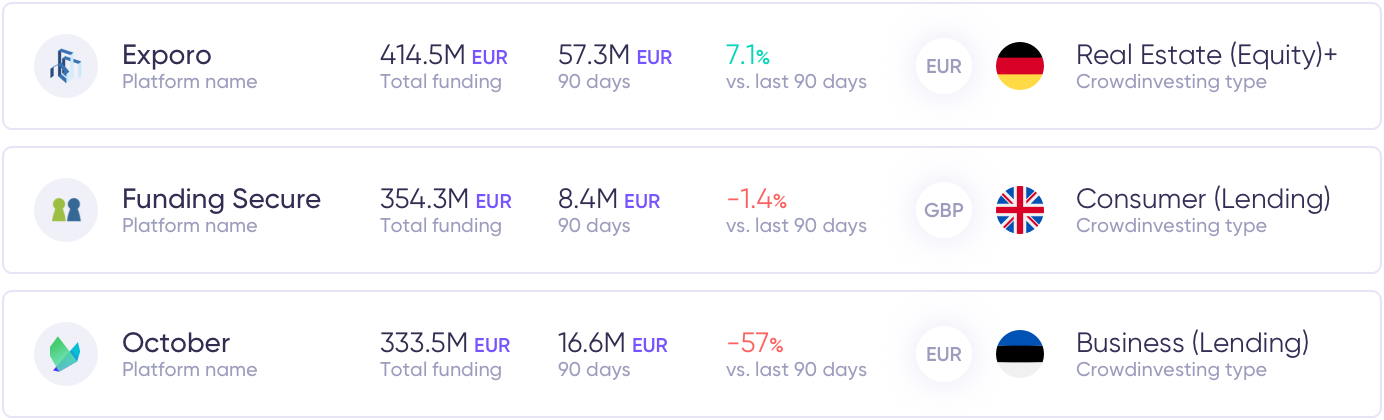

Tag: Funding Secure

Current trends in P2P/P2B lending and where does Debitum Network stand

Current trends in P2P/P2B lending and where does Debitum Network stand:

P2P/P2B lending market has been growing by leaps and bounds since 2005 when the first lending and investing platform of its kind (Zopa) was launched. The growth started accelerating after the financial crisis of 2008 when Central Banks slashed interest rates close to zero (or even below it). Attractive interest rates offered by alternative investment/lending platforms attracted a lot of retail and institutional investors and the market has grown from 1.2 billion dollars in 2012 to 64 billion dollars in 2015. It is expected to reach 500 billion dollars by 2025 by some moderate estimates or even 1 trillion dollars. What are other trends in the market and where Debitum Network stands in relation to other similar platforms? Stay with us and find out.

More platforms are expected to join an alternative lending/investment market

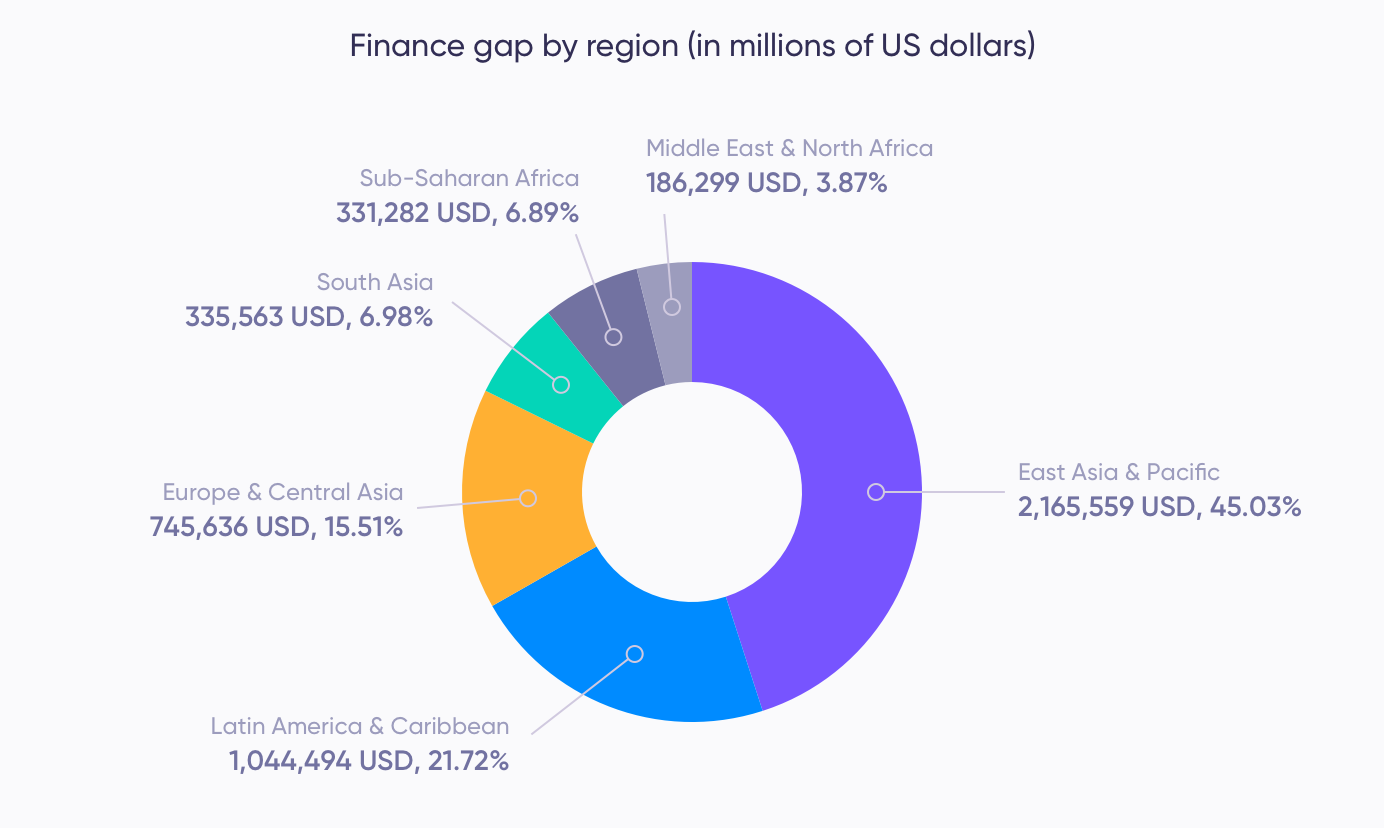

According to Reuters, P2P lending is among the fastest-growing segments in the financial lending market. Alternative investments are popular with the current generation and this means more market players will join the market. The market will continue growing as distrust in commercial banks remains huge. The interest rates offered by mainstream lenders are very low, and they still do a poor job in financing small and medium-sized businesses as well as consumers. The potential for Debitum Network (a P2B investment platform) is still great as SMEs in Europe are still underfinanced and the interest in alternative investments is on the rise. Check out the credit gap for SMEs around the world.

Source: smefinanceforum.org

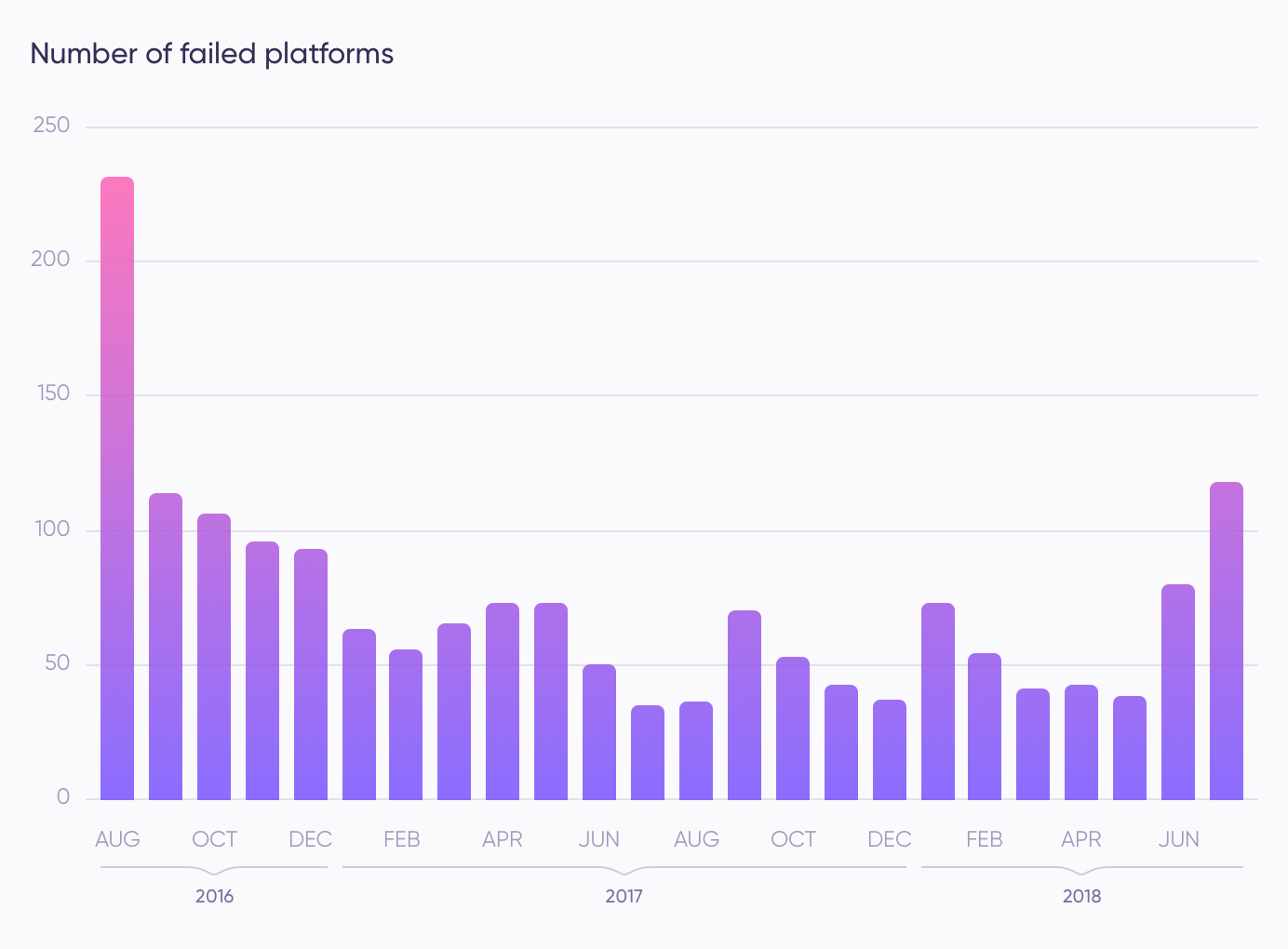

More bankruptcies of careless P2P lending platforms

Alternative lending platforms have to be careful who they lend money to or what loans they upload on their platforms for investment. Within the last year, 3 prominent alternative lending/investment platforms in the UK: Collateral, Lendy, and most recently Funding Secure went bankrupt. Tens of thousands of investors lost a lot of money, despite the fact, that Lendy and Funding Secure were regulated by the UK regulators. The UK is not an exception. A year ago, China underwent a turbulent period when thousands of P2P lending platforms went broke causing millions of investors to lose their money. The industry in China is close to $ 200 billion. Regulators have seriously cracked on online P2P lending platforms and only a few regulated ones will remain alive in the long run. The chart below says it all.

Source: bloomberg.com

Debitum Network takes seriously the safety of investors’ funds and therefore we have implemented a number of safety measures to ensure that. Firstly, we have a thorough screening process of potential loan originators to make sure they offer good loans with an excellent base of borrowing companies. Our risk management team follows up with a thorough investigation of the financial situation of a lender who is already onboard of Debitum Network and does responsible quarterly due diligence process. A case with Aforti Finance was an example of how the team’s work helped to avoid potential risks to investor’s funds and thus the assets of the mentioned loan originator were removed from our platform.

We have also implemented a buyback guarantee, which means that if the borrower is late with the repayment by more than 90 days, the broker who issued the loan will have to buy it back with the outstanding principal and interest. Most of the loans on our platform are with the buyback guarantee! Last but not least, we have independent risk assessors that do a risk assessment for the borrowing companies whose assets are uploaded on our platform. This type of risk assessment increases transparency, provides a more accurate risk scoring, and protects investors’ funds.

Acceptance by the mainstream

Governments around the world start welcoming fintech companies, including P2P/P2B lending/investment platforms. They seek alternatives to current established lenders (commercial banks) to increase options for small and medium-sized businesses to get funding. Thus, investing on these kinds of platforms becomes a part of recognized financial products just like the ones offered by traditional lending institutions. P2P lending has been authorized in all of Brazil since last year. Malaysia has a P2P scheme for first-time buyers. And in the US, P2P lending is regulated by the SEC (Securities and Exchange Commission). Thus, the importance of P2P/P2B lending is recognized by governments around the world.

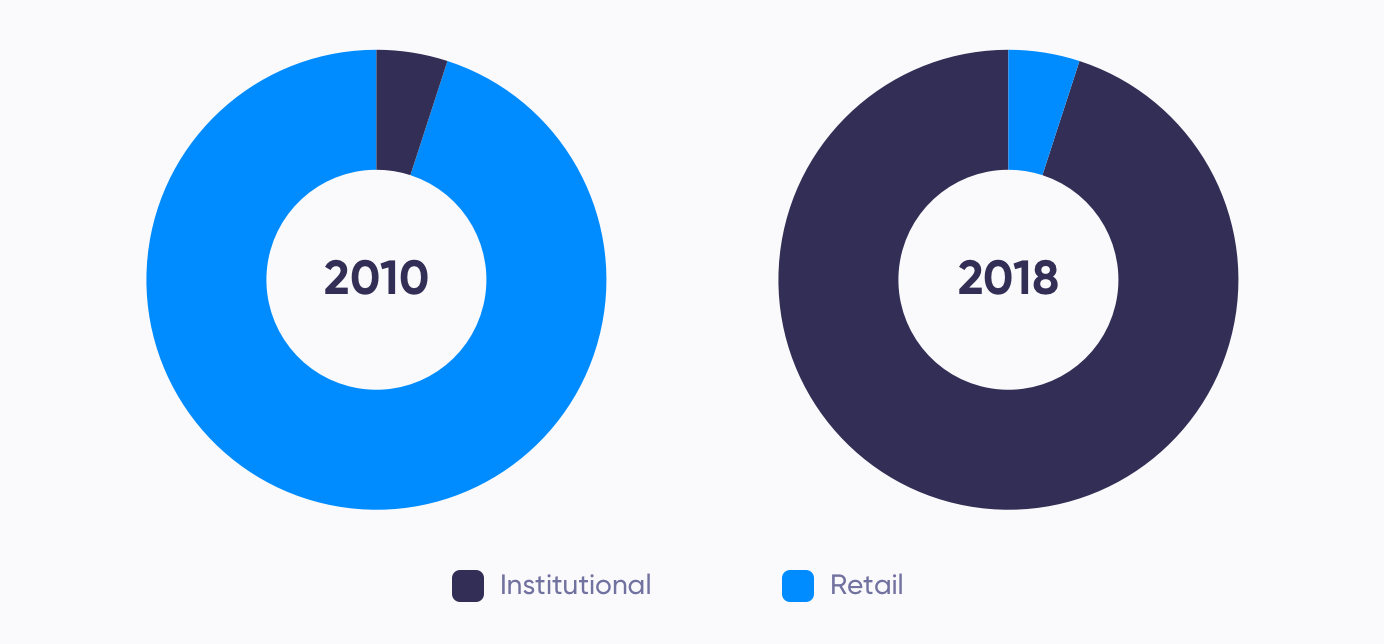

Increase in institutional investing

For quite a while, most investors on the alternative investment platforms were retail investors who would typically invest from 50 EUR to 5,000 EUR. The trend has been slowly changing across the board. Some platforms experienced it tremendously. Lending Club, the leader in consumer loans in the US shared in their blog post the following stats. The investments from institutional investors in 2010 covered less than 5% of all investments on their platform (10 institutional investors). In 2018 institutional investors comprised 95% of all investments (200 institutional investors).

Source: Lending Club

Debitum Network has been open to both retail and institutional investors since its inception. We have seen more and more institutional investors onboard our platform and expect the trend to accelerate as more loan originators onboard our platform and investors are offered a more diverse range of assets for investment.

More regulation for P2P platforms in the near future

The unregulated environment allows for more irresponsible lenders to exist and act carelessly with investors’ funds. This means that governments will not only encourage P2P lending/investing but will step up and increase regulation over the process. This will likely weed out those that compete unfairly and strengthen those that play by the rules and responsibly. Wild West for risky investment platforms that offer high returns and no security for investors’ funds might be over sooner rather than later.

Debitum Network is currently in the process of getting a license with one of the European financial regulators. We expect it to happen before the end of the year or the beginning of next year. We want to transparent, responsible and a safe environment for investors’ funds.

With that in mind, let’s proceed to our special offer for the week.

Top asset of the week

This week want to offer you an excellent asset that comes from our partner and loan originator Factris. The borrowing company is a wholesaler of hardware equipment. It has more than 25 employees, revenues of more than 4.1 million EUR, and has been in business for more than 21 years. The purchaser of the invoice is a distributor of metallurgical products, operates in Europe and has more than 270 million EUR revenues. Does it sound good enough? Check out the asset.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Debitum Network – a leader in interest rates for Invoice Financing loans

Debitum Network – a leader in interest rates for Invoice Financing loans:

High yield assets are definitely one of the top reasons that attract investors. The second one would be assets that are secure. After the 2008 crisis, most Central Banks slashed interest rates to zero or even below it. Keeping money in savings accounts became an unprofitable way to handle your money, despite a safe one. Alternative finance/investment platforms both P2P and P2B started growing like mushrooms after rain. They started offering above-average returns, in most cases higher than one can expect to get investing in most popular options such as stocks, hedge/mutual funds, or indexes. Debitum Network is not an exception as it offers some of the highest interest rates among investment platforms for loans in Invoice Financing category.

Overview of alternative investment platforms

P2PMarketData gives us an overview of the major players in alternative investments (P2P/P2B. There are currently around 80 well-established investment platforms around the world. Most of them specialize and accept/originate specific types of loans as assets for investment. They basically fall within three major categories:

- Consumer loans (33 platforms)

- Real estate loans (22 platforms)

- Business loans (28 platforms)

We can see that the distribution of these three types of loans among platforms are almost equal. Statistics regarding returns vary and it would be difficult to say the exact percentage for each platform as; not all are secured loans or have buyback guarantees, interest rates on assets vary and they change.

Let’s say you choose Lending Club, which is a top P2P lending platform in the world. They provide unsecured consumer loans for investment with various returns based on the risk category. What it actually means is that you can make 15% or you can lose all your money if you invest in loans that default and become uncollectible (this week one of the leaders in UK P2P platforms Funding Secure went bankrupt).

A leader in business loans Funding Circle (in the UK) also offers investment in unsecured business loans (development loans secured by property and land). The expected returns with the platform would be up to 7%. Taking into account, that most loans are unsecured, the returns are really low.

A lot of other investment platforms both in consumer and real estate will offer returns of around 8%-13% annually. But there is one but!

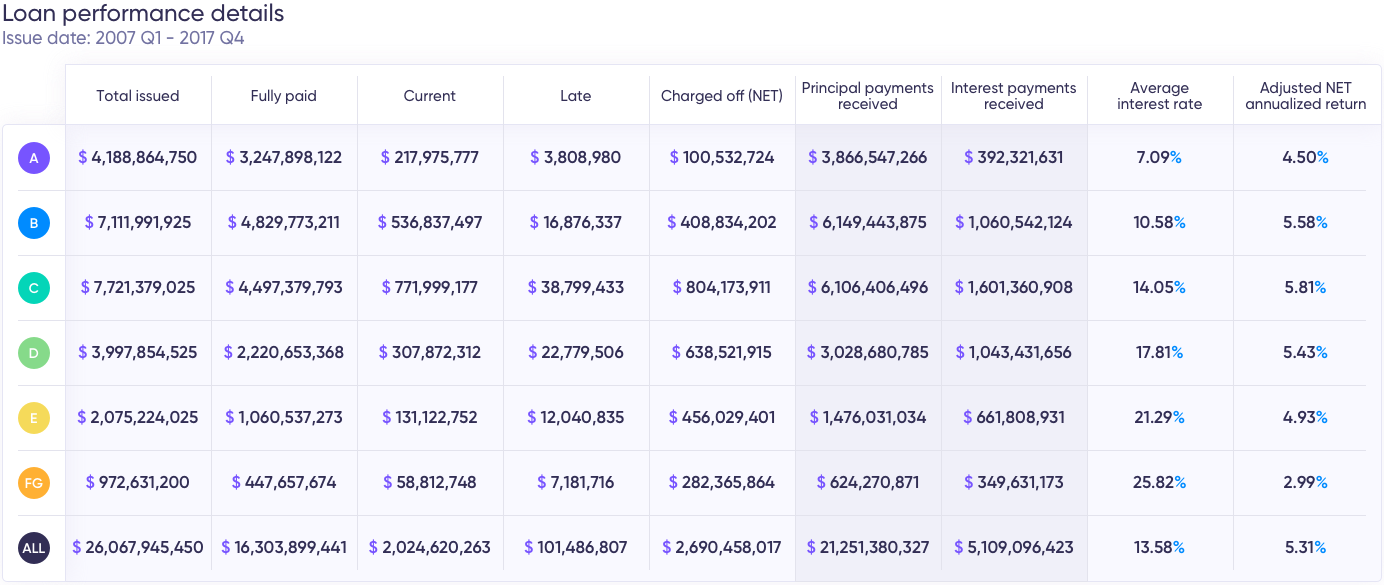

Expected Returns differ from real ones

It is obvious that returns depend on risk levels. If the platforms do not have an implemented buyback guarantee, the expected returns can be radically different from the real ones. Lending Club has shared some stats on their website and you can see for yourself how greatly adjusted annualized returns differ from the projected interest rates under specific risk categories. Defaulted loans can drag your real returns down up to 3-6 times.

Source: https://www.lendingclub.com/info/demand-and-credit-profile.action

For the sake of being discreet, we are not going to name specific names, but there are platforms that have default rates of 30%. It means that investing in these types of loans you are basically buying a lottery ticket. You may get lucky and earn around 20% annually, or lose all of your money. You have to do a thorough and time-consuming analysis before you can make the right picks for investment.

Debitum Network returns and conditions

Currently, Lifetime Invested Interest Rate on Debitum Network platform is 9.20%. Most of our investors get even better returns. How is that? Well, you can exclusively invest in 9.50%-10% assets and your returns will be higher than the average. Additionally, most of the loans on the platform have a buyback guarantee. In case, a borrower defaults on his obligations, the broker who issued the loan will have to buy it back with the outstanding principal and interest. Thus, the returns are real. Very few platforms will offer that returns with a buyback guarantee. Due to the guarantee, there has not been a single default on Debitum Network.

Furthermore, not only most of the assets have a buyback guarantee, but each asset will have a specific penalty rate, which an investor is going to earn, in case the borrower is late with repayments by more than 15 days (15 days is a grace period when no penalty is charged to a borrower). Penalty rates vary from 2% to 4.5%. It means you are able to earn beyond the platform average of 9.20%. Very few platforms will offer a penalty rate for late loans.

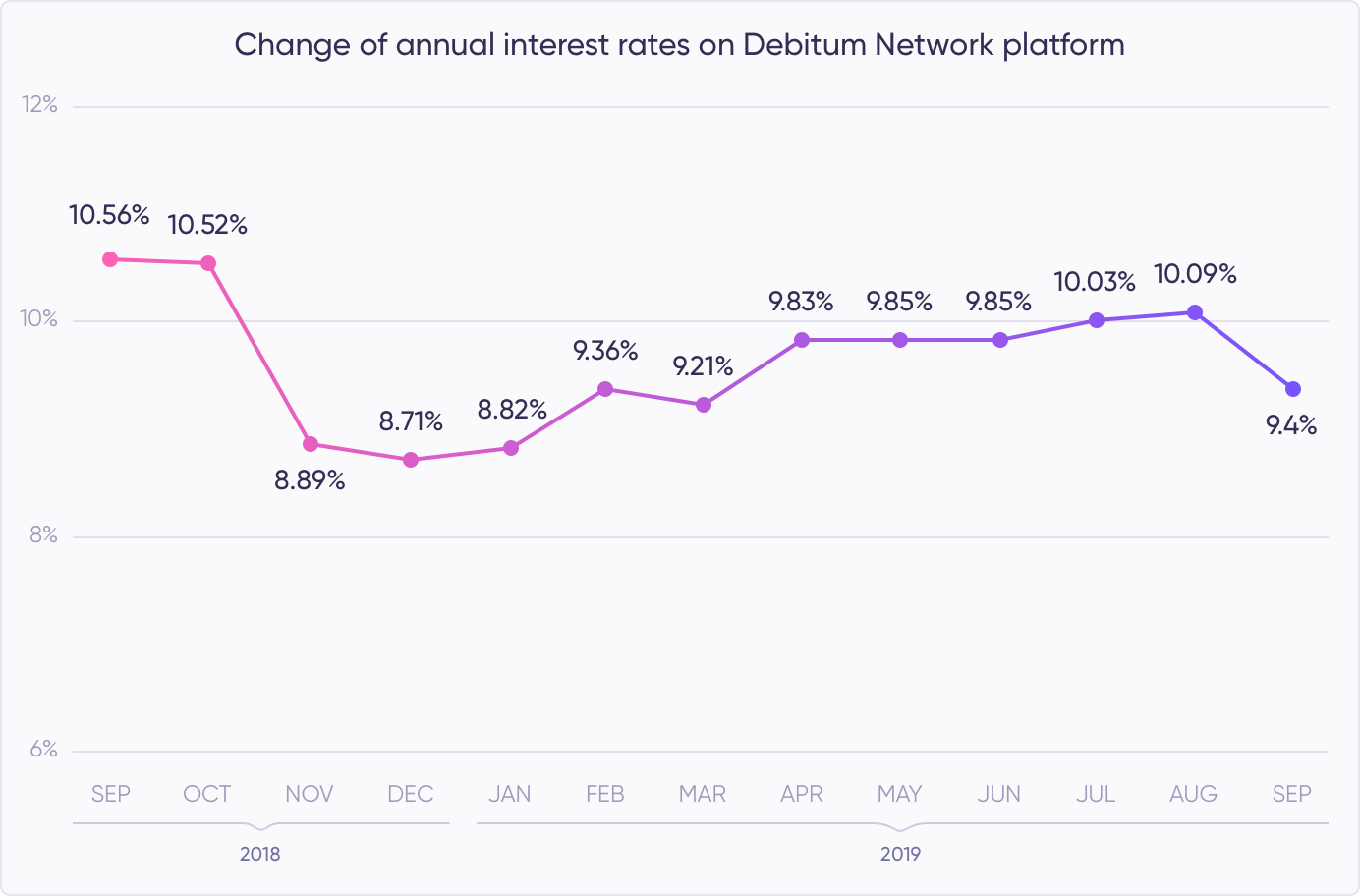

Thus, taking into account a current Lifetime Invested Interest Rate, a buyback guarantee, and a penalty rate, we can state that Debitum Network has the highest interest rates in Invoice Financing category. Take a look at how interest rates (earned) fluctuated since the launch last September, till the beginning of October this year. Have in mind, that these are the rates investors really received, (not adjusted) and there were no factors that could reduce them (no defaults due to the protection by a buyback guarantee).

Top asset of the week

The asset is from our partner and loan originator Factris. The borrowing company is a producer of electricity which has more than 340 thousand EUR in revenue, more than 60 employees and has been in business for more than 7 years. The Purchaser of the invoice is a manufacturer of petroleum products. It has more than 4 billion EUR in revenues, employs more than 1000 people, and has been in business for more than 28 years. Like what you see? Be sure to add it to your portfolio.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.