Tag: credit score

Why we use independent risk assessment parties

Why we use independent risk assessment parties

We believe that qualitative risk assessment is a crucial risk prevention measure for investment assets on Debitum Network. Finding a balance between risk and reward is the ultimate target for most investors. You should know that not all risk scoring methods used by alternative investment platforms are created equal, and some are more advantageous than others. Debitum Network risk scoring model could be the best. Why? Spare 5 minutes of your time and find out.

Debitum Network is the only platform to use independent risk assessors

That’s right. Debitum Network, from the very start, decided to use independent and professional third parties who do risk scoring for the borrowers and assets on our platform. Other platforms implement their own risk scoring. Thus, besides connecting borrowers to investors, they also try to do a professional risk assessment, which requires resources, databases, and knowledge of the market. We find that a generic risk scoring model is often ineffective and can often be manipulated.

Independent risk assessors increase transparency

Investors deserve to know the real situation of the borrower before he invests. If a platform does risk scoring themselves, they can manipulate the score to their advantage. They can give better rates to worse performing companies or inflate the scores for better-performing ones. Thus, inside risk scoring may mislead investors, giving them incorrect information about the real state of a borrowing company.

Local risk assessors know the market and their companies better

We upload assets from a borrowing company that resides in an x country. We also search for a local risk assessor who would provide a professional risk scoring for that specific company. Local risk assessors know local businesses and their specifics, and thus, they can evaluate companies applying for a loan with much better precision. It far outmatches any other generic risk scoring algorithm done by a loan originator or a P2P platform itself.

Independent risk assessment is an additional safeguard for investors’ funds

Risk assessors have access to tax and financial databases where they can find the real financial state of a borrowing company, and thus give an adequate rating to it. Therefore, if a company is seriously over-indebted, this would be reflected in a credit score. Then, investors would be able to decide whether to invest in the loan or not.

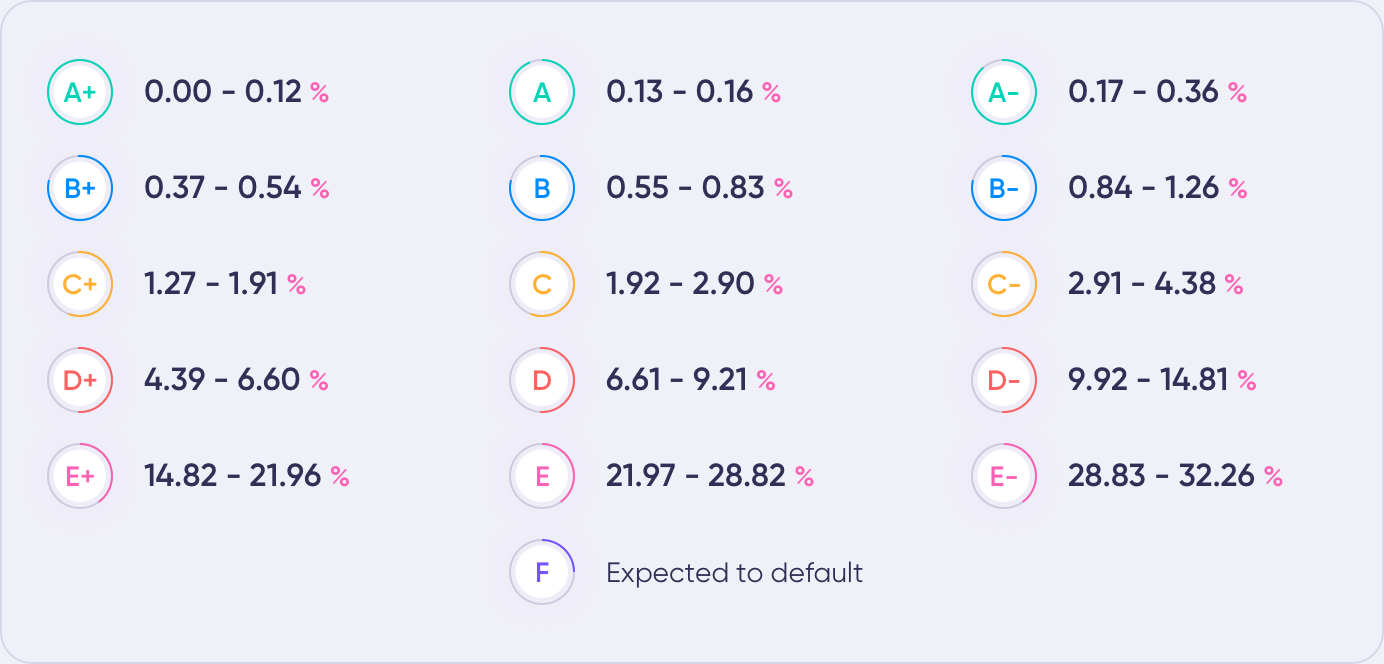

Ranges of credit scores on Debitum Network

Credit scores used on Debitum Network have been assigned based on a standardized probability of default of the business during the next 12 months. Debitum Network has aligned credit scores received from different risk assessors to fit in the same unified scale. The chart table below indicates the probability of default on loan based on historical events by a large number of businesses worldwide and might be inaccurate for a particular group of companies (and their loans) on Debitum Network.

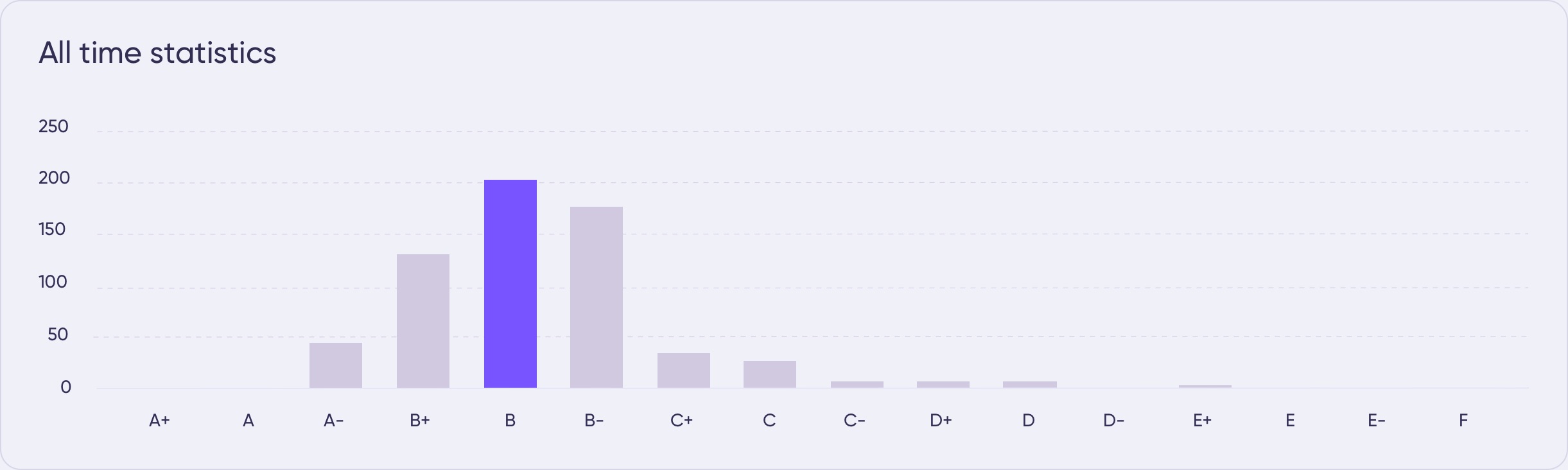

Most of the assets on Debitum Network have B, B-, or B+ ratings. We reject most of the loans below C (D-F) as these ratings indicate that the likelihood of a borrower to go broke within the next 12 months if very high. A to C ratings show that the probability of bankruptcy is very low. There have been a few assets on the platform with a score of D-E. They are placed on the platform as the borrowers pledged collateral as a guarantee, and the broker offers a buyback guarantee for the asset. Thus, the safety of investing in the assets is increased to the maximum. Refer to the statistics bar regarding historic ratings on Debitum Network.

Want to invest in high score assets?

Most of the assets on Debitum Network have excellent risk scores. We have selected a special one for you this week. Take a look, and if you like what you see, invest right away. Do not hesitate, as assets are funded very fast. You don’t want to stay behind. The borrowing company is engaged in the manufacturing of malt, it has been in business for more than 17 years, employs more than 60 people, and has revenues of over 13 million EUR. The purchaser is a beer manufacturer that employs more than 330 people, has revenues of over 58 million EUR, and has been in business for more than 26 years.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Why Credit scores for municipalities are so low and should they be

Why Credit scores for municipalities are so low and should they be

Risk assessors give businesses that come for a loan a credit score. It is a rating that provides a conclusion on your business credit reports. The credit score helps lenders understand the strength of your business model, how responsible and committed you are to achieve your business goals, and whether your company can make payments on time. So, this rating either increases your opportunity to get a loan or decreases it.

We, at Debitum Network, aim to be a decentralized lending platform, where investors, borrowers and third party service providers (risk assessment, insurance, and debt collection) all participate in the lending process responsibly. Credit score on our platform is provided by a trustworthy credit rating agency for each market, for example, by Scorify for Lithuanian businesses.

Debitum Network credit score

Credit scores used on Debitum Network have been assigned based on a standardized probability of default of the business during the next 12 months. Debitum Network has aligned credit scores received from different risk assessors to fit in the same unified scale. Below is the table with specific credit scores used on our platform.

| Credit Score in a letter rating | Credit Score in a 100 point scale | Probability of default within 12 months |

|

100 – 80 | 0.00% – 0.12% |

|

79 – 73 | 0.13% – 0.16% |

|

72 – 69 | 0.17% – 0.31% |

|

68 – 67 | 0.37% – 0.46% |

|

66 – 65 | 0.55% – 0.70% |

|

64 – 63 | 0.84% – 1.06% |

|

62 – 61 | 1.27% – 1.60% |

|

60 – 59 | 1.92% -2.42% |

|

58 – 57 | 2.91% – 3.65% |

|

56 – 55 | 4.39% – 5.50% |

|

54 – 53 | 6.61% – 8.27% |

|

52 – 51 | 9.92% – 12.37% |

|

50 – 49 | 14.82% – 18.39% |

|

48 – 47 | 21.97% – 25.40% |

|

46 – 45 | 28.83% – 32.26% |

|

44 – 0 |

Expected to default |

Be aware that above indicated probability of defaulting on a loan is based on historic events by a large number of businesses – it might be inaccurate for the particular group of businesses (and their loans) on Debitum Network.

Why sometimes credit scoring tools fail?

Regular credit scoring tools fail when assessing the credit worthiness of governmental institutions. Credit scores are derived from national statistics about the economic sector of the company, number of employees, taxes paid to the government, debts that the company has, judicial problems that the company faced, the money that is owed to the company, who are the counterparties and any other financial information, ratios, sales, turnover etc.

The problem occurs when you think about it from a perspective of a governmental institution. Local municipalities and other governmental entities have a lot of this kind of information missing as the government is not a private company owned by a few shareholders. So, the only thing left is to look at the financial information or any information regarding judicial problems and financial information available and thus the credit score provided comes only from that.

Public institutions are not cash positive. In fact, in Lithuania, even ‘Vilnius City Municipality’ which receives most taxes keeps on receiving more and more money from the central government every year (https://www.vz.lt/verslo-aplinka/2018/01/17/vilniaus-biudzetas-siemet–didesnis-nei-pernai-bet-vis-dar-deficitinis). Because of this, looking just at the financials and the judicial information of municipality yields and the wrong results it one may understand why credit scoring models give municipalities such low credit scores.

However, no municipality or public institution has gone bankrupt even during the last crisis of 2008. Obviously, because they are funded by taxpayers money and live on a governmental budget. Taking the above said into account, we can clearly state that municipalities and governmental organizations are strong payers and can be relied upon.

How is this important to Debitum Network?

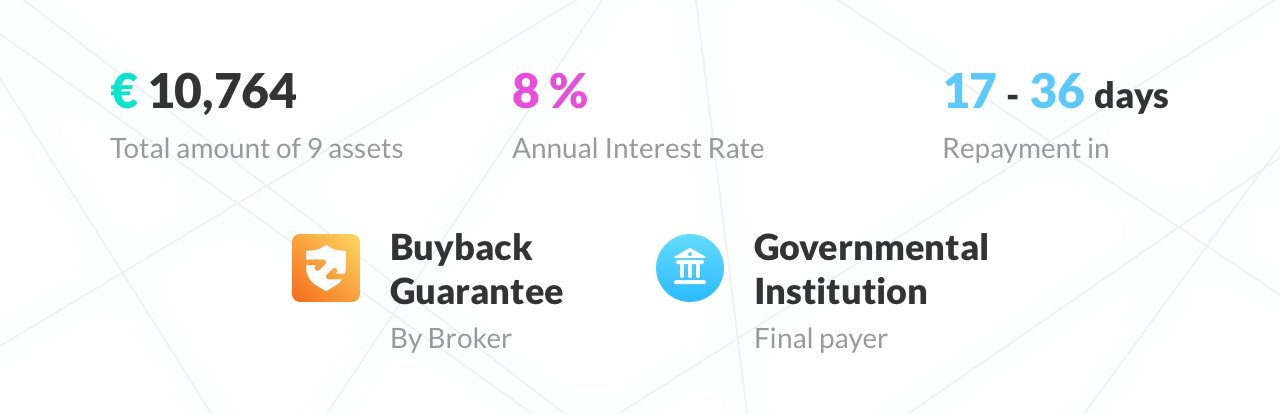

On 2018-11-07 Debitum Network received the first assets that have municipalities and they have their credit risks checked. The scores showed that the assets are Aggressive (i.e. only people that like risk should invest into these assets). But governmental institutions are some of the best payers on the Lithuanian market as they are backed by the Lithuanian government. So, they are unlikely to default. This leads us to the conclusion that any conservative investor can select investing in loans that will eventually be paid off by governmental institutions. Therefore, from now on, we give all the assets tied to governmental institutions a country credit score for that specific country, in this case for Lithuania it is A-.

A group of assets we offer to add to your briefcase

We have a special offer for you to invest in a short term and low risk loans for small business that offers their services for governmental institutions. The loans are issued for the company that has been providing architectural services since 2000 and the buyer of the services is one of municipalities of Lithuania. There currently are 9 assets of the kind and the total amount of invoices is just 10,764 Euros.

We are inviting those who are interested to act now.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Why is credit score important (updated)

Why is credit score important (updated)

Lending institutions give businesses that come for a loan a credit score. It is a number that provides a conclusion on your business credit reports. The credit score helps lenders understand the strength of your business model, how responsible and committed you are to achieve your business goals, and whether your company has the ability to make payments on time. So, this number either increases your opportunity to get a loan or decreases it.

An interesting fact for you to chew on; research shows that most startup businesses fail within the first 3 years of business, not because they lack abilities, talents, or a poor business plan, but because they have limited access to funding.

Typical Range for credit score

Credit scores for businesses may vary with different lenders, but the most usual range is 1-100. The higher the score, the better for business it is to get a loan as it means the company is not regarded as a risky one to lend to. 80 or higher is considered to be excellent.

An example of how a rating agency can rate risks based on specific credit scores:

A score of 1–69 indicates a high risk of late payment, 70–79 indicates moderate risk, and 80–100 represents a low risk.

Debitum Network credit score (old scoring system)

On Debitum Network platform Abra 1.0 assets can be filtered according to three categories and you can form your briefcase accordingly.

Just for the sake of giving you an example (numbers are for illustration purposes), which credit score category a specific number would go to:

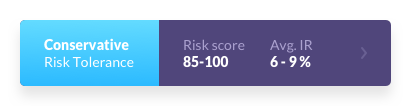

- 85-100 would mean conservative

- 71-84 would mean moderate

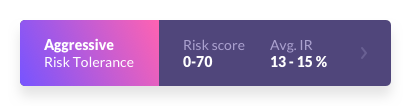

- 0-70 would mean aggressive

Credit score system updated. New scoring system took effect on the 14th of November.

| Credit Score in a letter rating | Credit Score in a 100 point scale | Probability of default within 12 months |

|

100 – 80 | 0.00% – 0.12% |

|

79 – 73 | 0.13% – 0.16% |

|

72 – 69 | 0.17% – 0.31% |

|

68 – 67 | 0.37% – 0.46% |

|

66 – 65 | 0.55% – 0.70% |

|

64 – 63 | 0.84% – 1.06% |

|

62 – 61 | 1.27% – 1.60% |

|

60 – 59 | 1.92% -2.42% |

|

58 – 57 | 2.91% – 3.65% |

|

56 – 55 | 4.39% – 5.50% |

|

54 – 53 | 6.61% – 8.27% |

|

52 – 51 | 9.92% – 12.37% |

|

50 – 49 | 14.82% – 18.39% |

|

48 – 47 | 21.97% – 25.40% |

|

46 – 45 | 28.83% – 32.26% |

|

44 – 0 |

Expected to default |

Advantages of having a good credit score:

- Your business helps you to have a good image with your business partners, suppliers, investors, and lenders

- You can easier qualify for business loans as well as growth and expansion and borrow more

- You can get business loans at lower interest rates and save you money

- It can possibly get lower insurance premiums

- You may get business loans without signing a personal guarantee for any debts your business cannot pay

- It protects your personal credit.

Some of the negative things that may negatively impact your business credit score:

- Property arrests of a company make the company look riskier and decreases credit score as a result

- Companies that show court records (even one) have a risk of getting their credit scores reduced

- Having a high number of claims or lenders results in higher risk and consequently, lower credit score.

- Insolvency private individuals or managers of a company will likely push credit score down.

The main methods to improve your credit score:

- You have to separate business and personal finances

- Get a business credit card, start building a line of credit

- Choose business partners and lenders who will report your good payments to business credit agencies

- Pay your bills and payments to creditors on time or better early

- Do not exceed your credit utilization ratio by 30 percent

- Have a habit of checking your credit report and correct any mistakes/errors in it.

Debitum Network Platform Abra 1.0 is Live!

On the 3rd of September, we reached a significant milestone on our roadmap and delivered the first version of our platform Abra 1.0.

It does not matter whether you are a conservative, moderate or aggressive investor, you will find assets according to your risk tolerance and be able to invest for an average annual return of 7-11%.

Small businesses can register on our platform and borrow from 10,000 EUR to 1 million EUR.

Service providers can sell their services of risk assessment and debt collection to clients all over the globe for an attractive compensation.

Ready to invest?

New functions that help filter assets on Debitum Network platform

New functions that help filter assets on Debitum Network platform (Updated)

Our global lending platform Abra 1.0 launches on the 3rd of September. After the launch, investors from around the world can start onboarding, and, after authentication, begin investing in available assets.

Credit score and interest rate

Investment assets are loans and they are categorized or filtered according to credit score and an average interest rate for a specific period. These will be key filters, which an investor may use while selecting which assets to invest in. More risk-averse investors will probably concentrate on less risky assets and earn lower interest, while more aggressive ones will be able to choose riskier assets with considerably higher interest rates.

So, each asset or a group of assets, that you may want to own will show you the credit score and an average interest rate that you are going to make if you invest in those specific assets.

An investor should know, that the higher the risk score, the lower the risk and the lower the interest rate. The lower the credit score, the higher the risk and the higher annual interest rate.

Credit score will vary from 0-100, with 0 being the worst score, and 100 the best.

On Debitum Network platform, an investor will be able to see all available assets and filter them out according to a specific set of data.

Available portfolios

Assets will fall into following categories according to credit score and an average interest rate:

When you press portfolio, you can filter out the assets you want to omit and see only a specific category of assets, e.g., conservative. So, let’s say, there are 200 available assets. You press conservative portfolio, and you will get all the assets (let’s say 35) that are under this specific credit score category.

You press, moderate portfolio, and you get all the assets under this credit score category. Eventually, you can do that with assets that belong to the aggressive type of portfolio.

Alternatively, you can click on any specific asset manually and see its’ credit category and expected interest rate for a specific period of time loan is provided for.

Update of credit scores

Last November, we moved from risk categories expressed in numbers 1-100 to a better system of letters A+ – F removing any doubts for users which score is good 1 or 100, and widening the choice for selection and better defines risk category as well as percentage of likelihood of a default as described in this blog post.

Ready to start investing?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.