms or their brokers have implemented a buyback guarantee (the feature has been added on Debitum Network recently), which means that if any given loan is late by a specific number of days (typically from 30 to 120) the loan originator is obligated to buy back the loan and in most cases payback the accrued interest too (platforms differ on percentages of principal as well as interest they return). On Debitum Network, the investor is repaid outstanding principal and outstanding interest, but not an outstanding penalty (in case the repayment is late more than 90 days). Thus, if the investor is protected by a buyback guarantee a defaulted loan will not do significant damage to his overall returns. Additionally, loans placed on Debitum Network often have a guarantee from shareholders or are backed by assets (collateral). This strengthens the fact that invested money will be returned as the loan originator (broker) will have assets to sell and have the means to cover the losses incurred by investors from a specific loan.

Should you be worried if a loan is ‘Late’ on Debitum Network platform

As has been said, any given loan can be delayed. If you are an investor, this is a sign for a concern. However, nothing to be worried yet. Firstly, we differentiate loans that are under 15 days late. They fall under the ‘Grace period’ and no penalty is placed on the borrower, just the outstanding principal and interest.

‘Late’ (after Grace period) is a period when a penalty is calculated in addition to interest rate for each day being late (excluding Grace period), thus increasing the potential return for the investor, but also causing some worry as to “what if the loan will default?”

If you see a sign ‘Late’ under the Status section of our platform, there is no need to be concerned as our partner brokers have provided necessary buyback guarantees for investors.

However, let us go through the timeline of the lending process on our platform from the issuance of a loan till the repayment or the status of being ‘Late’, so that you may understand better what happens in each stage, how you are protected and whether you need to be worried.

This is the timeline of any loan uploaded on Debitum Network platform:

An example of an asset in ‘Grace period’

As has been said, the borrower usually has 15 days of ‘Grace period’ if he is overdue with the payment of the loan after the repayment date. He still has to pay back the principal and interest but does not get a penalty for being late.

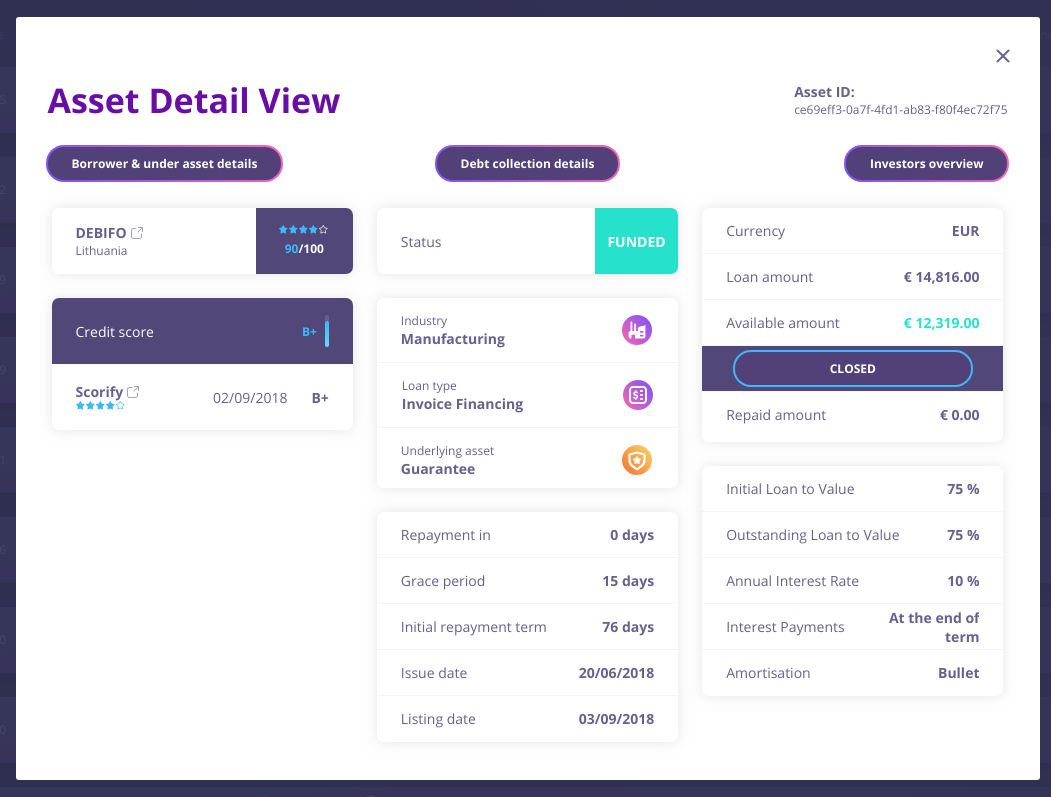

An investor can easily check the status of any given loan he has invested in on our platform. Having clicked ‘My investments’ button will load the list of all his/her current investments. One may spot that some of the loans are late, but still under grace period (typically 15 days). Below is the example of one. It has been in grace period for 10 days and has 5 days left, till the status changes to ‘Late’ (if not repaid by the end of 5 days). This borrower will have to pay both principal and interest, but no penalty yet. Having clicked ‘View’ button, an ‘Asset Detail View’ will pop up, where one can find more info about the loan and the borrower, how strong he is, whether he has borrowed before, borrower’s revenue amounts, years in business, or who the final payer for invoices is. This info should give more confidence for the investor as the loans on our platform are carefully handpicked and borrowers carefully assessed by loan originators. One should also remember that some industries undergo seasonality effect, where business generates less income and, therefore, some invoices may be paid slightly later. We will look at the ‘Asset Detail View’ window in our next example.

An example of an asset that is ‘Late’

Loans that have the status of ‘Late’ can be analyzed in the same fashion. An investor can click ‘My investments’ button and all the assets he has invested in will show up. Under the column ‘Status’ the investor can see which of the loans that he has invested in are ‘Late’. Below is an example of an asset, which is ‘Late’. The basic info about the asset one can find is: the industry, the broker, how many days it is late, what kind of loan it is, guarantee, invested and repaid amount, annual interest rate, credit score, outstanding interest, penalty increment, status, and ‘View’ icon.

More detailed info about the loan can be found by clicking ‘View’ button. This opens an ‘Asset Detail View’ window. There you will find such info as: when the asset is going to be repaid, grace period, initial repayment term, issue date, listing date, when interest is paid, amortization and more importantly ‘Borrower and Under Asset Details’. The window has more details about specifics of the industry borrower is in, how many years and what kind of guarantees are provided. Sometimes, a loan originator can provide more detail financial summary of the borrowers activity (attached document), which proves the ability of the borrower to pay back the loan in full. An investor should also remember that there have not been any defaulted loans on Debitum Network platform yet.

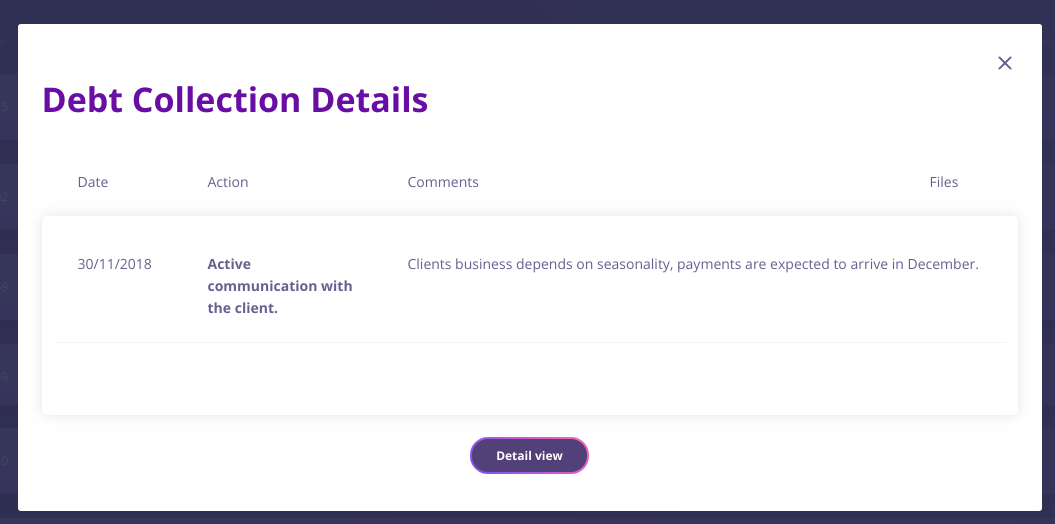

Debt collection – communication with late payers

‘Debt collection details’ button will bring you to the current status of the debt collection process. If the loan is late over 15 days (grace period is over), we talk to the broker who is in contact with the borrower and actively communicate with him to facilitate the smooth repayment of the loan. In ‘Comments’ section, you will find a comment with a likely reason for the repayment being late and when the payment is expected to arrive.

How can potential investors protect themselves?

Avoid lending platforms that do not have any security measures to protect investors’ money: buyback, collateral, personal guarantees. On Debitum Network, you are provided with all of the mentioned protective means for your funds.

Choose platforms that focus on short-term loans, because even when the loans are delayed, your money will not get stuck for long and a turnaround of capital will be much faster than with the ones that may keep your money stuck for 2 or more years. Waiting for 3 years for the payout and not getting one is not something a smart investor expects from his invested capital on p2p platform. Again, on Debitum Network, most of the loans are from 2 weeks to 3 months.

Check the default rates on platforms. Anything above 5% indicates the platform or the loan originator is not very skilled at filtering out problematic and selecting the safest loans for investors to invest in. No defaults have been on our platform yet, and our partner brokers keep defaulted loans under 2%.

Our offer for investors – invest in assets with a buyback guarantee

Investors that want to invest in exclusively safe assets can do so on Debitum Network. Our offer for them is to choose assets that have a buyback guarantee from a broker. If one invests in those and they are late with repayment more than 90 days, the broker is obligated to buy the loan with outstanding principal and interest. Thus, investors’ funds always remain protected under the buyback guarantee and he does not have to worry about late or defaulted loans anymore. The buyback icon is magnified in the asset bar below. Check for the icon if you want to invest in the assets protected under the buyback guarantee.

Join our platform and start investing

The interest in Debitum Network platform has been rising steadily. Investors onboard and invest in short-term loans every week. You can also sign up on the platform at any time and participate by helping small businesses around the world grow. You will earn attractive interest at the same time.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.