Tag: buyback guarantee

Buyback guarantee and its’ importance in online lending

Buyback guarantee and its’ importance in online lending

In P2P and P2B lending platforms a buyback guarantee is a guarantee provided by a loan originator regarding a specific loan. If repayment of that particular loan is delayed by more than a specified number of days (typically from 30 to 180), then the broker (loan originator) is obligated to buy back the loan by fully or partly compensating investors for their remaining principal invested as well as outstanding interest. Platforms differ on the percentage of principal returned and the amount of interest paid.

In a way, it resembles an insurance system, albeit for loans on p2p platforms. Thus, if the borrower fails to pay off the loan in time, it will be bought by the broker (loan originator), so the investor will not lose the money and in most cases, the accrued interest will be returned too.

How investors get liquidity in online lending?

Understanding how investors get liquidity is important as on some platforms loan maturity for loans may be a few years and if investors on those platforms invest in loans, they effectively become longer-term lenders themselves. As in most cases, they cannot get out of their positions and access their capital in a predefined time of the loan by agreement, any investor would want to know how liquid the assets he invests in are and if his capital is protected in case the borrower defaults.

Sure, certain platforms offer a secondary market as a viable option for investors to sell their stake in loans. At the time of writing only 29% of all investors on one of the largest European p2p platforms, Mintos, have made at least one investment via the secondary market. In addition, there are around 2 times as many assets available on the secondary market compared to the primary market over there. It seems that other investors on the same platform are not so keen to buy late and long loans from their fellow investors. Hence such option adds value and liquidity but is not a silver bullet and we have to go back to brokers (loan originators) for liquidity solutions.

A broker (loan originator) should have enough equity to be able to take a loss on a late or defaulting loan. Institutional investors who provide a larger amount of funding to lending companies usually request that the leverage on equity is not more than 4-10 times. Meaning that for each 1 million EUR of a loan portfolio, a broker (loan originator) would have between 100k-250k EUR in equity. What does it mean? It means that if 5% of all loans default, a lending company can still cover all losses from their equity and continue their operations.

So, a lending company with a healthy equity vs portfolio ratio is a choice trusted by institutional investors managing large funds and most likely is a better liquidity provider for a final investor in a loan if compared to a secondary market on the same lending platform.

Do high-interest rates compensate risks and absence of buyback guarantee?

Some platforms, such as Bondora bypass loan originators and keep all interest to themselves without offering any buyback guarantee. They offer plenty of high interest (30-200%) high-risk loans. A high percentage of them will default. You have to be a very picky investor in order to figure out, which loans are worthwhile investing and you will find out that the expected returns hardly ever become real ones. Statistics that Bondora have shared with their users shows that around 25% of investors on their platform have suffered losses, and have not made profit.

Loan originators on Mintos and Twino platforms offer buyback guarantee after the loans are not repaid 60 and 30 days after maturity term. On our own Debitum Network, the brokers would buy back a loan if the repayment of the loan is late more than 90 days. The best part is that the brokers pay not only the principal but also the interest, which makes investing in the offered loans seemingly risk-free. Interest rates on these platforms are relatively lower than on Bondora or on platforms that offer payday loans to invest in.

Let’s look at some data of the most popular platforms around Twino and Bondora as well as our Debitum Network and try to figure well they fare protecting investors’ capital, what security measures they measure and a few other pieces of data:

From the table above we may draw a number of conclusions. Firstly, high-interest rates without a buyback guarantee will not deliver expected or promised returns as the number of defaults on these type of platforms (e.g. Bondora) is very high and most investors actually lose money as selecting loans that will actually be paid off by the borrower is inexplicably difficult.

If businesses or people are able to borrow at smaller interest rates, there is a higher probability that they will repay the loans, as opposed to borrowing at high interest rates that exceed 30% annually. Smaller interest rates will likely have smaller expected returns, but as the rate of defaults is much smaller, the real net return will be higher than with loans that have very high-interest rates and no buyback guarantee.

Shorter term loans effectively decrease your risk. What is the logic behind it? Very simple! If the company has been paying interest for the whole year, it will most likely not default if there are a couple of months left. This is one of the reasons why Debitum Network focuses on short-term loans for SMEs. We see that offering investors to invest in 1-3 months duration loans carries less risk and psychological pressure for them than keeping funds locked for a year or more with limited possibilities to exit the position.

Do buybacks eliminate risk completely or how can investors protect themselves?

A loan originator may go bankrupt and in that case, your money invested in the loans of the originator will most likely be lost. Eurocent loan originator went bankrupt and the loans it put on Mintos platform defaulted, thus causing investors to lose money on both principal and interest (Mintos doing their best to get the investors’ money back). Thus again, a buyback guarantee is as good as the company behind it.

Investors could choose only loans that have a buyback guarantee from a broker. It would be wise to choose only those that offer the option of buyback even at the expense of getting smaller interest rates. You want as much clarity from platforms and brokers operating on them regarding buybacks too. In March 2017 Twino introduced ‘payment guarantees’ rather than buyback guarantees. This change means that investors are now left owning non-performing loans for up to 2 years, and relying on Twino to make the payments due. The loans cannot be sold on the platform. Thus liquidity for investors dries up and investors have to wait for years until the money is eventually returned in case of default.

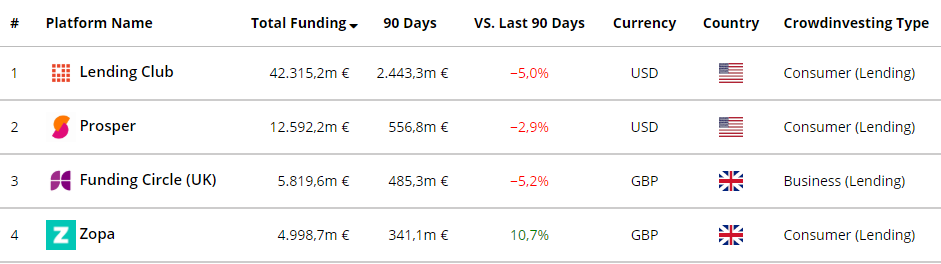

Spreading your investments in different loans and possibly different loan originators or even platforms is one of the options as diversification significantly reduces risk due to the fact that an investor ‘does not keep all eggs in one basket’. Asset-backed p2p or p2b loans are also a form of insurance as in case of a borrower’s default an asset can be sold and investors’ money paid back. Smaller interest rates for businesses is an advantage too. If borrowers are charged smaller interest rates they have a higher chance of repaying it rather than defaulting as they would if they were charged some rates from 30-50% annually or more. In the same fashion, collecting payments on an asset-backed business loan is simpler and usually faster than collect them from a bankrupt private person who defaulted on a payday loan issued by some payday loans’ platform. Thus, Debitum Network can proudly go shoulder to shoulder with long seasoned p2p platforms such as: Funding Circle, Lending Club, Zopa, Assetz Capital, Fellow Finance, Grupper, October, Ratesetter, FundingSecure, Lendy, MoneyThing and etc.

Investing with Debitum Network

Short-term loans with maturity mostly from 1 to 3 months, interest rates from 7 to 10.85% and a buyback guarantee is an offer from Debitum Network to investors on our platform. This enables investors to gain a number of things: earn attractive interest, have a fast turnover of their capital (1-3 months) and by means of buyback guarantee to protect their investments as much as possible.

Got interested? Try DEBITUM NETWORK!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Debitum Network – a leader in interest rates for Invoice Financing loans

Debitum Network – a leader in interest rates for Invoice Financing loans:

High yield assets are definitely one of the top reasons that attract investors. The second one would be assets that are secure. After the 2008 crisis, most Central Banks slashed interest rates to zero or even below it. Keeping money in savings accounts became an unprofitable way to handle your money, despite a safe one. Alternative finance/investment platforms both P2P and P2B started growing like mushrooms after rain. They started offering above-average returns, in most cases higher than one can expect to get investing in most popular options such as stocks, hedge/mutual funds, or indexes. Debitum Network is not an exception as it offers some of the highest interest rates among investment platforms for loans in Invoice Financing category.

Overview of alternative investment platforms

P2PMarketData gives us an overview of the major players in alternative investments (P2P/P2B. There are currently around 80 well-established investment platforms around the world. Most of them specialize and accept/originate specific types of loans as assets for investment. They basically fall within three major categories:

- Consumer loans (33 platforms)

- Real estate loans (22 platforms)

- Business loans (28 platforms)

We can see that the distribution of these three types of loans among platforms are almost equal. Statistics regarding returns vary and it would be difficult to say the exact percentage for each platform as; not all are secured loans or have buyback guarantees, interest rates on assets vary and they change.

Let’s say you choose Lending Club, which is a top P2P lending platform in the world. They provide unsecured consumer loans for investment with various returns based on the risk category. What it actually means is that you can make 15% or you can lose all your money if you invest in loans that default and become uncollectible (this week one of the leaders in UK P2P platforms Funding Secure went bankrupt).

A leader in business loans Funding Circle (in the UK) also offers investment in unsecured business loans (development loans secured by property and land). The expected returns with the platform would be up to 7%. Taking into account, that most loans are unsecured, the returns are really low.

A lot of other investment platforms both in consumer and real estate will offer returns of around 8%-13% annually. But there is one but!

Expected Returns differ from real ones

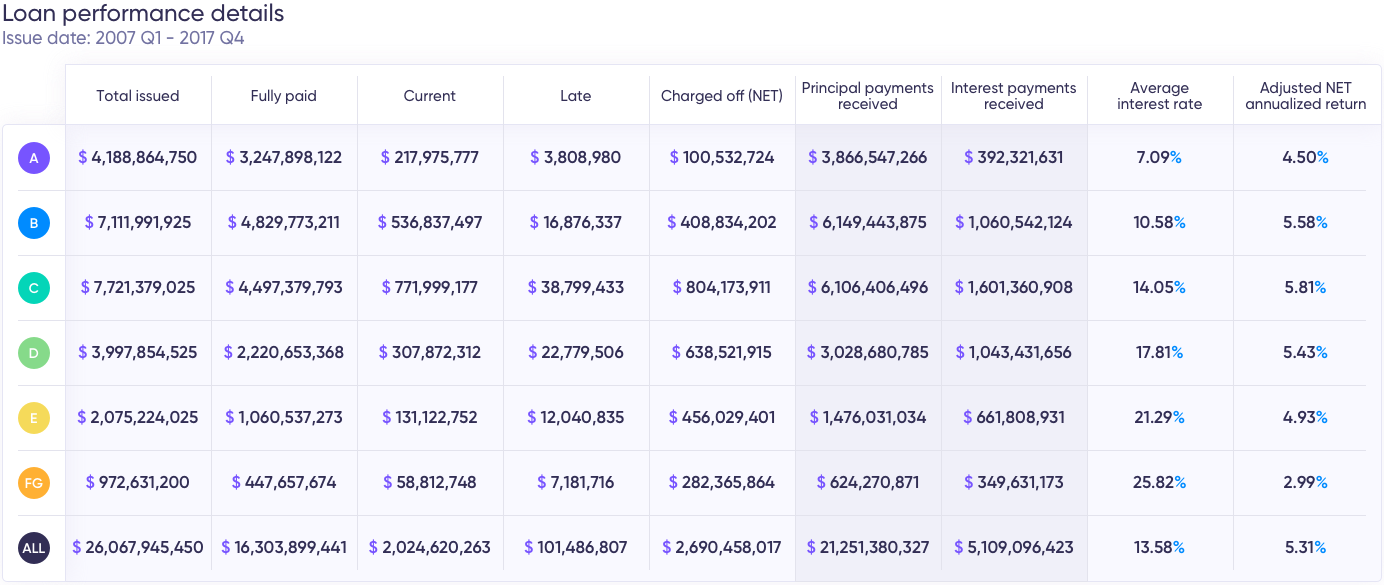

It is obvious that returns depend on risk levels. If the platforms do not have an implemented buyback guarantee, the expected returns can be radically different from the real ones. Lending Club has shared some stats on their website and you can see for yourself how greatly adjusted annualized returns differ from the projected interest rates under specific risk categories. Defaulted loans can drag your real returns down up to 3-6 times.

Source: https://www.lendingclub.com/info/demand-and-credit-profile.action

For the sake of being discreet, we are not going to name specific names, but there are platforms that have default rates of 30%. It means that investing in these types of loans you are basically buying a lottery ticket. You may get lucky and earn around 20% annually, or lose all of your money. You have to do a thorough and time-consuming analysis before you can make the right picks for investment.

Debitum Network returns and conditions

Currently, Lifetime Invested Interest Rate on Debitum Network platform is 9.20%. Most of our investors get even better returns. How is that? Well, you can exclusively invest in 9.50%-10% assets and your returns will be higher than the average. Additionally, most of the loans on the platform have a buyback guarantee. In case, a borrower defaults on his obligations, the broker who issued the loan will have to buy it back with the outstanding principal and interest. Thus, the returns are real. Very few platforms will offer that returns with a buyback guarantee. Due to the guarantee, there has not been a single default on Debitum Network.

Furthermore, not only most of the assets have a buyback guarantee, but each asset will have a specific penalty rate, which an investor is going to earn, in case the borrower is late with repayments by more than 15 days (15 days is a grace period when no penalty is charged to a borrower). Penalty rates vary from 2% to 4.5%. It means you are able to earn beyond the platform average of 9.20%. Very few platforms will offer a penalty rate for late loans.

Thus, taking into account a current Lifetime Invested Interest Rate, a buyback guarantee, and a penalty rate, we can state that Debitum Network has the highest interest rates in Invoice Financing category. Take a look at how interest rates (earned) fluctuated since the launch last September, till the beginning of October this year. Have in mind, that these are the rates investors really received, (not adjusted) and there were no factors that could reduce them (no defaults due to the protection by a buyback guarantee).

Top asset of the week

The asset is from our partner and loan originator Factris. The borrowing company is a producer of electricity which has more than 340 thousand EUR in revenue, more than 60 employees and has been in business for more than 7 years. The Purchaser of the invoice is a manufacturer of petroleum products. It has more than 4 billion EUR in revenues, employs more than 1000 people, and has been in business for more than 28 years. Like what you see? Be sure to add it to your portfolio.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Debitum Network partners with a loan originator VIHOREV INVESTMENTS from the Czech Republic

Debitum Network partners with a loan originator:

Debitum Network keeps on growing and we onboard more new parties on our platform every month. Today, we are proud to announce a new partnership with a loan originator from the Czech Republic – Vihorev Investments

Debitum Network partners with a loan originator:

Debitum Network keeps on growing and we onboard more new parties on our platform every month. Today, we are proud to announce a new partnership with a loan originator from the Czech Republic – Vihorev Investments

. Vihorev Investments is a prominent real estate developer with years of experience in the market. The company focuses on developing real estate projects in Prague, the Czech Republic.

Through the partnership with Debitum Network, Vihorev Investments will offer the first test assets in the industry of real estate. These would be the first assets of a real estate industry on the Debitum Network platform and we hope for a successful continuation in the partnership after the first assets have been funded.

About Vihorev Investments

Vihorev Investments has been active in the real estate market for many years, building or managing assets worth EUR 20 million. In 2018 alone, it sold real estate worth approximately EUR 8 million. At present, it actively operates 4 projects with 177 residential or commercial units and is preparing to launch other projects.

A real estate project ‘STRAKONICKÁ’

Vihorev Investments has just successfully finished a residence project ‘STRAKONICKÁ’. The project has been developed in the heart of Prague and consists of 28 apartments and 4 studios. The total area of the residence is 1650 m2. The apartments are suitable for housing, business or can be used as an investment. 100% of the apartments have already been sold.

Test assets on Debitum Network (STRAKONICKÁ project) from Vihorev Investments

Debitum Network is going to refinance the equity of the project “STRAKONICKÁ”. This will be done via Vihorev Investments’ local SPV (Special Purpose Vehicle). The refinancing sum is spread over 15 ‘test assets’ that are uploaded on Debitum Network platform and are available for investing. We hope that the first mutual project between Debitum Network and Vihorev Investments will be successful and this will grow into a further fruitful partnership and more assets from the loan originator will be offered on Debitum Network platform.

A selected asset from the project STRAKONICKÁ

We encourage everybody (register on our platform, if you haven’t done it yet) to look at the newly uploaded assets from our new partner and possibly adding some of them to their portfolio (if you can’t see the loan originator, be sure to check the filter and adjust it accordingly). We have selected the top asset from the batch of assets (STRAKONICKÁ project) for you. It is expected that over the upcoming 5 years the project will generate a 148% return on equity from renting the apartments and have an average occupancy rate of over 75%. Furthermore, 100% of the borrower shares are provided as collateral. The asset also has a buyback guarantee. Does it sound good enough? If yes, be sure to add it to your portfolio. Do not hesitate as the assets on the platform are funded really fast. Check out the asset.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Investing in business loans versus real estate loans

Investing in business loans versus real estate loans

Interest in alternative finance platforms has been increasing steadily together with the number of platforms. Currently, there about 100 worth mentioning P2P and P2B platforms (Debitum Network included). The assets (loans) that the platforms offer for investors to invest in can be put into three main categories: consumer loans, real estate loans, and business loans. Most of the platforms specialize. About ⅓ of them focuses on consumer loans. We covered those while comparing consumer loans with business loans. ⅓ of the platforms focuses on business loans. And about ⅓ of platforms focus on real estate loans. The aim of this blog post is to compare business loans versus real estate loans within the context of alternative financing platforms.

How are business loans different from real estate loans?

Business loans are issued solely for businesses and for business purposes. They can be secured (company’s assets are pledged as collateral to be used in case of failure to repay the loan) or unsecured (no assets are pledged as collateral and the lender can only make a general claim for the assets of the borrowing company). Secured loans, naturally carry smaller risks and, consequently, have smaller interest rates.

Real estate loans are a type of investing that is backed by real estate (property both residential and commercial) or investing in loans given for projects related to real estate/rental. In the case of bad loans, a lender can make a claim for the assets that are pledged (real estate).

The leading real estate platforms and the advertised returns

According to p2pmarketdata.com, there are 17 platforms focus solely on real estate (lending). Around the world, there would be more (around 30), but only 17 stand out. The three leading platforms in real estate lending are Sharestates, Octopus Choice, and Estateguru. Sharestates (in the US) has a 10.32% annualized return for investors. Octopus Choice (in the UK) currently has a target interest rate of 4%. Estateguru (in Europe) is the leader in terms of returns and has the historical average weighted returns of 12.12%.

Risks of investing in real estate loans

The idea that real estate loans are backed by tangible assets (real estate itself) is enticing and provides confidence in this type of lending. However, the most recent reports about Lendy (once a leader in real estate loans, now has an outstanding loan portfolio of about 155 million GBP, of which about 90 million GBP are in default) as well as independent reviewers who diversify among various alternative finance platforms paints a different picture.

In the case of default, real estate that was pledged has to be sold to return investors’ money, plus interest. However, selling real estate that failed as a project may not be that easy, as who will pay the desired amount (to cover the debt to say nothing of outstanding interest). Most of the platforms do not have a buyback guarantee as the real estate serves as a guarantee to get back investors’ money in case of default. Investors can wait for months, possibly years (legal proceedings, sale of property takes a lot of time) to get their funds back. Taking what has been said into account, 8-12% (Lendy advertised gross annual return before tax up to 12%) annual interest advertised on most real estate lending platforms, may not be the real returns that an investor gets.

Some real estate lending platforms have a Reserve Fund (Provision Fund) which is meant to cover the losses for investors who end up holding bad loans. However, not all platforms have it and coming back to the example of Lendy, a conclusion can be made that if investors are exposed to a large number of poor quality loans, their funds can be lost entirely with little or no hope to get them back.

What are the risks of investing in business loans?

Investing in business loans is exposed to the same risks as investing in real estate loans. A business loan may default and if it does not have any safeguards as collateral or a buyback guarantee investors who put their funds into such a loan will lose their money. With the interest rates being very similar in real estate and business loans one might ask, why choose one type of investment over the other? If both can default, and both can return relatively the same returns, is any type of investment is better?

Quality loans with a buyback guarantee are the solution

Inherently, one type of loans is not better than another one. Both real estate platforms (as in case of Lendy) or lenders that offer business loans (as in case of Eurocent bankruptcy) can go bankrupt. Quality loans, backed by a number of safety guards make the type of lending advantageous, whether it be real estate loans or business loans.

One of the best safety measures that help to protect investors’ funds is a buyback guarantee. A lot of platforms that offer business loans have implemented the guarantee for their loans. A buyback guarantee means that if the borrower is late with the repayment of the loan by a predefined amount of days (usually 30-90, the actual number depends on the platform and a loan originator that issues a loan) the broker (loan originator), who issued the loan will have to buy back the outstanding principal with the outstanding interest. The guarantee significantly reduces risks for investors. If the loans are high quality there would be very few defaults, and, consequently, the originator will be able to fulfill his obligation to buy back a few that underperform.

On the other hand, a buyback guarantee is as good as the broker who offers it. If the loan originator (broker) has a lot of bad loans in his loan portfolio, eventually, he will not be able to honor his promise to buy back all of them and will have to declare bankruptcy as we have seen in Eurocent case. Then, investors who put funds into the loans will lose not only the promised interest but also the principal (with very little hope to get the money back).

What about business loans on Debitum Network?

A buyback guarantee has served well users on Debitum Network platform. Within the period of 9 months since the launch there hasn’t been a single default on the platform. A few loans were bought back by the loan originators, and investors always got their principal, interest, as well as money earned on penalty rates (for late loans). This proves that quality business loans with a buyback guarantee are the ultimate choice for investors who search how to employ their capital on alternative finance platforms, whether it be real estate loans or business loans.

Earn steady returns investing in business loans on Debitum Network platform

One of the main advantages of Debitum Network is attractive interest rates for assets in invoice financing with a buyback guarantee. They are among the highest in the industry. Real interest paid to investors who use our platform, currently stands at 9.75%. Thus, we have selected an asset for you from the platform, which you might consider adding to your portfolio for investment. The borrowing company specializes in the re-sell of authentic branded products for customers in over 100 different countries. It has over 50 employees and over 500,000 EUR in revenues. Check out the asset!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Investments in business loans versus consumer loans

Investments in business loans versus consumer loans

High-interest rates remain the key factor which attracts people to invest in assets on alternative finance platforms (P2P or P2B/B2B). Low-interest rates in the banks have driven people to search for alternative ways to put their money to use instead of keeping them in savings accounts for ridiculously low returns. P2P and P2B lending platforms offer way more appealing options to gain returns than most other investment solutions around. However, promised returns may not be the delivered ones. Let us look at what impacts the real returns and why investing in business loans might be a better option than consumer loans.

How are business loans different from personal/consumer loans?

Business loans are issued solely for businesses and for business purposes. They can be secured (company’s assets are pledged as collateral to be used in case of failure to repay the loan) or unsecured (no assets are pledged as collateral and the lender can only make a general claim for the assets of the borrowing company). Secured loans, naturally carry smaller risks and, consequently, have smaller interest rates.

Consumer loans are personal ones and are issued for private individuals, typically for non-business purposes (buying a home, car, covering social security liabilities, paying of bills). If an individual fails to pay off the loan, the lender will come after his/her personal assets to get back the lent money. As lenders usually have collateral from businesses they won’t require personal guarantees from business owners, which they would do from individuals taking out a personal loan.

Some facts about the leading P2P/P2B lending platforms

Source: p2pmarketdata.com

According to P2PMarketData.com out of 74 top P2P lending and equity platforms (Debitum Network included) about 20 focus solely on consumer lending. Among them the leaders in volume and total financed loans (Lending Club and Prosper) in the US. 12 of them do both, but with a tendency to offer more consumer loans (leading platforms: Mintos, Twino). 17 belong to Real Estate (Lending) with Sharestates (in the US) and Octopus Choice (in the UK) being the leaders in the sector (we will do comparisons with these platforms and business lending in future posts). 23 platforms focus solely on offering investments in business loans (Funding Circle from the UK being the leader of the group of platforms and our own Debitum Network belongs to the group too).

What are the risks of investing in consumer loans?

Independent reviewers state that investing in consumer loans, even on the most secure P2P lending sites such as Lending Club or Prosper can help you make a 15% return on your investment or cause you to lose money. How is that? The answer is quite simple, different loans perform differently. Some borrowers go bust and they never pay back. Investors typically lose money on these type of loans. Unlike businesses private individuals may not have cash flows to offer, or valuable assets as collateral and the ones that are offered are often not enough to cover the principal of the loan, to say nothing of the outstanding interest. Thus an expected 15% return on investments in consumer loans may be significantly slower and if an investor picks non-performing loans he may not make any money, but lose all of his investments.

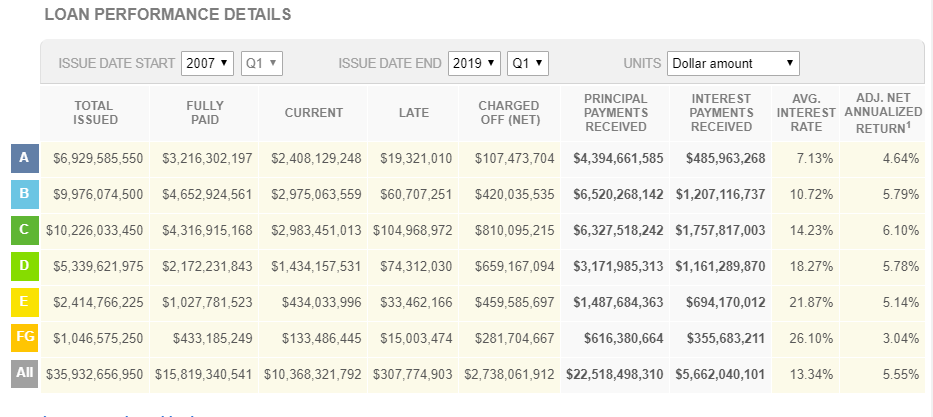

Most of the lending sites rate their loans and the loans with the lowest risk get the lowest interest rates, and the worst risk rate loans get the highest interest rates, some might be as high as 30%. However, even low-risk loans sometimes underperform and default. It takes thorough analysis, wide range classification, and insight to select the most secure loans to get a conservative 5%-7% adjusted annual return on the investments. Lending Club (one of the most trusted P2P lending platforms) gave this table to show how average interest rate may differ from adjusted annualized return for investors.

Data source: https://www.lendingclub.com/info/demand-and-credit-profile.action

Data source: https://www.lendingclub.com/info/demand-and-credit-profile.action

What about the risks of investing in business loans?

The main risk of investing in business loans is the same as that of investing in consumer loans – a loan may default and investor lose all of his invested money. So, why not invest then in consumer loans if they offer higher interest rates? The question is logical and it has the logical answer. Business loans are inherently safer to invest in as they will offer more safety for investors’ funds. A business may pledge collateral (equipment, warehouse, cars, goods), invoices as a guarantee that the loan will be fully repaid. In case of borrower’s failure to pay off the loan, the lender can go after the assets of the borrower and get back the principal and interest due on the loan (in the best case scenario).

On some platforms (Debitum Network included) loan originators that upload their assets on the platforms also offer a buyback guarantee for the loans they have issued. This means that if the borrower is late with the repayment of the loan by a specific number of days (typically 30-90 days), the broker who issued the loan will have to buy back the outstanding principal and the outstanding interest. This reduces the risk of investing in business loans on the platforms to the minimum.

Under these conditions, the real possible risk from the possibility (a rare one) that the loan originator will go broke and fail to buy back the principal and outstanding interest. It happens from time to time as in the example of the loan originator Eurocent (on Mintos platform), when investors lost their money invested in the loans issued by the mentioned broker. Despite the efforts of the platform to get back investors’ funds, the hope of positive outcome seems to be dim. Thus, the buyback guarantee is as good as the loan originator that provides it.

How safe is investing in business loans on Debitum Network platform?

However, these events are rare and lending to businesses with the protection under a buyback guarantee provides investors with maximum safety. In the period of 8 months since the launch of Debitum Network platform we have uploaded hundreds of loans to choose from, and there hasn’t been a single default. Thus, investors have got back all of their invested principal and earned interest. Plus, late loans give investors an opportunity to earn extra profits from existing penalty rates (those differ among loan originators and specific loans), thus increasing his/her profits along the run. At the time of writing, the average interest rate paid to investors on Debitum Network platform is 9.72%.

Want to earn attractive interest on Debitum Network assets?

We regard the safety of investors’ funds seriously and take only the best assets that our partners loan originators offer. Most assets are short term and this is another safety guard for investors’ capital because borrowers have to prove that they are able to pay off the principal and interest for a considerable term after taking a loan before we accept it on our platform. Short term, also means that your capital is never frozen for a long period of time. Fast turnover and compounding interest is what makes our platform attractive! Want to start investing?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What are the risks of investing in short term loans on P2P/P2B platforms

What are the risks of investing in short term loans on P2P/P2B platforms

Risk/reward ratio is at the heart of each type of investment. A rule of thumb remains the same, the higher the risk, the greater the reward, the lower the risk, the lower the reward. Institutional investors seek the type of investment options that offer the highest return with the lowest risk. Risks may vary and some investments may have so many of them that it may be unwise to even consider them. A relatively new way to invest is P2P/P2B platforms. Despite criticized by the mainstream these alternative finance platforms have gained more and more popularity in recent years. Let us look and see how risky they are and how those risks can be reduced, and profit increased.

Not all alternative investment platforms are created equal

Even within the alternative lending/investment platforms, there are significant differences that may impact your risk/reward ratio. Some platforms offer personal loans to invest in, other real estate projects, others such as Debitum Network, focus on investing in short term loans for businesses (invoice financing and business loans).

Obviously, the percentage of defaults on the platforms vary greatly too. One of the leaders in the alternative lending/investment market Zopa has around 0.6% of defaulted loans, while another prominent player in the field (according to independent research) may have around 30%. In the 9 month period of existence, there has not been a single defaulted loan on Debitum Network platform. Commercial banks typically have around 1%-2% of defaulted loans.

Online platforms that offer users to invest in personal loans or payday loans may have high-interest rates: 15%-35%. However, taking into account that on some of the platforms 1 out of 5 investors may lose money, the average net return on them will go down to around 10%. It is obvious that the aspect of safety should be taken more seriously while talking about investments and returns on the platforms.

What are the risks and how can they be reduced?

A borrower may default on its’ obligations to pay off the loan and it is the biggest risk for an investor who has put money into such an asset. The invested money can be lost and never repaid.

To avoid such a scenario, a lot of (not all) platforms have implemented a buyback guarantee, which basically means that if the borrower is late with his repayments by more than 30-90 days (60-90 on Debitum Network platform. The actual number depends on the loan originator that issued a specific loan), the broker/loan originator will have to buy back the specific loan with the outstanding principal and interest. So, if a specific loan defaults, the investors’ risk is reduced to the minimum.

Another risk, that has much less likely probability of happening is when the loan originator goes default. This happens from time to time. When Eurocent loan originator (on Mintos platform) went broke, investors that invested in the assets of the loan originator, lost their money. Despite the fact, Mintos is doing everything in their power, there is little hope for investors to regain their invested balance and the interest earned on it. That’s why the buyback guarantee is as good as the loan originator that provides it. A proper selection and thorough screening of loan originators are necessary before onboarding them on an investment platform. Debitum Network selects loan originators carefully as well as their assets that are placed on our platform for investment. Due diligence parties as well as risk assessing companies do thorough risk rating defining the probability of default of the borrowing company and the loans uploaded on our platform.

Extra measures to ensure the safety of investors’ funds

Debitum Network solely focuses on loans for businesses as businesses have a higher chance of repaying the loan than private individuals. Businesses will unlikely borrow at such high-interest rates that some P2P lending platforms offer. Offering extra guarantees and taking extra risks borrowing at 20% is something that SMEs will hardly ever do. Private individuals that may take a loan for a car or a home will have to undertake very high risks that they are not very skilled at handling, thus increasing the likelihood of a potential default and consequently loss of the investors’’ money in the given loan.

P2P platforms similarly use other protection methods for investors funds. Collateral from borrowers or real estate can serve as a guarantee that in case of default, it will be used to repay the investors. However, even sold the collateral may not be enough to compensate the entire invested amount, to say nothing of the outstanding interest. Real estate in the same fashion can be an illiquid asset and it may take a lot of time to sell it to repay the investors (with no assurance that they will get the full invested amount back or due interest). In that respect, a buyback guarantee is a far superior method for protecting investors’ funds and profits and the loan originator (in case of default of a specific loan) buys back both outstanding principal and interest.

Personal guarantees from the owners of the borrowing businesses are yet another protective measure to ensure the safety of investors funds. By the guarantee, the owner of the business guarantees, that if the business fails to pay off the loan, he/they will pay it off. It is typically not tied to a specific asset. In the event of non-payment, the lender can go after the personal assets of the guarantor.

Some platforms employ third parties to do risk assessment and due diligence services. This ensures transparency and quality of services as no conflict of interest is involved. Our own Debitum Network takes these service providers from countries where borrowing parties reside and thus, risk assessment or due diligence services are more accurate due to the specialization of the party doing the services and the knowledge of the local market.

Want to invest in low-risk assets in Debitum Network?

On Debitum Network we apply all available security measures to ensure investors funds’ are safe. Last week we onboarded a new loan originator Aforti Finance, who is the leading non-bank lender in the Polish market. This enables us to provide new investment opportunities, flexibility, and options to choose from for our customers. The first assets from the loan originator have already been uploaded on Debitum Network platform and you can start investing in them. They have attractive interest rates and a buyback guarantee. Check them out!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Aforti Finance, the leading non-bank lender joins Debitum Network

Aforti Finance, the leading non-bank lender joins Debitum Network platform

Debitum Network keeps on growing and new parties onboard our platform each month. Today, we are happy to announce a new partnership as we onboard a new loan originator from Poland Aforti Finance. Aforti Finance is one of the leading non-bank lenders in the Polish market, which is one of the largest in the Central and Eastern European region. It is part of Aforti Holding, which is listed on the Warsaw Stock Exchange. We sat down to talk about the company with Tomasz Kaźmierski – the Chief Sales Officer (CSO) and the Vice President of Aforti Finance S.A. Get acquainted with our new partner!

How would you introduce Aforti to our community?

We are part of Aforti Holding – a company listed on the New Connect market being side market of the Warsaw Stock Exchange. We have been operating on the Polish market since 2014, is currently the largest non-banking financial institution providing financing to business clients, mainly small and medium enterprises. The Board of Directors team consists of experienced managers with a strong background in financial institutions as well as in non-banking companies. Therefore, in the credit assessment of customers, we implement procedures and rules similar to banking ones, which allows for skipping too risky customers. Also, we focus on process automation – which makes our offer really competitive in comparison to other market players in Poland. We offer our products through our own outlets and through dedicated Call Centers. At the same time, we work with brokers, however closing the deal is being done by Aforti Finance employees, what allows us to properly check the customer and greatly limit the number of bad loans and subsequent NPL (Non-Performing Loans).

Can you describe how your lending process works? How is it different from getting a loan in a bank?

Our process is pretty simple but precise and accurate. Also, what is important for our clients, it is really fast. As soon as we receive a client’s documents, we begin the analysis involving an automatic check of the client in external scoring databases (including bank databases), where our potential client shall be verified. In addition, we automatically process bank statements using specially designed software that ensures their authenticity. We can close the entire decision process in 4 hours – we meet the expectations of the client who expects decisions as soon as possible. If the amount of the loan granted meets the client’s expectations – we arrange a meeting with our verifier, who meets with the client in the place of his business to verify and confirm originals of all previously provided documents, including bank statements. Also, we visually verify client’s business activity, which allows us to eliminate almost any potential frauds and extortions in this area. No bank on the Polish market operates so fast while maintaining such high-security standards in parallel.

Which markets do you operate in and what are your plans for future expansion?

At the moment, we run our business in Poland, where we have over 70% market share. At the end of October 2017, we were officially licensed by the National Bank of Romania to operate in Romania and we want to start our operations there in max a few weeks. Our plans are not limited to Romania – we want to expand soon our presence to other countries in the region.

What distinguishes Aforti from other loan originators in the region?

We operate very quickly, much faster than our competition. We are in a position to do that without losing the quality of loans cause we implemented a significant number of automated processes in the area of assessing the customer’s creditworthiness using internally prepared scoring. Also, we are in a position to grant a loan needed to pay off the client’s liabilities in ZUS (Social Insurance Institution) or unpaid taxes. Such purposes of the loan are unacceptable for most of our competition. Allowing that we help entrepreneurs to improve their financials and at the end to enable cooperation with banks. For us, it translates into a growing number of satisfied customers, more recommendations of our services, and finally into better financial results and bigger dividend for our shareholders.

Who is a typical customer of Aforti?

Almost 80% of our clients run their business for more than 24 months, and more than half of them – over 48 months. We do not offer our services to newly established entrepreneurs. The average age of our entrepreneur exceeds 40 years. These people – before starting their own business – have gained experience in other companies. A typical client runs its business as a sole proprietorship, focusing its activity on trade (wholesale and retail), transport, storage or construction.

What are the products presented in your offer?

We offer unsecured loans to the sole proprietorships and limited liability companies. In both cases, the maximum loan value is 150k PLN, and the maximum loan maturity is 36 months. In our product portfolio, there is also mortgage loan and in this case, it is possible to obtain financing up to 500k PLN, LTV up to 70%, for a period of up to 60 months. The average value of granted loans amounts to 86k PLN, and the average maturity is 18 months.

How was 2018 for Aforti and what are your plans for 2019?

2018 was another year of strengthening of Aforti Finance position in the area of B2B loans for small and medium enterprises.

In 2018, over 3,820 loan applications were submitted for an amount of PLN 479 million, which means over 50% growth comparing to the previous year. In terms of sales numbers, we granted loans worth over PLN 59 million, beating last year record in terms of volumes and the number of loans.

Currently, we are the leader on the Polish B2B loan market (loans granted by non-banking financial institutions) and we intend to maintain this position in the coming years. Talking about further expansion and business development – in November 2018 we’ve obtained a license granted by the National Bank of Romania allowing us to start our operations in this country. Likewise, as soon as possible we want to start our operations in other “low entrance costs” countries in the region.

What are the benefits for investors to invest in loans issued by Aforti?

From the 3 most important features of every investment (profitability, liquidity, risk level), we put all our efforts on the last one: lowering risk. As described on previous pages, before we grant a loan – we thoroughly verify involved risks including the activities carried out by the customer. Our target is limiting to the minimum or even eliminating the risk of frauds. Nevertheless, we understand that running a business always involves risk – so even the best scoring systems will not provide a 100% loan repayment guarantee. Therefore, regardless of the period for which we provide financing, we give to the investor a guarantee of buying back loans offered on the Debitum platform in case, when a borrower is more than 60 days late with the payment of their obligations to Aforti Finance. As a result, investors limit their risk level to the risk related to Aforti Finance, not to the borrower.

What are your expectations for cooperation with Debitum Network?

The most important for Aforti Finance is to build long-lasting and fruitful cooperation. As we plan to significantly extend the size of our operations, we need to be supported by a partner, who understands our needs, is technically and operationally advanced, and also has the scale of the business big enough to secure our financing needs. We believe Debitum Network can become such a partner.

The first assets from Aforti Finance are coming soon

The first assets from Aforti Finance will soon be uploaded on Debitum Network platform and investors can start investing in them. The assets will be short term with an annual interest of 11%-12%. All of them have a buyback guarantee. Got interested? Be the first one to invest in the assets and earn attractive interest.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Services industry on Debitum Network platform

Services industry on Debitum Network platform

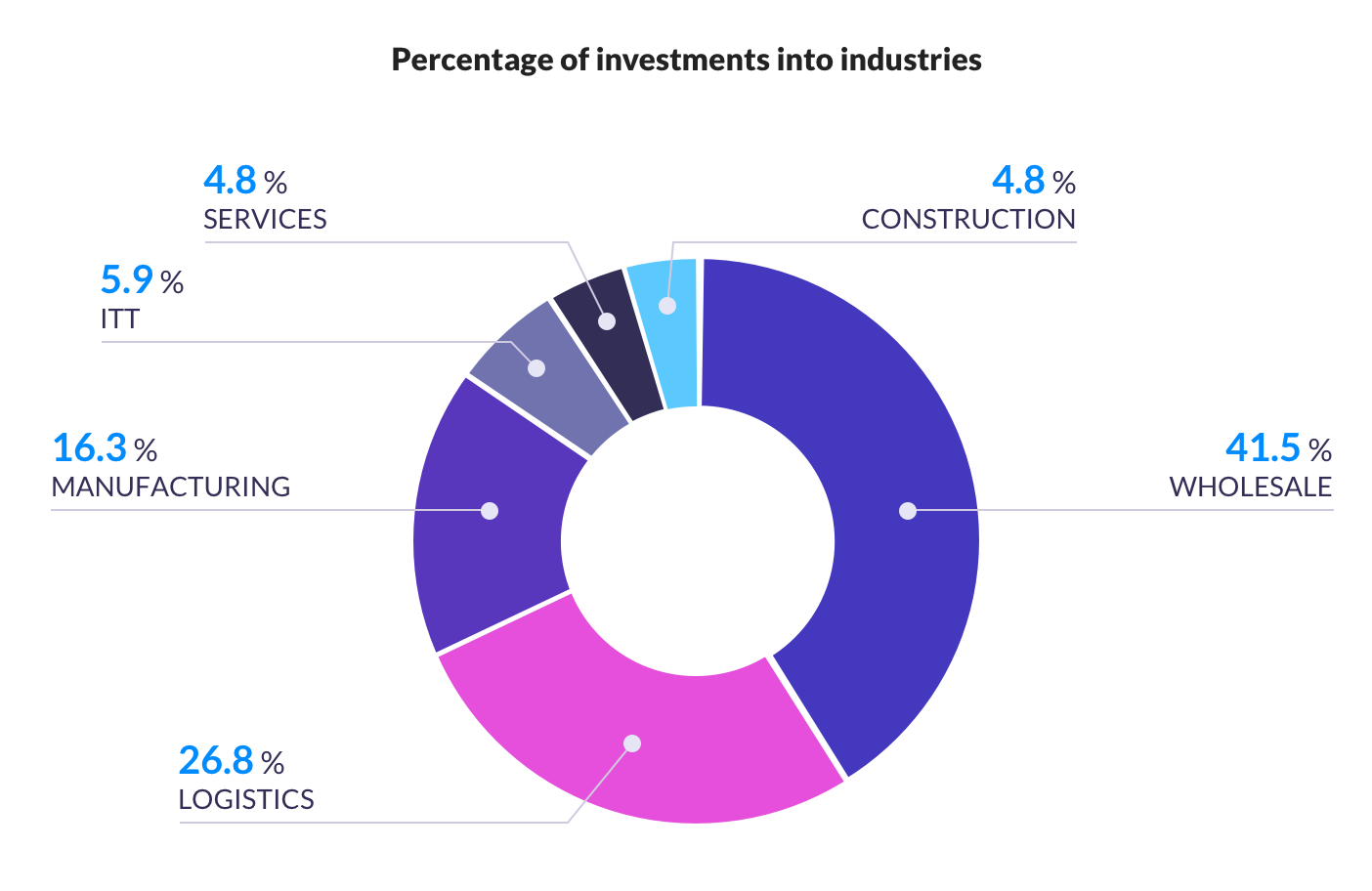

Wholesale industry assets were the most popular among investors on Debitum Network platform in February. The assets had the highest interest rates, so no wonder investors rushed to invest in them. However, one of the key investment rules should never be neglected – always diversify. Diversification reduces risk as funds are distributed among various investment options as well as risk classes. Services industry was overlooked by investors last month. We see no good reason why and in this blog post want to stress why investors should consider adding the assets from the industry to their portfolios.

From the chart above, one can see that investors preferred Wholesale, Logistics and Manufacturing industries and neglected ITT, Services, and Construction. Only 4.8% of all the invested money was in the Services industry. Investors chose to invest that way. However, it does not mean that the assets in the industry are inferior, worse or less safe than those of other industries, and in this post, we will prove that they are safe and worth investing in.

|

Services industry assets have a high credit rating |

Assets from the Services industry on Debitum Network platform have a high credit rating. They fall within the range from B to B-. The ratings for the assets of Services are presented by our reliable partner risk rating company Scorify. B and B- rating mean that the probability of default of a company within the next 12 months is between 0.55%-1.06%. Thus, we can state that the assets carry very low risk and is a good investment option for investors of various risk tolerance classes, and the best for moderate risk tolerance investors.

|

All the assets have a buyback guarantee |

After an introduction of a buyback guarantee on Debitum Network platform, any asset in any industry (including the Services industry) on our platform has a buyback guarantee. What does that mean for an investor? If a borrower is late with the repayment of the loan (it may occasionally happen) by more than 90 days, the broker (loan originator) who issued the loan will be obligated to buy it back, plus outstanding principal and interest, minimizing the risk for the investor to the minimum.

Another thing that makes an investor benefit in case the loan he has invested in is late is a penalty rate set by a loan originator. Investors are now able to see a penalty rate (annual interest rate section) for a specific asset if the borrower is late with the repayment of the asset. The investor will get the percentage of the penalty rate they see, in case the repayment is late by the defined number of days. Current assets from the Services industry have 4.5% as set by our partner and loan originator Debifo.

|

Buyers of invoices are strong businesses |

Companies in the Services industry deal with other companies. The latter ones pay for the issued invoices and the services provided. It is important as a company that is offered service is a strong company and long term relationships with the service providing company. It means, there is a better chance that the invoice will be paid for and the loan eventually repaid. These final invoice payers have big revenues from 10 to over 100 million Euros. They are usually long term partners with our partners loan originators, and they have proven to be reliable business entities to do business with.

|

Borrowing companies and their customers are experts in the markets they operate |

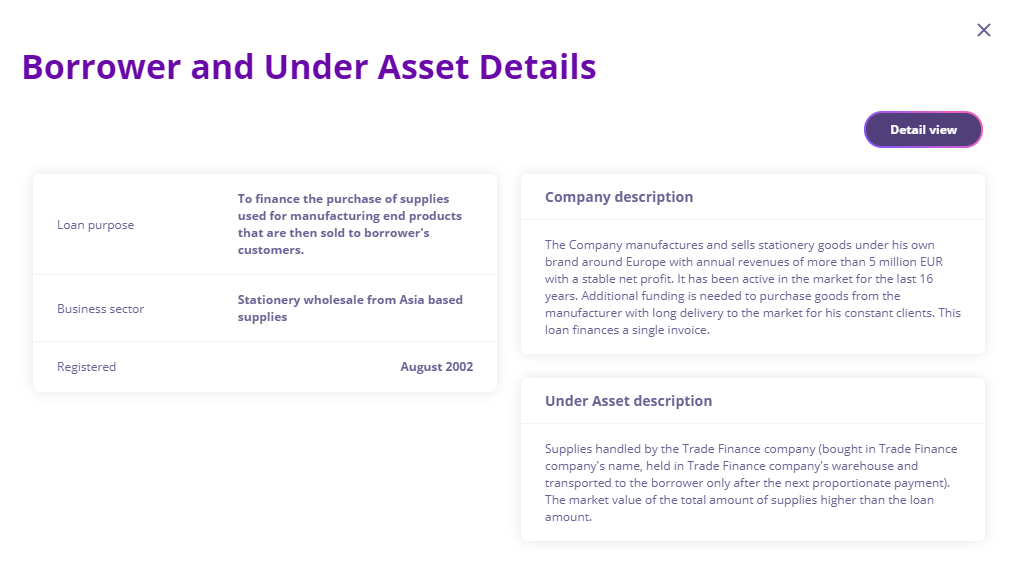

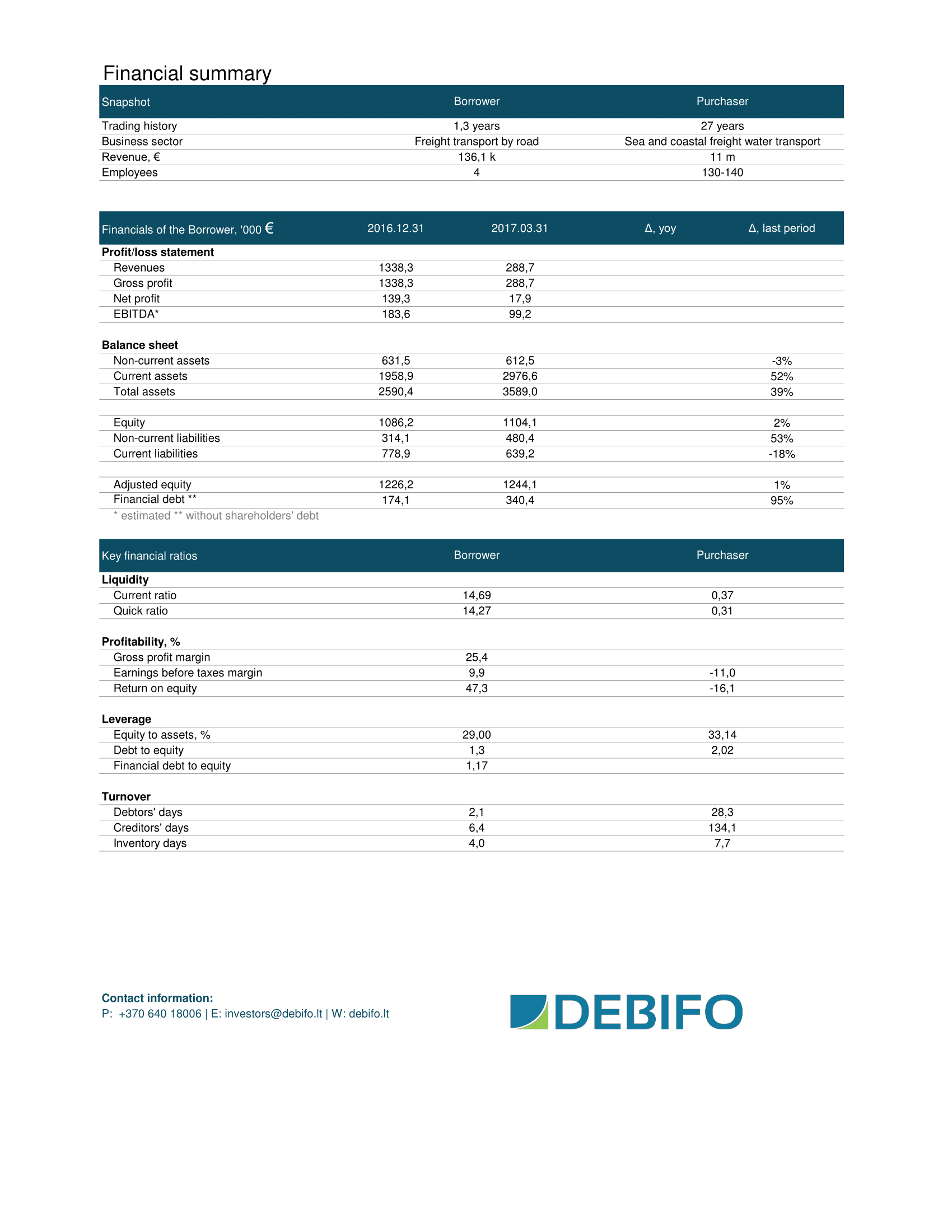

The borrowing companies (that borrow from our partners loan originators) and companies that pay for their invoices are well-known businesses that have been in operation for over 20 years. They have a steady stream of income, operate in a lot of countries, and they have proved to be reliable by borrowing and repaying the loans before. Companies that purchase their invoices are also well-known names in their field and they pay for the services they are provided on time. More info about both the borrower and the purchaser of the invoice can be found in ‘Under Asset description’ when you click ‘View’ on an asset bar.

Financial summary about the borrower and the purchaser of invoices

If you tend to invest manually and want to get a more detailed financial statement about a borrower, you should look at a financial summary that is often provided by a loan originator and placed in ‘Borrower and Under Asset Details’ window as an attached document. You can download the PDF file and check carefully the financial data, which is both about the borrower and the final buyer of the invoice. You may find some extra useful info that will help you to make up your mind regarding investment into a specific asset.

Why our loan originator prefers assets from Services companies

- They usually get one big bill at the end of the month (it means a company always stays cash positive)

- They provide a clear service, either done or not (clarity for lenders and loan originators if of utmost importance as clearly defined services will higher likelihood that invoices will be paid)

- Deferred payment terms are almost always applied (deferred payments typically range 30-90 days and the issued invoices serve as guarantees that the loans will be repaid)

Selected assets from the Services industry

Having outlined all the advantages of investing in the assets of the Services industry we would like to offer investors to add some of the assets from the industry to their portfolios. We have selected the top 2 assets to choose from. Both of them are from the company that has been in business for over 25 years and has over 100 thousand Euros in revenues. The purchaser of the invoices specializes in the transport of refrigerated cargo and container by own ships, with revenue above 11 million Euros.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Advantages of investing in short term loans

Advantages of investing in short term loans

A lot of small businesses, especially those that are seasonal in nature, often need short-term loans rather than long-term ones to have working capital for daily business needs, purchase goods, materials, inventory, and equipment, meet payrolls, or pay for services in order to function unobtrusively. They repay the loans in under a year, in most cases within the period of 90-120 days. As alternative lenders require less bureaucracy than traditional banks and finance loans much faster, small businesses can get necessary cash without making long-term commitments.

Not only businesses that borrow short term, but also investors that invest in those short-term loans gain a lot of benefits. The scope of the article is to look at some of them, give you a glimpse of how many of the benefits some of the biggest p2p lending platforms (Zopa, Mintos, Funding Circle, Lending Club, Assetz Capital) as well as Debitum Network have and also give our investors a special offer for investment.

What are some other advantages for investors to invest in short-term loans?

|

Less psychological stress |

Waiting for the maturity of a loan can be quite a psychological drag for any investor. Uncertainty about the outcome (possible default) causes significant stress and anxiety for many investors. Even with the safest platforms loans occasionally default and not knowing whether this or that loan may default is a serious disadvantage for investors that invest on p2p platforms that concentrate on long-term loans (1-5 years). Thus, short-term loans (from 1 to 5 months) is psychologically advantageous for an investor. One can easily imagine the impact of having invested for 3 years, waiting patiently through the period and finding out that the loan he has invested in has defaulted. And if the platform does not offer buyback guarantee for investors, all invested money would be lost.

|

Smaller likelihood of default |

It is likely, that if the borrower has been paying off a loan for 10 months out of 12, he will unlikely default on it if there are just 2 months left till the maturity. Thus, on Debitum Network, our partner loan originators (brokers) upload business loans that have a few months left till the maturity date (they have been issued and successfully been partly paid back before being listed on the platform). Borrowers have to prove that they are solvent and they do that by paying the bulk amount of loan before it is uploaded on our platform. Furthermore, most of the loans on Debitum Network are protected under broker’s buyback guarantee. So, even if these short-term loans default, investors will not lose any money, plus get back outstanding interest.

|

Smaller amounts to invest |

Loan amounts for short-term loans are typically smaller and thus investors can quickly finance those, while borrowers will most likely pay those out. It is far easier to pay off a loan of 5,000 Euros than the one for 50,000 Euros. The average loan amount on Debitum Network is 9,000 Euros. And as the minimum investment amount is just 10 Euros any investor can contribute to the financing of small businesses around the world and make attractive interest from day one.

|

Faster turnover of capital |

Faster movement of funds is another great advantage for investors investing their capital in short-term loans. One can diversify 100 Euros in 10 different loans of 2 months maturity, earn 7-11% annual interest and after successful repayment reinvest both principal and interest earned on previous investments. Investing in longer-term loans investor’s funds can get stuck in non-liquid assets. Investors investing on p2p platforms effectively become lenders themselves and often have to wait out the entire maturity term without the realistic possibility to get out of their positions, particularly if a platform does not offer a liquid secondary market for investors to sell their loans to other investors at discounted prices.

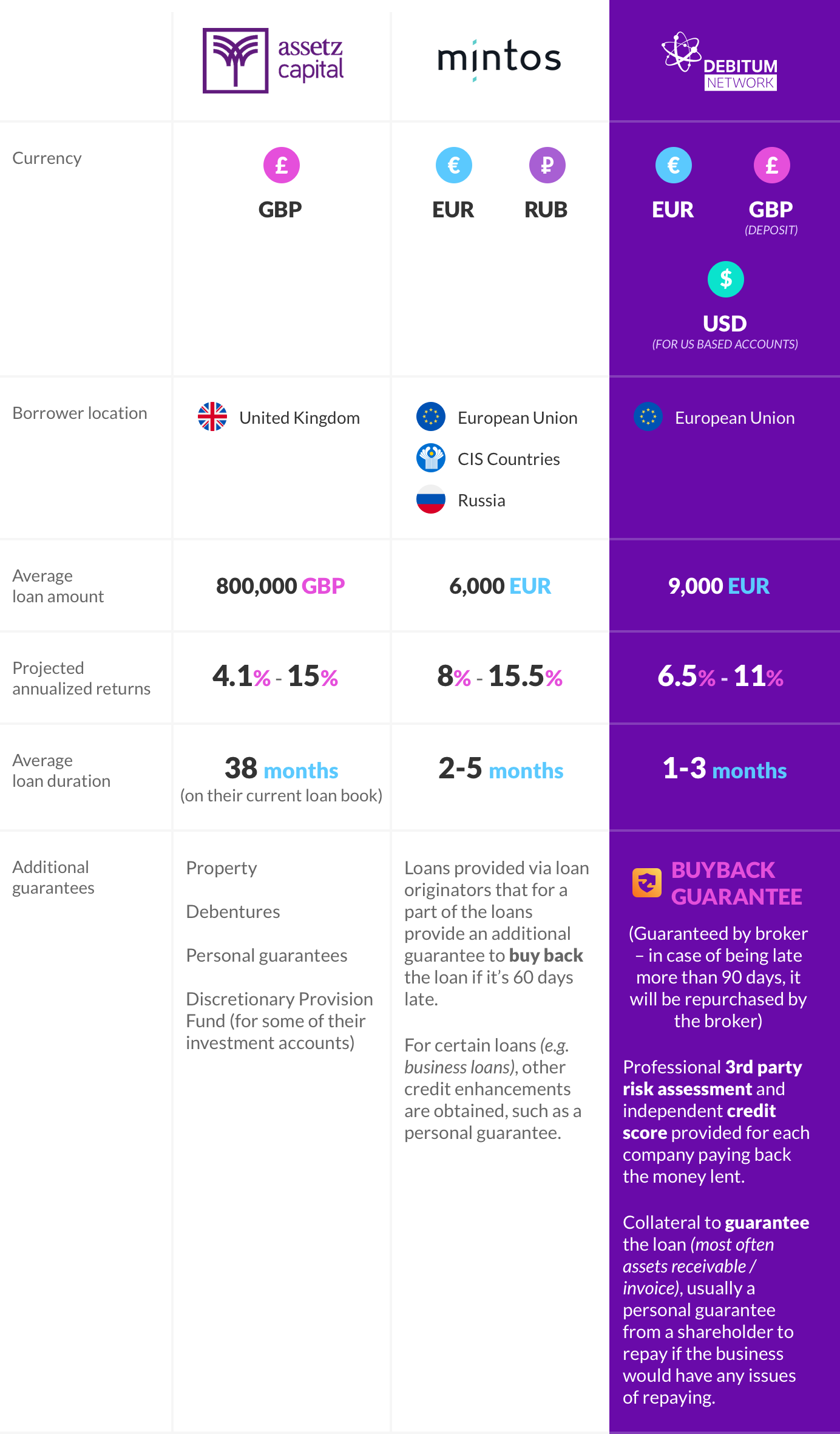

Having the above-mentioned advantages in mind, let us look at 3 players in p2p lending market Assetz Capital, Mintos and our own Debitum Network and see how they compare.

It is obvious from the table above that short-term loans (from 1 to 5 months) has become more popular with investors in recent years. No wonder Mintos has become a leading p2p lending platform in Europe. Short-term loans comprise the biggest amount of loans on their platform. Debitum Network is similar to Mintos in this regard as most loans on the platform are short term. Additionally, we have independent 3rd parties doing credit scores and risk monitoring options, thus potential investors can enjoy all of the advantages that short-term loans have over long-term ones in a transparent ecosystem.

Assetz Capital still remains one of the biggest alternative lending platforms in the UK surpassed only by Ratesetter and Zopa. Loans on their platform might be too long in duration for most investors who want a faster turnover of capital. Similarly, they do not have a buyback guarantee (loan originators are not obliged to buy back the loan if repayment is late by a specific number of days), even though other guarantees are in place.

Huge loan amounts (average of 800,000 Pounds for Assetz Capital) require participation from lots of investors to cover the full sum and may take a lot of time to implement. Having in mind that some loans may default, it would be a great disadvantage for those who have committed their capital in the loans to wait until maturity and, then, see a defaulted loan. From an investor’s point of view, it would be convenient to have smaller (5000 – 10000 Euros) and shorter-term loans (2 – 4 months) just as in the example with Debitum Network or Mintos, for the reasons discussed above.

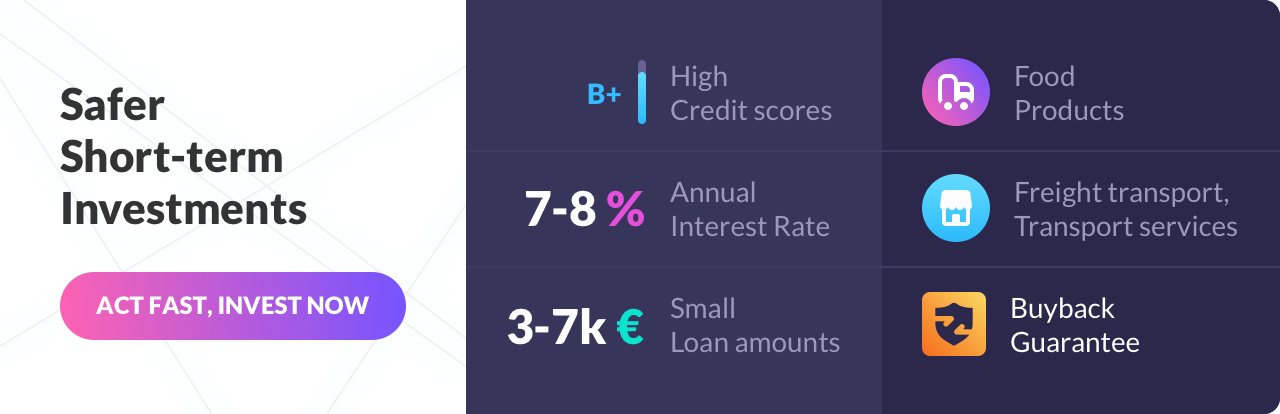

New short-term assets uploaded on Debitum Network platform

Debitum Network has been updated with new assets available for investment. This time we uploaded various assets of Food Products, Freight Transport & Transport Services companies. All new assets have buyback guarantees and a high credit score. They range from 3 to 7 thousand EUR, so hurry up and start your month by making an investment, which will bring you ROI within the next 40 days.

Check out our TOP 3 short-term assets recommended for investment!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What if the repayment is late?

What if the repayment is late?

Delayed and non-performing loans is an inevitability even on the safest p2p lending platforms. If an investor has a lot of loans in his portfolio, he will occasionally have a defaulted or delayed loan. Commercial banks typically have 1-2% percent of defaulted loans. Percentages with different loan originators or p2p platforms differ greatly: from 0.6% on Zopa to around 30% on Bondora. This is precisely the reason why investors must be careful while choosing a p2p platform to invest with.

Borrower’s default may be the biggest risk to an investor on a p2p platform. A delayed repayment on a loan can also be a cause for concern. Invested money may eventually be lost, and waiting for the positive outcome (for the borrower to repay the loan) can be quite a psychological drag as an uncertainty over the security of funds can erode investor’s trust in a given loan originator or a platform.

Buyback as a form of protection

Most of the p2p platforms or their brokers have implemented a buyback guarantee (the feature has been added on Debitum Network recently), which means that if any given loan is late by a specific number of days (typically from 30 to 120) the loan originator is obligated to buy back the loan and in most cases payback the accrued interest too (platforms differ on percentages of principal as well as interest they return). On Debitum Network, the investor is repaid outstanding principal and outstanding interest, but not an outstanding penalty (in case the repayment is late more than 90 days). Thus, if the investor is protected by a buyback guarantee a defaulted loan will not do significant damage to his overall returns. Additionally, loans placed on Debitum Network often have a guarantee from shareholders or are backed by assets (collateral). This strengthens the fact that invested money will be returned as the loan originator (broker) will have assets to sell and have the means to cover the losses incurred by investors from a specific loan.

Should you be worried if a loan is ‘Late’ on Debitum Network platform

As has been said, any given loan can be delayed. If you are an investor, this is a sign for a concern. However, nothing to be worried yet. Firstly, we differentiate loans that are under 15 days late. They fall under the ‘Grace period’ and no penalty is placed on the borrower, just the outstanding principal and interest.

‘Late’ (after Grace period) is a period when a penalty is calculated in addition to interest rate for each day being late (excluding Grace period), thus increasing the potential return for the investor, but also causing some worry as to “what if the loan will default?”

If you see a sign ‘Late’ under the Status section of our platform, there is no need to be concerned as our partner brokers have provided necessary buyback guarantees for investors.

However, let us go through the timeline of the lending process on our platform from the issuance of a loan till the repayment or the status of being ‘Late’, so that you may understand better what happens in each stage, how you are protected and whether you need to be worried.

This is the timeline of any loan uploaded on Debitum Network platform:

An example of an asset in ‘Grace period’

As has been said, the borrower usually has 15 days of ‘Grace period’ if he is overdue with the payment of the loan after the repayment date. He still has to pay back the principal and interest but does not get a penalty for being late.

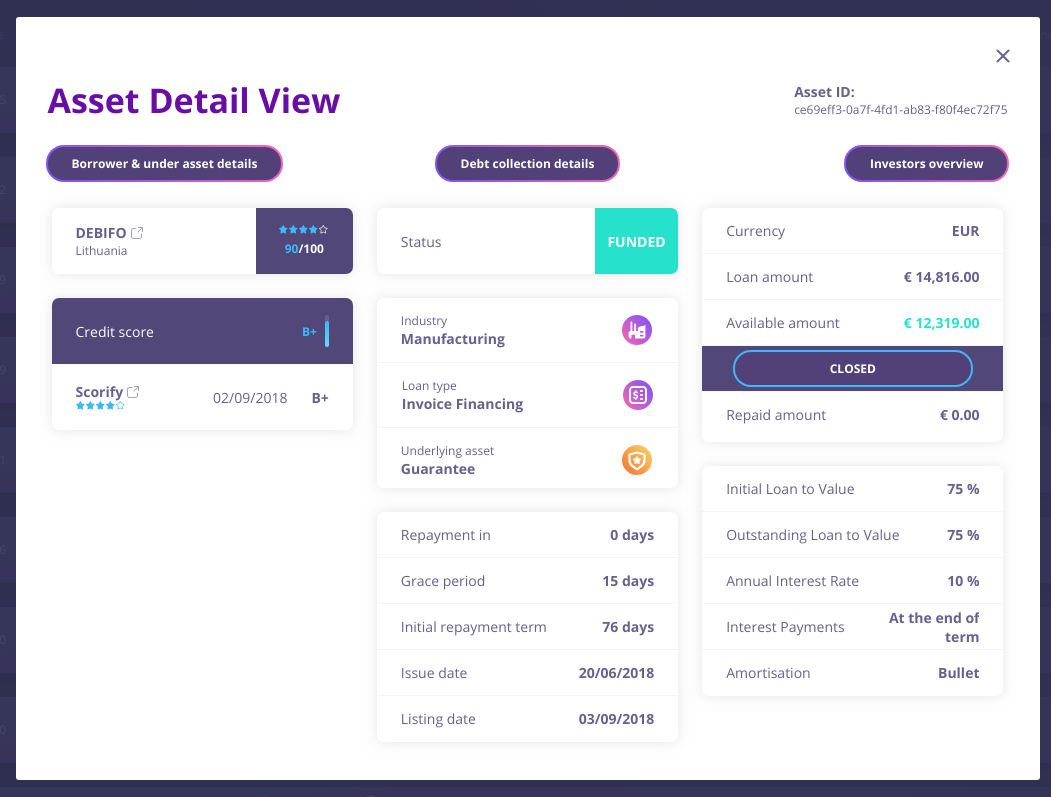

An investor can easily check the status of any given loan he has invested in on our platform. Having clicked ‘My investments’ button will load the list of all his/her current investments. One may spot that some of the loans are late, but still under grace period (typically 15 days). Below is the example of one. It has been in grace period for 10 days and has 5 days left, till the status changes to ‘Late’ (if not repaid by the end of 5 days). This borrower will have to pay both principal and interest, but no penalty yet. Having clicked ‘View’ button, an ‘Asset Detail View’ will pop up, where one can find more info about the loan and the borrower, how strong he is, whether he has borrowed before, borrower’s revenue amounts, years in business, or who the final payer for invoices is. This info should give more confidence for the investor as the loans on our platform are carefully handpicked and borrowers carefully assessed by loan originators. One should also remember that some industries undergo seasonality effect, where business generates less income and, therefore, some invoices may be paid slightly later. We will look at the ‘Asset Detail View’ window in our next example.

An example of an asset that is ‘Late’

Loans that have the status of ‘Late’ can be analyzed in the same fashion. An investor can click ‘My investments’ button and all the assets he has invested in will show up. Under the column ‘Status’ the investor can see which of the loans that he has invested in are ‘Late’. Below is an example of an asset, which is ‘Late’. The basic info about the asset one can find is: the industry, the broker, how many days it is late, what kind of loan it is, guarantee, invested and repaid amount, annual interest rate, credit score, outstanding interest, penalty increment, status, and ‘View’ icon.

More detailed info about the loan can be found by clicking ‘View’ button. This opens an ‘Asset Detail View’ window. There you will find such info as: when the asset is going to be repaid, grace period, initial repayment term, issue date, listing date, when interest is paid, amortization and more importantly ‘Borrower and Under Asset Details’. The window has more details about specifics of the industry borrower is in, how many years and what kind of guarantees are provided. Sometimes, a loan originator can provide more detail financial summary of the borrowers activity (attached document), which proves the ability of the borrower to pay back the loan in full. An investor should also remember that there have not been any defaulted loans on Debitum Network platform yet.

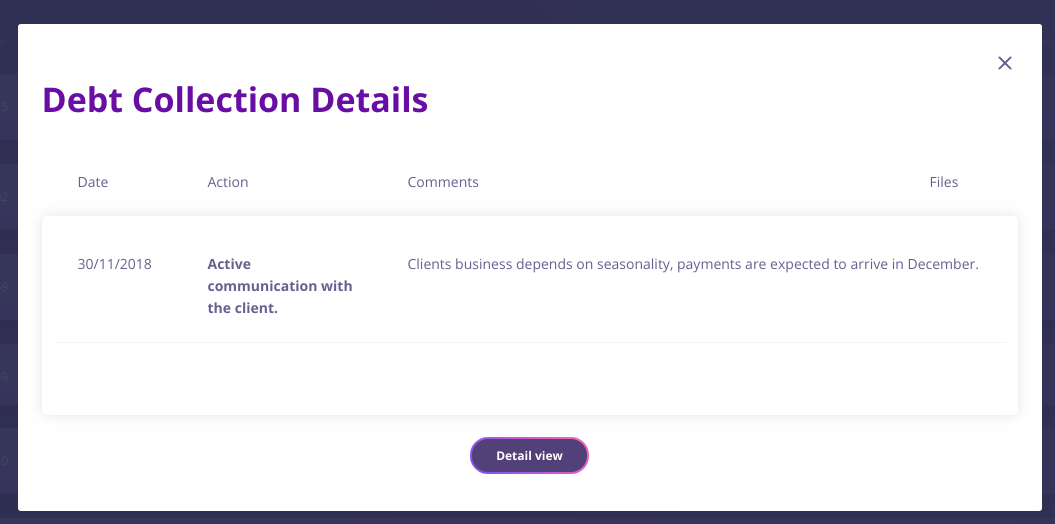

Debt collection – communication with late payers

‘Debt collection details’ button will bring you to the current status of the debt collection process. If the loan is late over 15 days (grace period is over), we talk to the broker who is in contact with the borrower and actively communicate with him to facilitate the smooth repayment of the loan. In ‘Comments’ section, you will find a comment with a likely reason for the repayment being late and when the payment is expected to arrive.

How can potential investors protect themselves?

Avoid lending platforms that do not have any security measures to protect investors’ money: buyback, collateral, personal guarantees. On Debitum Network, you are provided with all of the mentioned protective means for your funds.

Choose platforms that focus on short-term loans, because even when the loans are delayed, your money will not get stuck for long and a turnaround of capital will be much faster than with the ones that may keep your money stuck for 2 or more years. Waiting for 3 years for the payout and not getting one is not something a smart investor expects from his invested capital on p2p platform. Again, on Debitum Network, most of the loans are from 2 weeks to 3 months.

Check the default rates on platforms. Anything above 5% indicates the platform or the loan originator is not very skilled at filtering out problematic and selecting the safest loans for investors to invest in. No defaults have been on our platform yet, and our partner brokers keep defaulted loans under 2%.

Our offer for investors – invest in assets with a buyback guarantee

Investors that want to invest in exclusively safe assets can do so on Debitum Network. Our offer for them is to choose assets that have a buyback guarantee from a broker. If one invests in those and they are late with repayment more than 90 days, the broker is obligated to buy the loan with outstanding principal and interest. Thus, investors’ funds always remain protected under the buyback guarantee and he does not have to worry about late or defaulted loans anymore. The buyback icon is magnified in the asset bar below. Check for the icon if you want to invest in the assets protected under the buyback guarantee.

Join our platform and start investing

The interest in Debitum Network platform has been rising steadily. Investors onboard and invest in short-term loans every week. You can also sign up on the platform at any time and participate by helping small businesses around the world grow. You will earn attractive interest at the same time.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Attractive European logistics industry’s assets to invest in

Attractive European logistics industry’s assets to invest in

Importance of logistics for business

It would be impossible for the current world to exist without goods or objects delivered or transported between places. Logistics is a part of supply chain management; it plans, implements and controls the flow and storage of goods and services in order to meet customer’s requirements. Logistics management might be the underlying factor in the success of any company’s operations and outperforming of competitors. Logistics is crucial to the distribution industry, as it makes the distribution of goods fast and efficient.

The transport and logistics industry is made up of six industry sectors making it one of the largest industries in the world and since it largely correlates with other industries, particularly manufacturing, the growth of logistics is positively reflected on the growth of an economy as a whole. Expansion in logistics sector accelerates the optimization and adjustment of the industrial structure, advances the transformation of economic growth, and thus promotes a rapid economic development.

Europe – the hub of world logistics

Logistics is widely considered one of the main engines of the European economy too. It helps create industrial value by the movement of goods and cooperation among companies and is one of the key industries in job creation. Logistics sector comprises around 14% of GDP of the European economy and has been one of the fastest growing economic industry of EU. Total goods transported in the European Union are estimated at 4 billion tkm (1 tkm is 1,000 kgkm and a kgkm means moving 1 kg of cargo a distance of 1 km). More than 11 million people are employed in the European logistics sector.

LPI index published on the World Bank website indicates that 8 out of 10 top performing countries in logistics around the globe are European countries.

As Lithuania, Estonia and Latvia have the main routes of logistics connecting Russia to Western Europe, the two countries are climbing in the chart and currently take 54, 36 and 70 positions in the field. No wonder the above mentioned facts make investing in logistics (in Europe) an attractive opportunity. However, those opportunities in the industry come with challenges and risk.

Innovative technologies create sharp competition and costs remain an impediment for the industry

Implementation of new technologies and automation in logistics creates obvious advantages for local service providers, but may force the ones that do not have money to invest in technologies out of business. As around 14% of companies outsource their logistics services, competition for the market share becomes even more fierce.

Furthermore, personnel, fuel/energy and real estate costs in particular, as well as interests, and leasing showed significant increase throughout the decade in the industry, new entrants in the market as well as introduction of robotics drove prices down, thus reducing the competitiveness of smaller companies and even forcing some of the players out. This leads us to the conclusion that investing in the field requires careful selection and weeding out the weak performers as well as choosing the best companies. Picking random assets is far from effective strategy here.

Comparison of assets from logistics by different loan originators

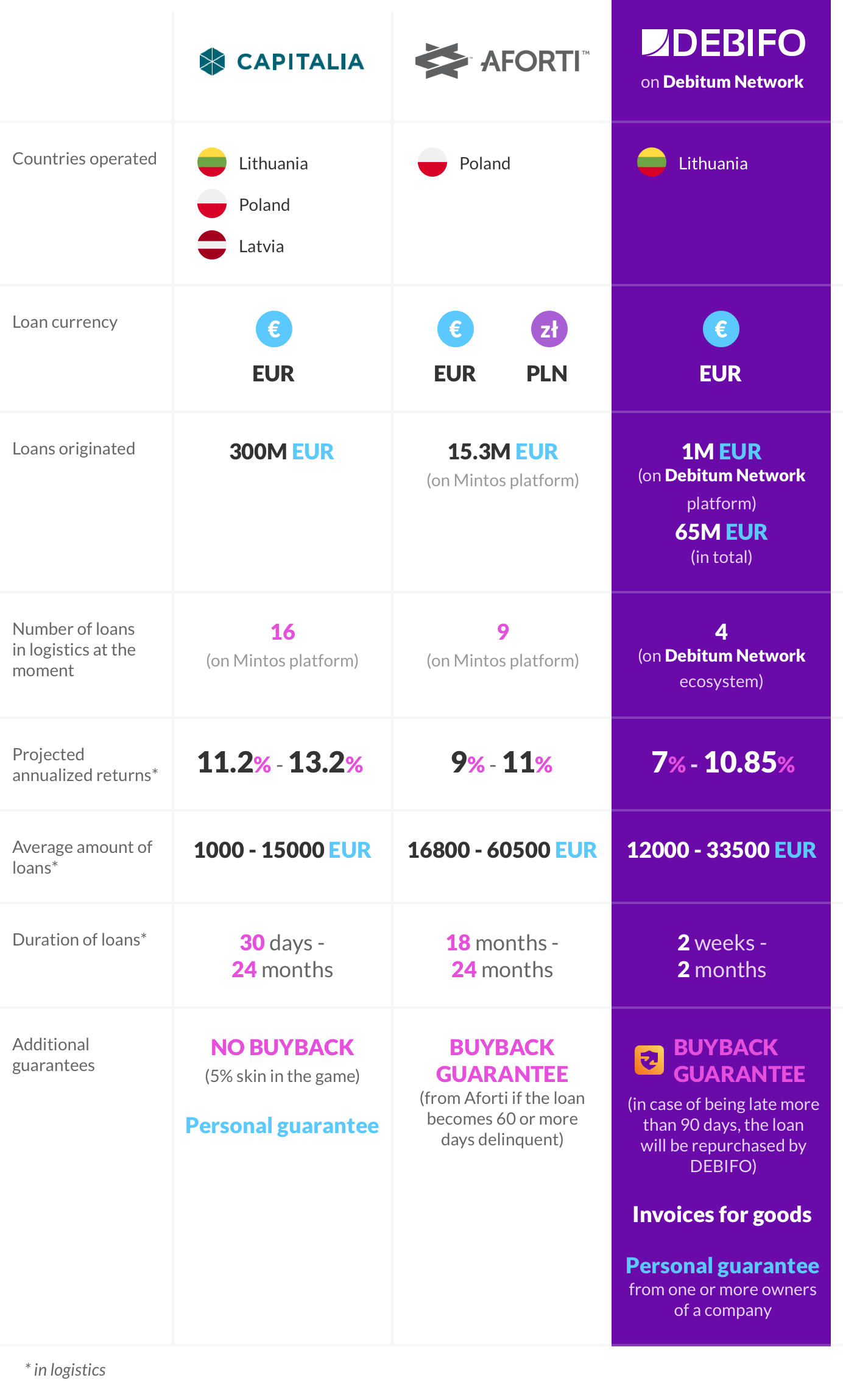

Bearing in mind both opportunities and risks involved in investing in the industry, let us look at some of the loans in logistics from loan originators that upload their loans from the industry of logistics on Mintos platform. We singled out Capitalia and Aforti that operate in related European countries as Debitum Network. The third player is DEBIFO that in addition provides its assets via our own Debitum Network.

We see logistics not only as a very promising industry to invest but also a very competitive one, where sharp competition drives logistics companies out of business, thus making investing in random companies of the sector risky. Attractive interest rates without a buyback guarantee will likely significantly reduce average return for investors as bankruptcies in the respective field happen from time to time. Thus, a buyback guarantee offered from a broker is a sign that a broker is willing to take full responsibility in case of bankruptcy and not leave the losses for investors to cover.

A faster turnover of capital should be viewed as a plus as opposed to investing in loans with a duration of 12 months or more. Debitum Network accepts loans that have a much shorter maturity date, which also significantly reduces the possibility of default and reduces psychological stress for those who have invested in the assets. Plus, if the company has been paying off the loan for a year, statistics show that the risk of a company to go bankrupt reduces significantly for the last few months before the final repayment date.

Why is logistics industry attractive for Debifo?

- The invoice amounts are relatively small 5,000-34,000 Euros.

- Our customers’ main logistics operations are export from Lithuania to Western Europe.

- Large and strong European buyers that will pay for invoices.

- Freight is mostly insured or is insurable.

- Owners have strong ambitions to grow.

- Owners accept somewhat higher interest rates from alternative lenders.

What are the benefits for investors?

- Assets in logistics on Debitum Network platform will pay 7-11% per annum.

- The loans are issued to businesses that have been in business (on average) for 9 years and the loans are backed by an accepted invoice from large corporations with an average revenue of 700 million EUR. In addition, there are private guarantees, usually from two or more shareholders of a company and also a buyback guarantee from the broker.

- Repayment days are from 2 weeks to 2 months. You start earning interest since day one.

- You can invest flexible amounts, starting from 10 EUR per asset.

- You can invest even if the date of repayment is a few days away.

- More loans from European businesses in logistics coming soon.

Got interested? Why don’t you try our platform for yourself!

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.