Tag: Debitum Network

Buyback guarantee and its’ importance in online lending

Buyback guarantee and its’ importance in online lending

In P2P and P2B lending platforms a buyback guarantee is a guarantee provided by a loan originator regarding a specific loan. If repayment of that particular loan is delayed by more than a specified number of days (typically from 30 to 180), then the broker (loan originator) is obligated to buy back the loan by fully or partly compensating investors for their remaining principal invested as well as outstanding interest. Platforms differ on the percentage of principal returned and the amount of interest paid.

In a way, it resembles an insurance system, albeit for loans on p2p platforms. Thus, if the borrower fails to pay off the loan in time, it will be bought by the broker (loan originator), so the investor will not lose the money and in most cases, the accrued interest will be returned too.

How investors get liquidity in online lending?

Understanding how investors get liquidity is important as on some platforms loan maturity for loans may be a few years and if investors on those platforms invest in loans, they effectively become longer-term lenders themselves. As in most cases, they cannot get out of their positions and access their capital in a predefined time of the loan by agreement, any investor would want to know how liquid the assets he invests in are and if his capital is protected in case the borrower defaults.

Sure, certain platforms offer a secondary market as a viable option for investors to sell their stake in loans. At the time of writing only 29% of all investors on one of the largest European p2p platforms, Mintos, have made at least one investment via the secondary market. In addition, there are around 2 times as many assets available on the secondary market compared to the primary market over there. It seems that other investors on the same platform are not so keen to buy late and long loans from their fellow investors. Hence such option adds value and liquidity but is not a silver bullet and we have to go back to brokers (loan originators) for liquidity solutions.

A broker (loan originator) should have enough equity to be able to take a loss on a late or defaulting loan. Institutional investors who provide a larger amount of funding to lending companies usually request that the leverage on equity is not more than 4-10 times. Meaning that for each 1 million EUR of a loan portfolio, a broker (loan originator) would have between 100k-250k EUR in equity. What does it mean? It means that if 5% of all loans default, a lending company can still cover all losses from their equity and continue their operations.

So, a lending company with a healthy equity vs portfolio ratio is a choice trusted by institutional investors managing large funds and most likely is a better liquidity provider for a final investor in a loan if compared to a secondary market on the same lending platform.

Do high-interest rates compensate risks and absence of buyback guarantee?

Some platforms, such as Bondora bypass loan originators and keep all interest to themselves without offering any buyback guarantee. They offer plenty of high interest (30-200%) high-risk loans. A high percentage of them will default. You have to be a very picky investor in order to figure out, which loans are worthwhile investing and you will find out that the expected returns hardly ever become real ones. Statistics that Bondora have shared with their users shows that around 25% of investors on their platform have suffered losses, and have not made profit.

Loan originators on Mintos and Twino platforms offer buyback guarantee after the loans are not repaid 60 and 30 days after maturity term. On our own Debitum Network, the brokers would buy back a loan if the repayment of the loan is late more than 90 days. The best part is that the brokers pay not only the principal but also the interest, which makes investing in the offered loans seemingly risk-free. Interest rates on these platforms are relatively lower than on Bondora or on platforms that offer payday loans to invest in.

Let’s look at some data of the most popular platforms around Twino and Bondora as well as our Debitum Network and try to figure well they fare protecting investors’ capital, what security measures they measure and a few other pieces of data:

From the table above we may draw a number of conclusions. Firstly, high-interest rates without a buyback guarantee will not deliver expected or promised returns as the number of defaults on these type of platforms (e.g. Bondora) is very high and most investors actually lose money as selecting loans that will actually be paid off by the borrower is inexplicably difficult.

If businesses or people are able to borrow at smaller interest rates, there is a higher probability that they will repay the loans, as opposed to borrowing at high interest rates that exceed 30% annually. Smaller interest rates will likely have smaller expected returns, but as the rate of defaults is much smaller, the real net return will be higher than with loans that have very high-interest rates and no buyback guarantee.

Shorter term loans effectively decrease your risk. What is the logic behind it? Very simple! If the company has been paying interest for the whole year, it will most likely not default if there are a couple of months left. This is one of the reasons why Debitum Network focuses on short-term loans for SMEs. We see that offering investors to invest in 1-3 months duration loans carries less risk and psychological pressure for them than keeping funds locked for a year or more with limited possibilities to exit the position.

Do buybacks eliminate risk completely or how can investors protect themselves?

A loan originator may go bankrupt and in that case, your money invested in the loans of the originator will most likely be lost. Eurocent loan originator went bankrupt and the loans it put on Mintos platform defaulted, thus causing investors to lose money on both principal and interest (Mintos doing their best to get the investors’ money back). Thus again, a buyback guarantee is as good as the company behind it.

Investors could choose only loans that have a buyback guarantee from a broker. It would be wise to choose only those that offer the option of buyback even at the expense of getting smaller interest rates. You want as much clarity from platforms and brokers operating on them regarding buybacks too. In March 2017 Twino introduced ‘payment guarantees’ rather than buyback guarantees. This change means that investors are now left owning non-performing loans for up to 2 years, and relying on Twino to make the payments due. The loans cannot be sold on the platform. Thus liquidity for investors dries up and investors have to wait for years until the money is eventually returned in case of default.

Spreading your investments in different loans and possibly different loan originators or even platforms is one of the options as diversification significantly reduces risk due to the fact that an investor ‘does not keep all eggs in one basket’. Asset-backed p2p or p2b loans are also a form of insurance as in case of a borrower’s default an asset can be sold and investors’ money paid back. Smaller interest rates for businesses is an advantage too. If borrowers are charged smaller interest rates they have a higher chance of repaying it rather than defaulting as they would if they were charged some rates from 30-50% annually or more. In the same fashion, collecting payments on an asset-backed business loan is simpler and usually faster than collect them from a bankrupt private person who defaulted on a payday loan issued by some payday loans’ platform. Thus, Debitum Network can proudly go shoulder to shoulder with long seasoned p2p platforms such as: Funding Circle, Lending Club, Zopa, Assetz Capital, Fellow Finance, Grupper, October, Ratesetter, FundingSecure, Lendy, MoneyThing and etc.

Investing with Debitum Network

Short-term loans with maturity mostly from 1 to 3 months, interest rates from 7 to 10.85% and a buyback guarantee is an offer from Debitum Network to investors on our platform. This enables investors to gain a number of things: earn attractive interest, have a fast turnover of their capital (1-3 months) and by means of buyback guarantee to protect their investments as much as possible.

Got interested? Try DEBITUM NETWORK!

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Debitum platform update: April statistics (2022)

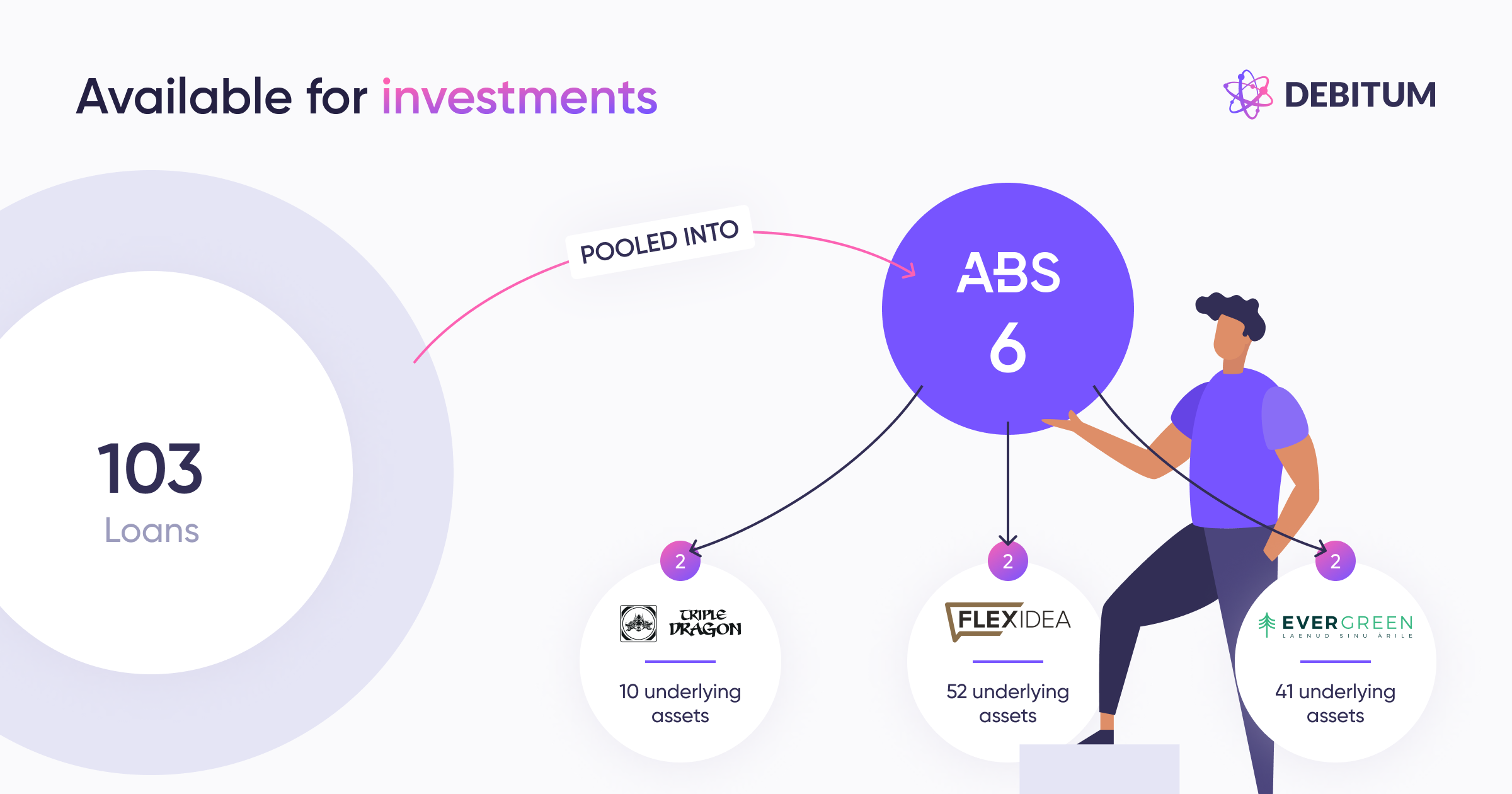

Number of assets (loans) pooled into number of Asset-Backed Securities from which Loan Originator

TRIPLE DRAGON has 10 underlying assets, FLEXIDEA has 52 underlying assets, EVERGREEN CAPITAL has 41 underlying assets.

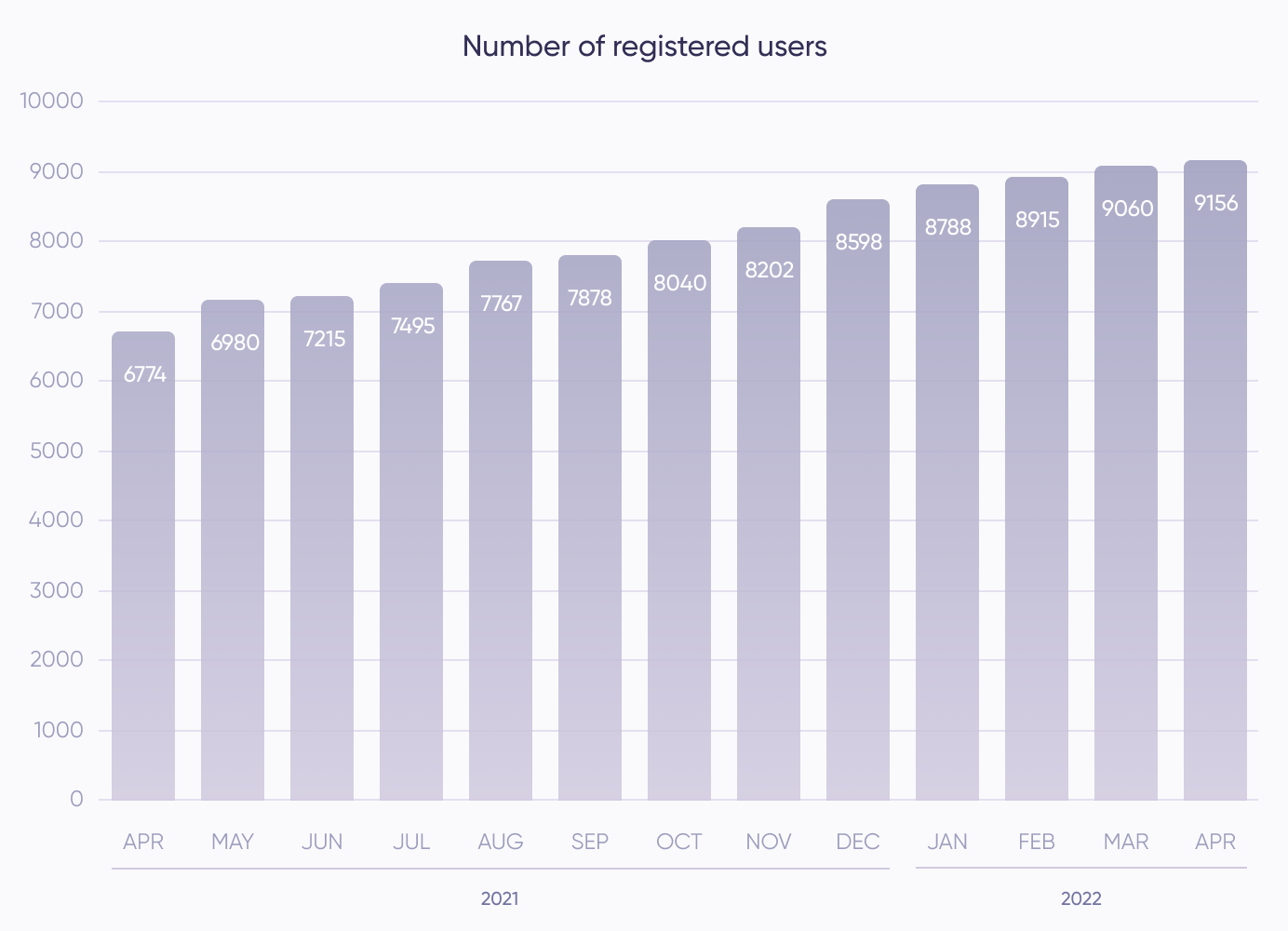

The number of registered users (activated)

In April we have reached 9156 registered users.

Compared to March the number of registered users in April has grown by 96 users (1%). Compared to April 2021 number of registered users in April 2022 has grown by 2382 users (35%).

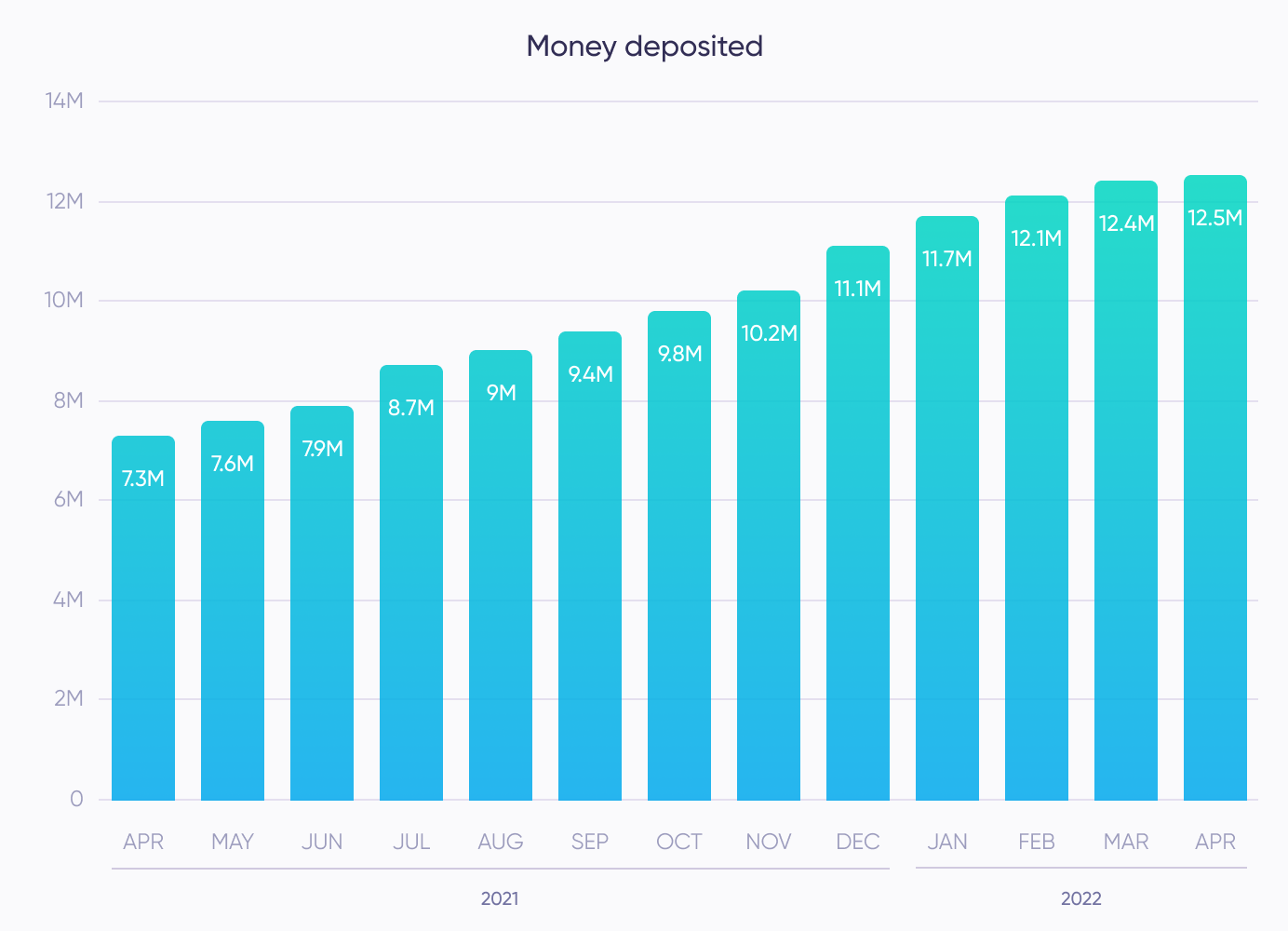

Money deposited

In April, we have reached 12.5 mil. € of deposited funds.

Compared to March the money deposited in April has grown by 0.1 mil. (1%). Compared to April 2021 money deposited in 2022 has grown by 5.2 mil. (71%).

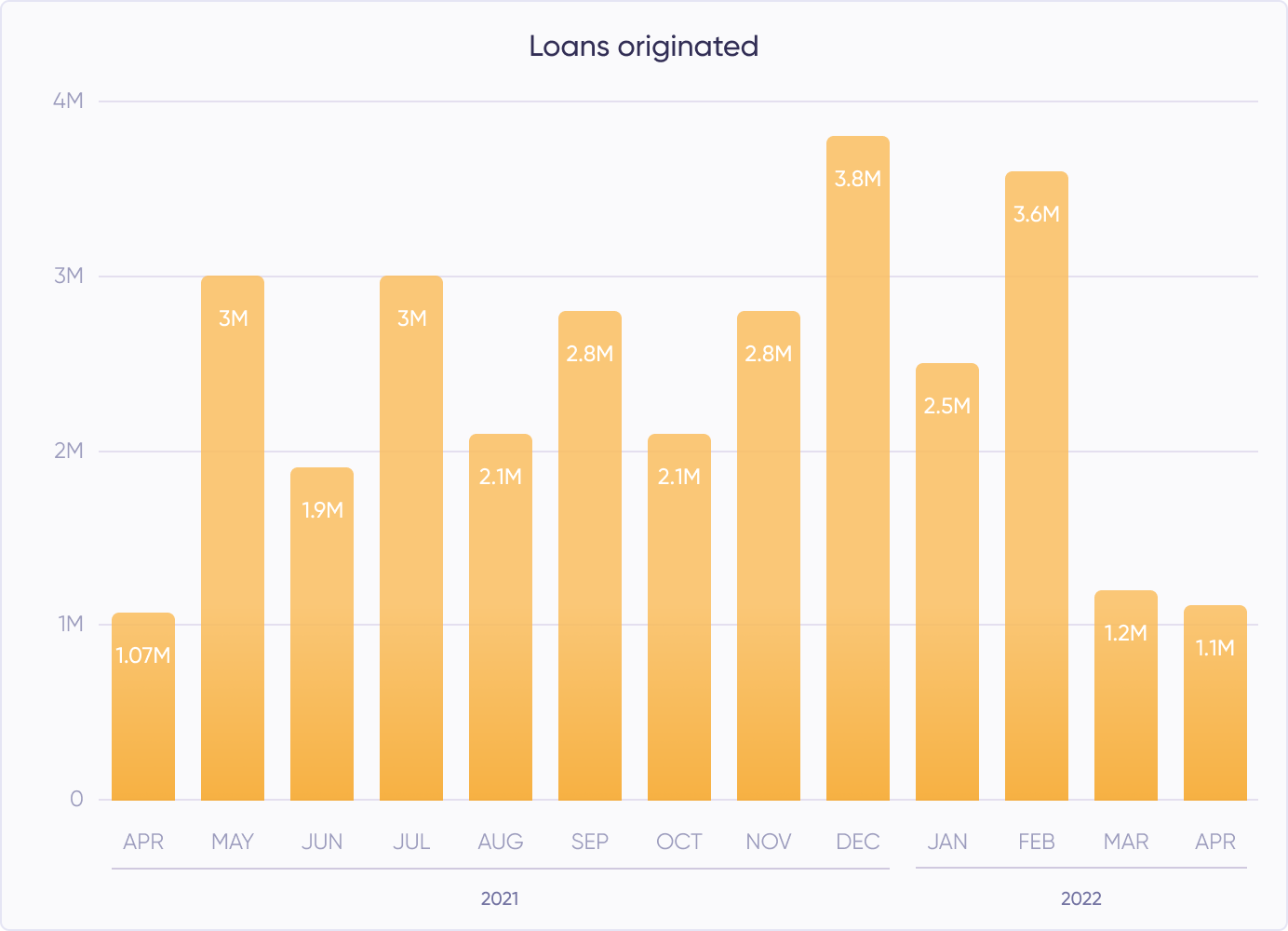

Loans originated

In April there are 1.1 mil. € of loan amount originated.

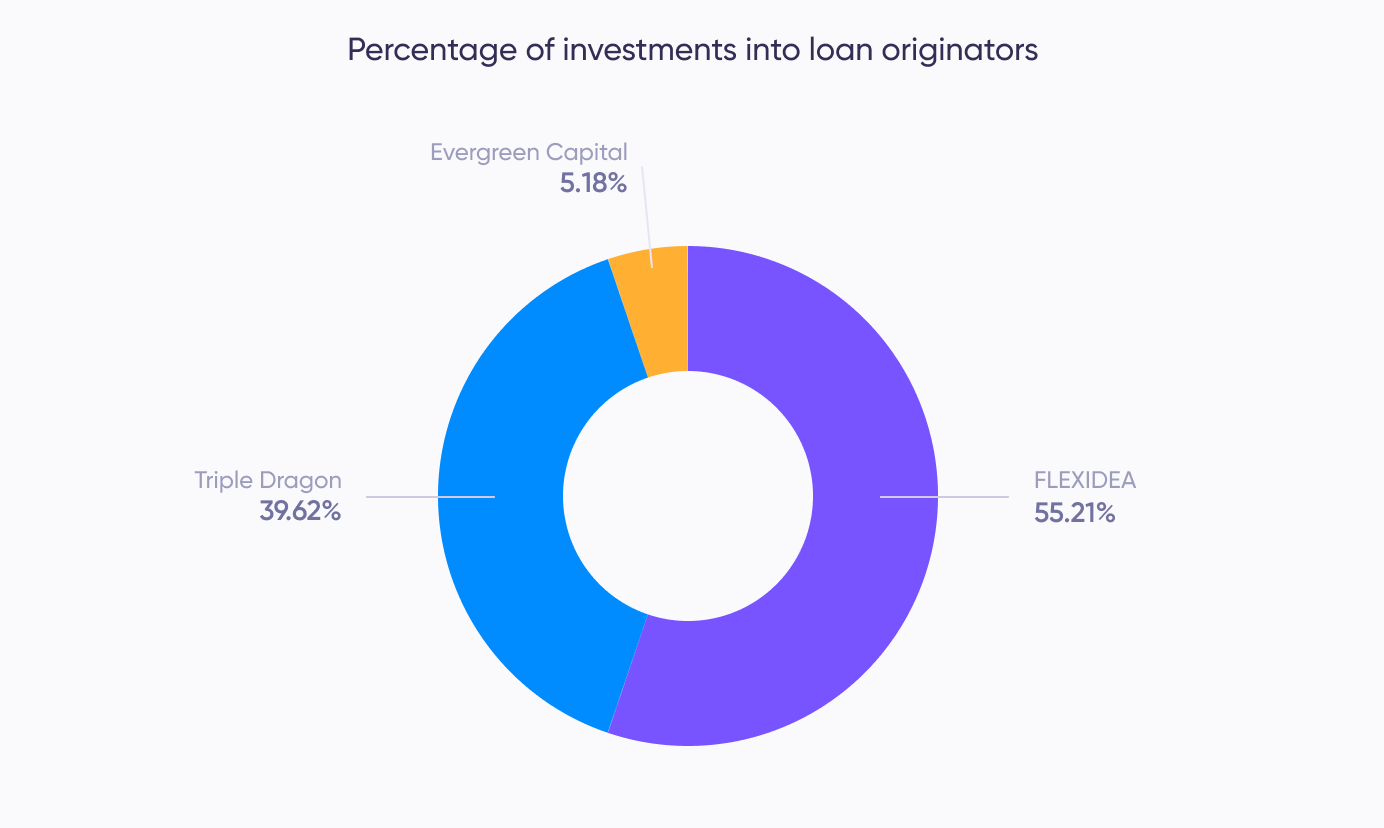

Percentage of investments into loan originators

In April of all investments – 39.62% are in TRIPLE DRAGON, 5.18% are in EVERGREEN CAPITAL, and 55.21% are in FLEXIDEA.

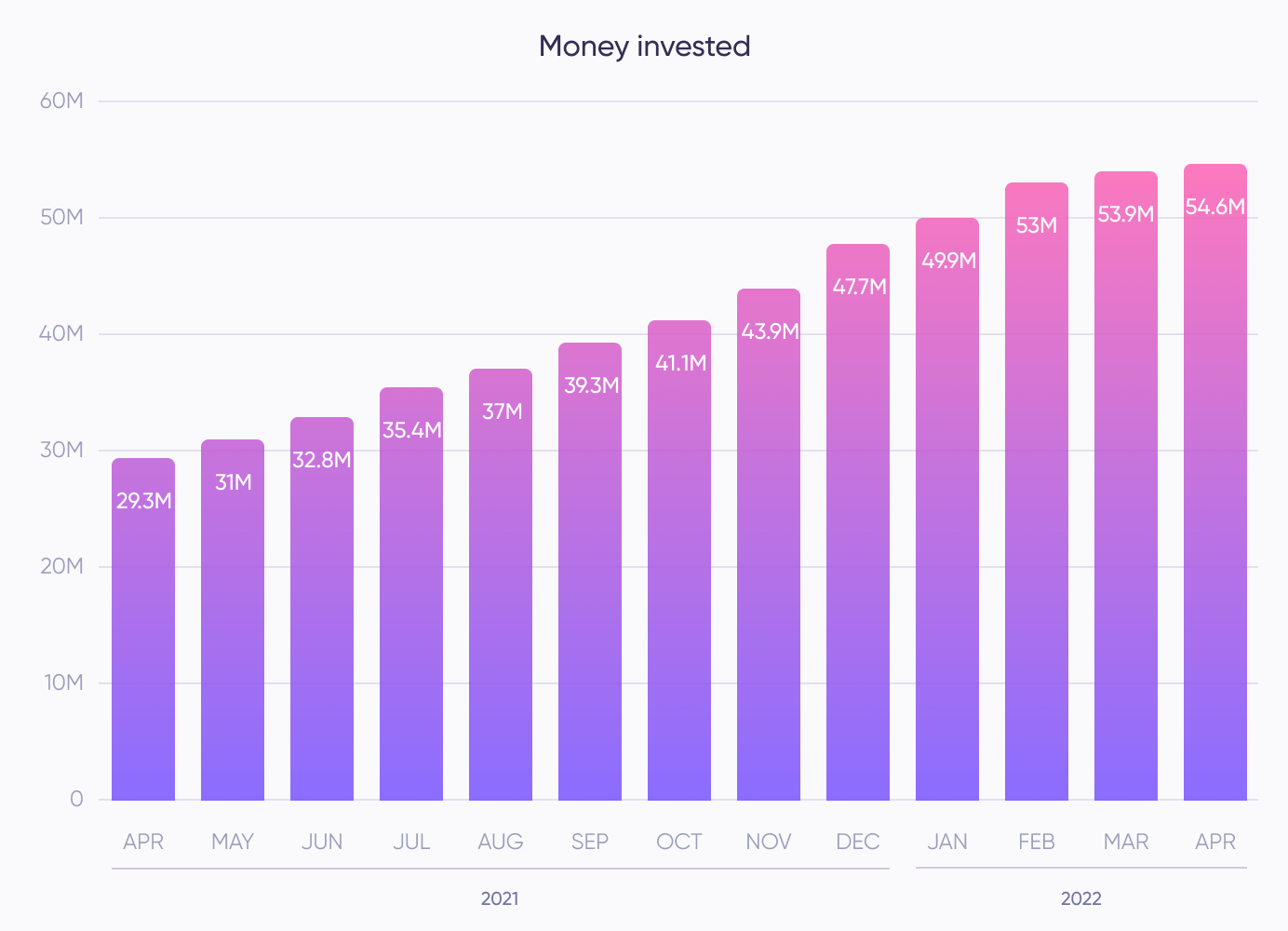

Money invested

In April, there is a total 54.6 mil. € invested.

Compared to March total money invested in April has grown by 0.7 mil. (1%). Compared to April 2021 total money invested in April 2022 has grown by 25.3 mil. (86%).

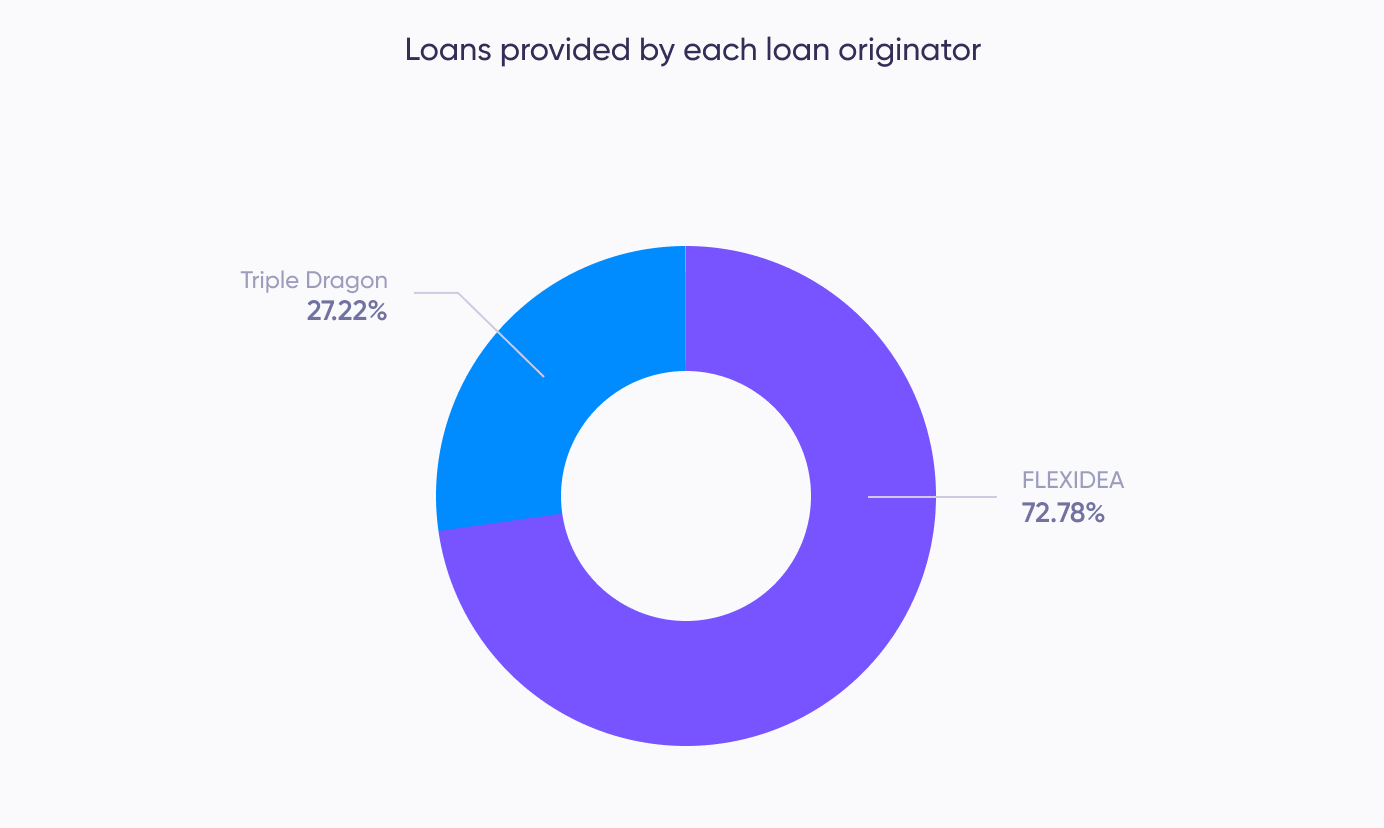

Loans provided by each loan originator

In April of new loans provided 27.22% is from TRIPLE DRAGON, 72.78% is from FLEXIDEA.

The most popular industry in April is ITT

If you are looking to invest then you should definitely note that the most popular industry in April was ITT.

Prosperitu joins Alternative Financial Services Association in Latvia

Prosperitu joins Alternative Financial Services Association in Latvia

We are happy to announce that Debitum Network platform operator ‘SIA Prosperitu’, established in the Republic of Latvia, has become a member of Latvian Non-bank association (Alternative Financial Services Association).

“To be a part of the association is another opportunity to upgrade our knowledge and offer new opportunities to our partners, investors and loan originators. Prosperitu is going to take part and give their impact working on P2P law project with other Non-bank association members” told us the director of Prosperitu Martins Perkons. For Debitum Network this also means being acknowledged as a notable player in the field of alternative finance and P2P online lending.

The mission of the association

Alternative Financial Services Association in Latvia unites providers of financial services operating outside the banking sector. Most of the members belong to financial technology or FinTech companies.

The mission of the association is the creation of a reliable and responsible sectoral practice, aimed at long-term cooperation and assessed positively by consumers and the market monitoring institutions, at the same time respecting the opportunities provided by the alternative financial services for free and ensured the development of every individual and society.

Members of the association

Members of the association come from the alternative finance industry and the following areas: leasing services, non-bank mortgages, online consumer credits, and peer-to-peer lending platforms. A lot of famous names in the P2P lending industry are members of the association such as: Mintos, Twino, or Robocash, and from now on Debitum Network is among the recognized players in P2P lending too.

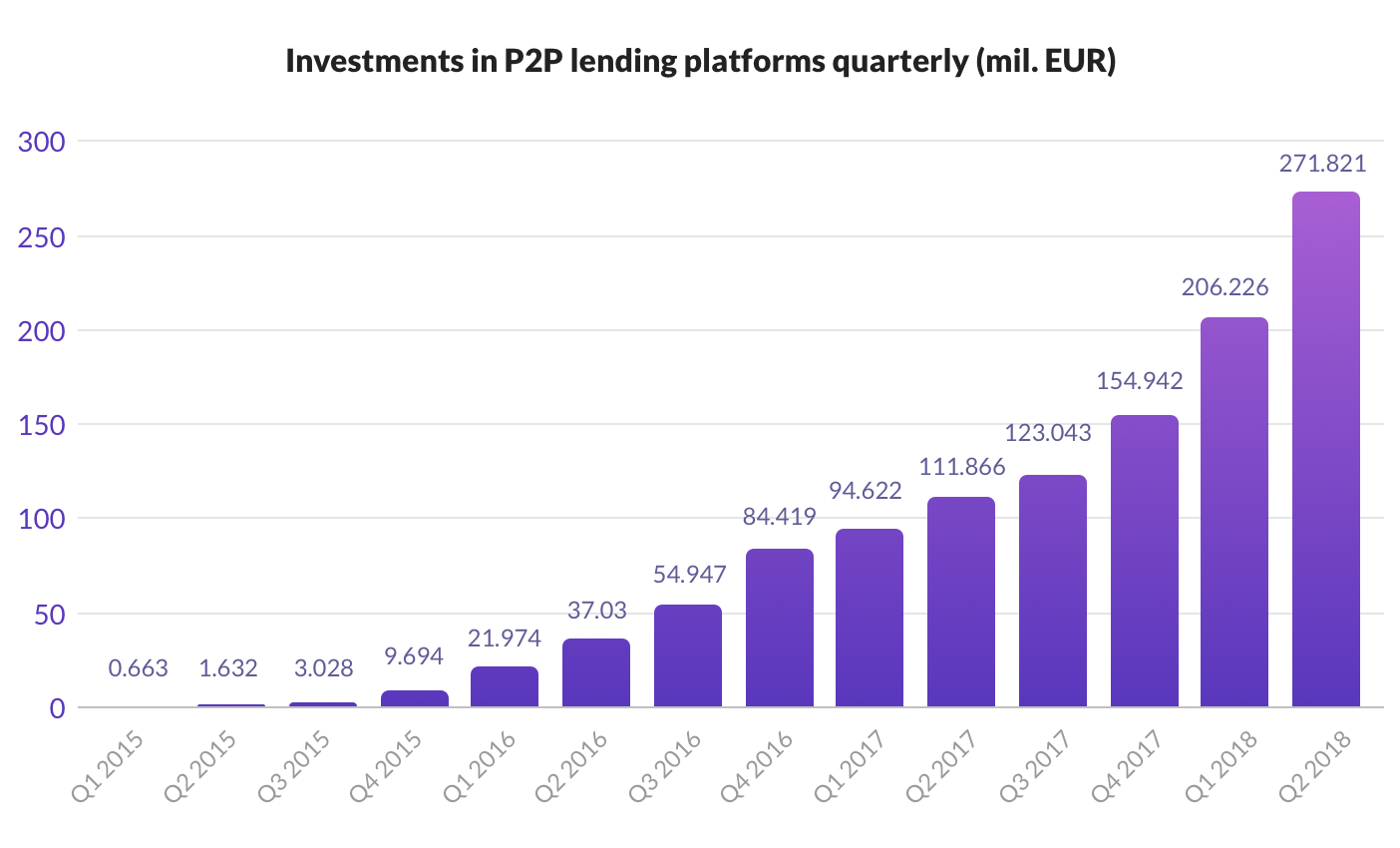

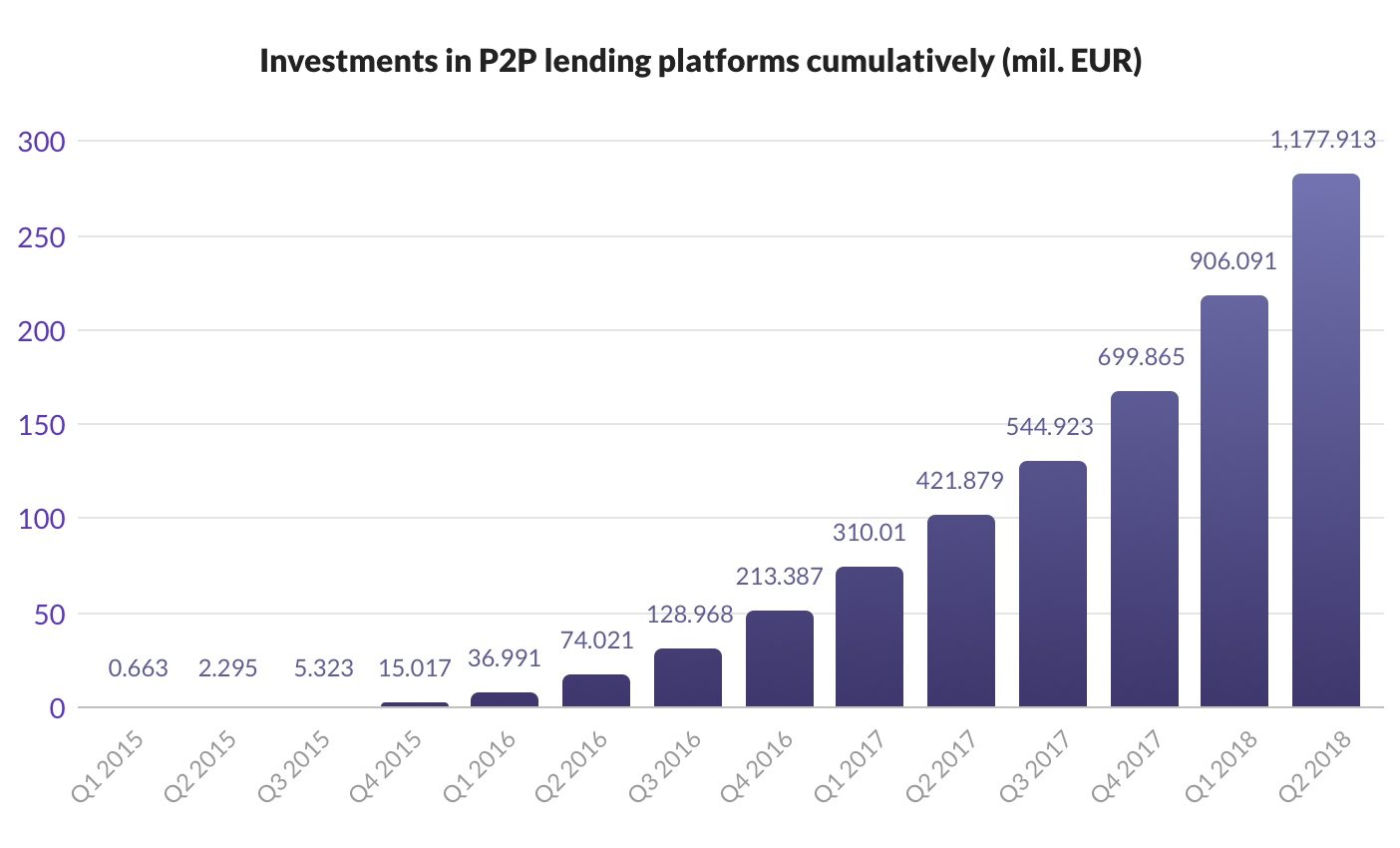

Online lending is a relatively new industry but statistics show that the interest and investments on P2P platforms have been growing by leaps and bounds in the recent years confirming we are in a competitive market with lots of opportunities ahead. Just take a look at the charts below.

Interest in Debitum Network platform on the rise

Interest in alternative investments will likely continue rising as interest rates in Europe remain close to zero. Debitum Network platform got real traction last year with multiple increases in the number of investors and investments month after month. This is likely to continue as interest rates for the assets vary from 7.5% to 11.5%, which is way above commercial banks or other traditional options of investments may offer. Just the fact should be a good incentive to join our platform and start investing.

Another incentive is that the assets are very low risk as all of them have guarantees: a buyback guarantee (it means that if the borrower is late with the repayment by more than 90 days, the loan originator will have to buy back the loan with outstanding principal and interest), collateral of physical assets (equipment, cars, warehouses and etc.) or a personal guarantee from the owners of the company that borrows. Having all of the above in mind, wouldn’t you like to try investing with us?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What makes any investment safer?

What makes any investment safer?

Investing is always associated with risk. There are no 100% safe investments. An investor always looks to balance the acceptable level of risk with potential reward. Some are willing to bet on EUR/GBP exchange rate fluctuations in the face of Brexit with 20x leverage on some retail Forex platform, while others are so risk-averse that they choose to lend to Germany, while Germany 2-year bonds are still providing negative returns of -0.6%.

The rule of thumb has not changed, though – the higher the risk, the higher the expected return. However, the returns, in case of lending would be hypothetical as riskier investments will have a higher probability of default, thus bringing the overall net return down. While Germany has its risk rating at AAA (default risk too small to understand – 0.00003% in one-year period or 0.00550% in 10-year period) or has its creditworthiness even as high as 100 out of 100 (the latest rating by Trading Economics), we expect that any amount lent to Germany will be returned as promised – no real risk for an investor.

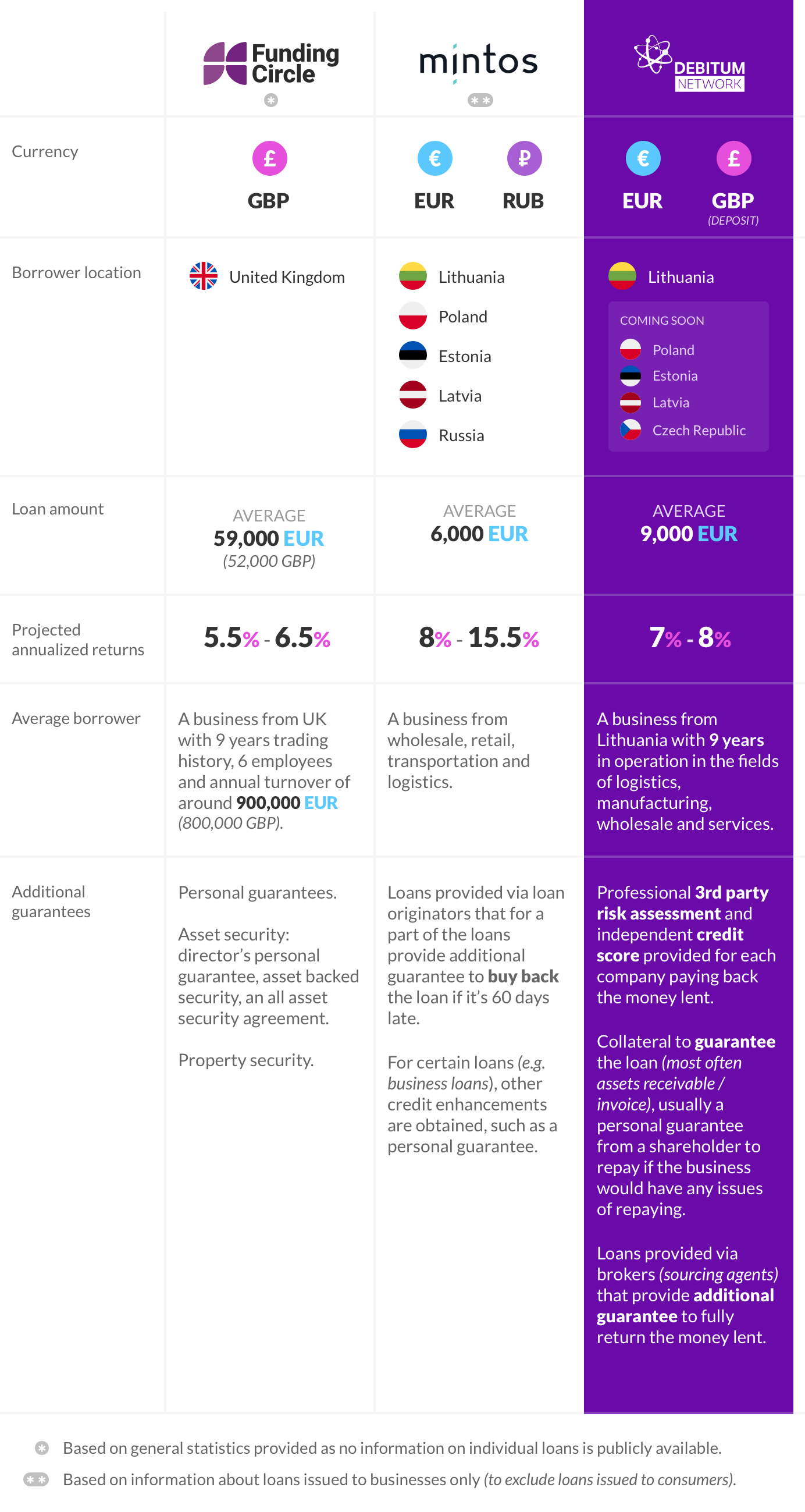

A more riskier option is investing on Peer-2-Peer or Peer-2-Business platforms with considerably higher returns. P2P or P2B solutions offer a possibility for an investor to directly lend to an individual or business that needs funding. Such solutions offer returns somewhere in the range from 5% on Funding Circle (Conservative lending option) and Debitum Network 7.3% to around 12% on Mintos (average historical return). Then, there are platforms like Bondora that offer an average interest rate of 32.5%, while the average net return is only 10.1% with 1 out of 5 investors losing money. The latter illustrates the point of a need for safer investments perfectly; as potential returns increase, so does the risk of losing one’s investment.

Safety is one of the key values at Debitum Network. When we started creating our platform, safety of investors’ funds was at the heart of it. Therefore, we chose to concentrate on loans to businesses, which have a much higher chance of repaying the loan rather lending to individuals. That allows Debitum Network to offer investment in business loans with average annual interest of 7-8%.

Let’s compare other details than interest rate for an average business loan currently available on the solutions mentioned earlier – Funding Circle, Mintos, and our own Debitum Network:

Businesses will hardly ever borrow at high interest rates that some of the Peer-2-Peer lending platforms offer. Nor will they offer extra guarantees and take risks ruining their businesses borrowing at 15-20% annually. Thus, platforms charging over 10% interest on loans will be much riskier for investors and likely attract more private individuals than businesses to borrow from. Debitum Network aims to satisfy business needs to borrow at affordable rates, as well as investors’ needs to have their invested capital safe. Which brings us to our initial position of lending exclusively to companies and at reasonable interest rates of 7-8%.

In addition to what has been said, here are a few principles, which we believe makes lending to businesses on our platform safer:

|

Professional risk assessors |

Third party services such as risk assessment single us out from other P2B platforms out there. Local professional service providers know local business specifics and therefore are better able to evaluate companies applying for a loan with much better precision than any generic risk scoring algorithm done by a single loan originator or platform itself. For Lithuanian market, Debitum Network uses Scorify, whose credit score rating system GoScore has been used to issue over 380’000 ratings. It ensures higher professional standard and more precise credit score available for a user to make a better informed investment decision.

|

Strong businesses |

Borrowers on our platform are well established SMEs and only loans handpicked by experienced loan originators such as Debifo and scored above the minimal needed credit score by independent risk assessors are placed on our platform. So far, the companies that borrow on Debitum Network platform have been in business for 9 years on average and they have borrowed and repaid the loans before. Longevity surely means better safety! Most current available assets are invoice financing loans with final payers of these invoices are mostly large companies with average revenue of 700 million EUR. They have been in business for decades and are considered key players in the economic areas of wholesale, manufacturing, logistics, and services. As the companies that actually ensure money inflow to pay back the loan are handpicked and truly strong in their respective sector and region, the risk for a loan not to be repaid and investor losing the money is reduced.

|

Guaranteed loans |

Each available loan on our platform is backed by an asset as a collateral – be it assets receivable (approved invoice for goods or services sold), variable asset (trucks, equipment and other) or fixed asset (real estate property). Often, there are also additional guarantees from company’s shareholders or another partner company’s guarantee. Moreover, our loan originators (brokers) have started offering a “buy back” of a loan being late more than 90 days. However, to make sure they can execute such an offer – we request them to put funds aside in a reserve fund as well as provide certain financial covenants towards Debitum Network.

Interested?

For many investors returns of 7-8% per annum sound really great and this is exactly what Debitum Network provides. Of course, there are ways to try earning more; however, one should always remember that in the world of investment, any type of return is associated with a certain level of risk.

As described, we, at Debitum Network work hard to ensure additional safeguards for your investment, so you can lend to businesses and earn returns with fewer worries. We believe that a loan with independent and professional 3rd party credit score and at least a few levels of payback safeguards (collateral from the business, it’s related entities and a broker that is sourcing the loan) is worth funding. Would you agree?

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Investment series: short term versus long term

Investment series: short term versus long term

One way to classify investing strategies is to take into account the time horizon. Long term versus short term is often discussed by financial experts, analysts and portfolio managers. One type of strategy by no means is better than the other. We may take the Oracle of Omaha Warren Buffet, who buys stocks and holds them indefinitely (and makes billions of $). On the other hand, there is speculator George Soros, who can keep his speculative position short term, just a few days and still make hundreds of millions of dollars as a result. Let us briefly cover the strategies and look at an alternative way to invest short term.

The difference of timing and expectations between the investments

A long-term investment will constitute investments, comprising stocks, bonds, real estate, and cash, that are intended to be held for more than a year. The long-term investments differ from the short-term investments in that the short-term investments will definitely be sold, sooner rather than later, whereas the long-term investments may never be sold.

Long term investments are those that have the likelihood to increase your profits over a long period of time. Those maybe index funds, stocks, long term government bonds. They tend to appreciate over the long haul and can withstand sharp and prolonged downtrends as an investor holding specific long-term instruments would not sell them when the financial markets are temporarily falling. Payout expectations are long term.

Short term investments will typically not last longer than a year and the investor holding financial instruments will look to convert them into cash any time opportunity presents itself. Payout expectations are short term. Among short term investors would often be traders or speculators that may hold their portfolio positions from a few hours to a couple of days. This is, naturally, increases risks as predicting daily or weekly fluctuations of any market is highly speculative and tremendously difficult thing to do. These types of investments may include: currencies, options, short term government bonds, stocks (for day trading) and etc.

Long term investors do not panic at short term market swings that go against them. Markets are cyclical. They go up and down, and then up again. On the other hand, those who have higher short-term expectations and take upon themselves higher risks should cut their losses quick when the market goes against them.

Investing in Short term business loans for small businesses

Short term investments may be not only securities, commodities, real estate or bonds but also loans for businesses. Alternative fintech companies such as our Debitum Network, Twino, Grupeer, Mintos, Funding Circle, Assetz Capital or Zopa not only help for SMEs to get funding for their operational costs but also gives both individual and institutional investors opportunity to participate in the financing process, invest in those loans and earn quite attractive annual interest at the same time.

Maturity terms for those loans typically last from a few weeks to 6 months. Annual interest is within the range 10-15%. Considering that a lot of investors cannot beat stock index returns, which is 8%, or even the average of mutual funds, which is 5%, 10-15% is really attractive.

Other advantages:

- Amounts are flexible. You can start with 10 Euros. The maximum is 10 million Euros.

- You may invest in an asset even if the repayment day is a few days away.

- Possibility to choose assets from various industries: Logistics, Wholesale, Manufacturing, Services to name a few.

- Portfolios should match the style of any investor: conservative, moderate and aggressive.

- All assets on the platform have a guarantee.

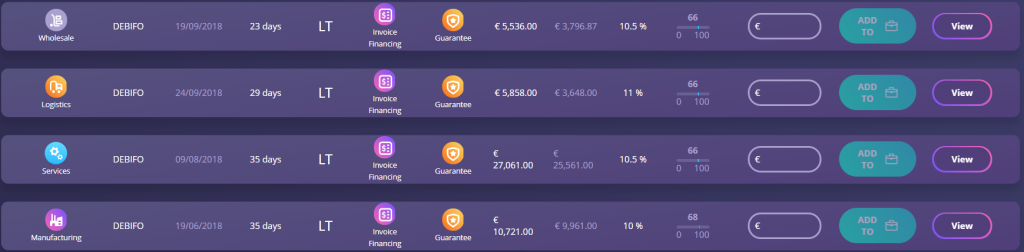

Below is the snapshot of 4 assets from our platform. You can invest in any of them. If you want to find out more what each item on the asset bar means and how to invest, you can read this blog post.

4 assets from the platform

If you got interested, try our platform

Disclaimer: It is important to point out that the approach presented here is not necessarily suitable for everyone and is presented for information purposes only. It is not intended to be investment advice. You should seek a duly licensed professional for investment advice matching your specific situation.

Investment series: Diversification

Investment series: Diversification

Diversification in investments is a method to reduce risk by distributing your funds among different financial instruments, industries, categories, and investment timeframes. Investors similarly use it to maximize returns on various investments that tend to perform differently at different market trends. It may not completely rule out risk, but surely reduce it significantly and enable you to achieve long term investment goals.

Why diversify?

If you own securities or commodities or any other financial instruments of the same kind, imagine what happens when the market turns around in that specific industry. More often than not, all of the securities in that field begin falling. Which means, all your investment portfolio is going down. Fund managers tend to mix up their portfolio with securities from different market segments: airlines, banks, high-tech, medicine, services, some commodities and etc.

A single event that may impact negatively one specific sector, will highly unlikely impact all of the sectors of the global economy. It is prudent to comprise your portfolio of instruments that do not correlate much so that when one segment of the market is affected, it would not impact the bulk part of your portfolio. Diversifying among asset classes is another way to make your investment strategy as efficient as possible. Government bonds will surely perform differently than stocks and what affects one group may not affect the other. Bonds and equities tend to move in different directions, so if your basket of equities is falling, your basket of bonds will likely rise.

A new area for your diversification – short term loans for SMEs

When it comes to investing, the first thing that would come to people minds are stocks, bonds, commodities. Some would add currencies, maybe real estate or physical methods. Few would think about investing money in loans for small businesses.

A new era of fintech and the blockchain opened new markets for investment. Regulation requirements and interest of commercial banks in big businesses left small businesses largely underfinanced. This created a new market for alternative lending. Businesses and individuals around the world can now finance SMEs globally. This has become a new stream of investments for any prospective and savvy investor to consider and an alternative way to diversify your investment portfolio. P2P lending platforms similar to Debitum Network are on the rise. Among them: Funding Circle, Mintos, Twino, Assetz Capital, Follow Finance, Ratesetter, Zopa, Upstart, Prosper Marketplace or Lending Club.

Debitum Network platform 1.0 Abra is live

On the 3rd of September an innovative alternative finance platform Debitum Network 1.0 Abra launched. It connects small businesses and funding sources around the globe. Now, anyone can participate in supporting the growth and expansion of SMEs and earn attractive interest at the same time.

Disclaimer: It is important to point out that the approach presented here is not necessarily suitable for everyone and is presented for information purposes only. It is not intended to be investment advice. You should seek a duly licensed professional for investment advice matching your specific situation.

Martins Liberts’ interview at VZ office

Martins Liberts’ interview at VZ office

VZ (Verslo Zinios), one of the leading business/finance newspapers in Lithuania invited co-founder of Debitum Network Martins Liberts for an interview. Martins sat down to share his vision of Debitum Network, behind the scenes of preparation for the upcoming release of the platform on the 3rd of September, and future plans. Below are some of the themes that were covered during the interview.

“Banks are not necessary for borrowing”

The title of the article “The banks are not necessary for borrowing” put a smile on our faces. IFC (International Finance Organization) has recently released a report, which indicates that there is 5.2 trillion $ gap in credit for micro, small and mid-sized businesses in the world. Traditional banks are not that interested in financing these. Debitum Network aims at filling some part of the gap by connecting small businesses in need of capital with investors. As a result, a new market is being created, where Debitum Network will connect borrowers to investors who invest in fiat. Thus, banks will also be able to participate in the financing process.

Debitum Network is a B2B platform

Martins singled out that in Lithuania and around the world there are a lot of internet lending platforms that are P2P (peer to peer), while Debitum Network is B2B (business to business). The main focus is to connect businesses that want to borrow with businesses that want to invest.

Individual investors will also have a chance to onboard the platform and invest flexible amounts, but the recipients of loans will only be businesses, not individuals. At the beginning of September, Debitum Network is organizing a fundraising event in London, where more than 100 institutional investors are expected to participate.

Investment amounts and potential interest

Most P2P platforms lend at 20% or more annual interest rates and few if any businesses will borrow under such conditions. When Debitum Network platform launches, SMEs will be able to borrow up to 10 million EUR, at an average 10-15% interest rates annually with terms between 2 weeks to 2 years. Banks typically lend at 3-8%, so you may see that we fit in the golden middle.

Responsible assessment of SME and distribution of loans

Martins, likewise, stressed that loans will be distributed responsibly and each SME that applies for a loan will have to provide legal documents, prove its’ solvency and pledge some assets as a guarantee.

Blockchain technology will be key to test the reliability of a borrower, as all operations and will be recorded on the blockchain and will be available to everybody.

Trust rating algorithm, together with a risk assessment score give star ratings for each participant on the platform. Trust rating algorithm was created by KTU (Kaunas Technological University). Third parties will also offer services of risk assessment, insurance, and debt collection.

Expectations for the launch

Martins states, that it is expected to start with € 500 000 – 1 000 000 worth of loans, on the day of the launch and have a turnover of 10 million EUR by the end of the year. Debitum Network has already made agreements with enterprises from Lithuania and Latvia and will soon be joined by companies from Estonia. The Czech Republic and other European countries will follow suit.

Modification to the previous expansion plan

Liberts admitted, that initial plan to launch in 16 countries and later expand to 50 countries were too ambitious, and the plan was moderated to expand at a slower pace, but in a more decisive manner and convincingly, by starting in 5 markets.

In the beginning, the funds between investors and SMEs will run through Debitum Network, and as the system reach maturity, Debitum Network will perform the function of a “bulletin board” by simply connecting investors with businesses who need to borrow.

The co-founders and experience beyond Debitum Network

Besides Martins Liberts, the other two co-founders of Debitum Network are Donatas Juodelis and Justas Saltinis, both of them are also co-founders of invoice financing company “Debifo”. Donatas is also one of the co-founders of INNTEC – a progressive IT company.

Thus, Debitum Network is being built on the practice and experience gained in the sectors of finance and technology. The company currently has around 30 people working on the project.

Interview with Nikita our country manager for the Czech Republic

Interview with Nikita our country manager for the Czech Republic

Our team at Debitum Network is expanding rapidly and with the approach of the platform in September, we expect to grow even more. Today, we want to introduce you to our new country manager for the Czech Republic Nikita Inzhevatov. Nikita spent two weeks in our Vilnius office familiarizing himself with our business, communicating with us and planning for his role as a country manager. We sat to talk about his previous work experience, why he made up his mind to join our project and what his two weeks with us were like.

Can you tell us briefly about your work experience?

My career began by selling corporate events, where I gained a lot of experience. Then I worked in customer support for Xerox, the company that provides services for a huge American company in IT. Later I did Software Asset Management for Microsoft and Inside Sales for HP inc.

Why did you decide to join Debitum Network?

Most of the companies, that I worked for, were on an early project phase. This is a very interesting stage to start. The same with Debitum Network. Here I will use all my experience already gained and will really try to make a difference and help the project develop even faster.

What do you like about our project?

Debitum Network is a very interesting and prosperous project, which will help finance the SME market and eventually help grow the economy. There are many companies nowadays, that need financing but are unable to go to banks. This is where we come in.

What will you have to do as a country manager for the Czech Republic?

My job is to attract as many high quality and trusted third-party local partners as possible by negotiating and discussing fair tariffs and services. I will also be searching for loan providers, which will fill our platform, businesses, that need money, that our investors will finance. I understand, that it will be tough, but I am ready and accept the challenge.

What has been your experience during these two weeks in our Vilnius office?

The atmosphere couldn’t be more friendly and the coffee couldn’t be tastier! The colleagues are very experienced and each and everyone tried to share their knowledge and help in every possible way. Everyone knows his/her job and does it to the max. I want to thank the guys a lot, for the support and training, that were provided, during my stay!

Thank you for the interview. Have a safe journey back and good luck.

Thank you, it was my pleasure!

Ways to get funding in alternative finance

Ways to get funding in alternative finance

Traditional way of getting a loan, that involves going to a bank and filling an application is probably the only way most people imagine. However, there are a lot of other ways to get funds for your small or medium-term business. Alternative finance p2p platforms such as our own Debitum Network or Mintos, Zopa, Funding Circle, Assetz Capital and others can offer you a few possibilities to choose from. This blog post aims at describing some of the most popular ways that alternative lenders provide funds to small businesses.

Equity crowdfunding

Equity crowdfunding is the process when, typically, a lot of people (crowd) provide money to small business in return for equity. Small businesses do it with the help of a crowdlending platform. This type of funding has been around for many years. However, in the past it would take big businesses or angel investors to provide the bulk amount of funds. In traditional IPOs, the starting sum would be $ 1 million. Nowadays, a lot of people with as little as $ 100 can participate in the funding process.

P2P lending

Peer to peer lending is online lending service that connects individual investors with borrowers and a loan is provided with an agreed fixed interest rate and maturity. Borrowers have their profiles on P2P lending platforms and investors may look at them, analyze past performance and determine whether they want to take risks lending money to that specific borrower. Borrowers can be both individuals and small businesses. An individual may provide a partial or full amount requested by a borrower. The rest money will come from other individual investors. To some extent, Debitum Network can be regarded as P2P lending platform, despite the fact that it only lends money to small and medium sized businesses, not individuals. In this regard, it is B2B (business to business) platform.

Property finance

Property finance type of funding is usually a secured business loan, where property (residential, business or property portfolio) is used as a collateral. You use the option when you want to borrow to buy property for a business or redevelop your existing property. You may also need to have a big deposit (up to 40 percent) for getting this type of loan. The benefit of that is that the bigger the deposit, the smaller the interest rates.

Invoice financing

In invoice financing a borrower uses his customers’ outstanding invoices to borrow money. A lender buys those invoices. In this way, an invoice of sales becomes a security for a loan. It has an advantage that you do not risk losing equity of your company. Small business companies often use this method of funding to get cash without waiting for the payment dates from their customers. The payment terms can be a drag as businesses often need cash fast for operational expense. Invoice financing allows you to transfer payment terms to your lender and you get the necessary money immediately. Invoice financing average return averages around 10-15% per year.

Asset based investing

Asset based lending is any kind of lending secured by an asset. When an asset is used as collateral, in case a borrower fails to repay the loan, the lender takes the asset from the borrower. This type of lending is typically used when a lender is not convinced that a company can pay the loan through its cash flows. Typically, the assets that are taken as collateral are: inventory, accounts receivable, machinery and equipment.

Register and start investing on Debitum Network platform

As you may see, there are plenty of ways to get funds for SMEs outside of traditional banking system. When Debitum Network platform launches in September, 2018 small businesses will have lots ways to get funding. There will be assets such as Factoring, Business loan, and a few more to choose from. Average expected returns for investors would be 7-11% per year and short term loans will vary from 2 weeks to 6 months. As platform is going to be global, any investor from around the World can invest in any asset with a flexible amount of capital, not necessarily full requested sum.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.