Tag: hedge funds

Hedge Funds: From a Slap on the Back to a Slap in the Face

Let’s have a quick look at hedge funds – the deregulated, risky investments reserved for the rich. Hedging basically means “off-setting risk by putting money into certain stocks or investments and shorting others”. Whether the market goes up or down is inconsequential – a hedge fund can make (or lose) money either way. But when the returns are good, they can be shamelessly good.

In 1949, when Fortune journalist Alfred Winslow Jones invented the term hedge fund, they were only accessible to the wealthiest investors, leaving out average income earners. Until fairly recently, 1 million dollars was still the entry fee into a hedge fund. However, the birth of “lite” hedge funds has brought that minimum investment fee down to 100,000. That’s still not exactly pocket change.

A lack of rules and regulations meant that for a long time hedge funds were Wall Street’s darling, attracting trillions of dollars in assets. However, the crash of 2008 placed hedge fund managers in an uncomfortable spotlight. Many were quick to blame them for investing in unsustainable mortgage-based securities, which are what sparked the economic unraveling.

Between 2009 and 2018, annualized returns fell from 30% to 6.09%. This means that hedge funds have on average underperformed the market in the years following the crash. However, fees have largely stayed the same. Normally, managers charge 2% of assets and 20% of profits. And due to a rise in inexperienced traders, closures are not uncommon. For every successful hedge fund, another loses spectacularly.

What financial media once touted as the sexiest investment option has now started to turn people off. The running joke is that hedge funds are, in fact, just a compensation plan for their owners, even when returns are close to nonexistent. The only consistent performers in recent years have been those who bought into tech giants, which have largely driven the market’s massive gains. Then again, just investing in the S&P 500 would have gotten you a better result.

Yet the myth of the genius hedge fund manager, who will beat the market and make superhuman returns, is still alive and kicking. Speaking of superhuman, around one-third of hedge-fund assets are now partly run by AI. So-called “systematic” funds follow investment rules based on an analysis of historical data and use algorithms to execute trades. The final investment decision is still made a breathing human, however, and is therefore still susceptible to human errors.

If you’re lucky enough to have the funds, think twice before investing in a hedge fund. At the very least, do your research about the fund managers so you don’t get pushed off a financial ledge.

Saving for rainy days or for investing

Saving for rainy days or for investing:

Future is full of uncertainties and being financially secure is one of the targets that people should pursue. Saving money for rainy days is an expression often quoted to stress the necessity to save. Emergency fund created for extra occasions or for retirement is the usual means of saving. It is really important and any extra income should be set aside for saving purposes. However, another important target for saving money is often neglected when discussing purposes of saving and that is saving for investing. In our view, it may be even more important than any other financial target due to the reasons we are going to discuss in this post. Let’s go on a quest to find out the benefits of saving for rainy days and for investing.

The benefits of saving for rainy days

Available money for emergencies

There are plenty of expenses that may arise due to unforeseen circumstances: medical expenses that are necessary to cover medical bills, loss of job (income), repair of your property (car, house). The money put aside for these emergencies will allow you to deal with the issues immediately instead of having to borrow to solve the issues.

Extra funds for retirement

When you quit your regular job and retire your income from work will stop coming, and you will need to have extra money to live on (apart from retirement funds). Your savings stored up for that purpose will come in handy then. They will substitute the income you used to get from your job and you will be able to maintain the lifestyle you are used to.

Extra cash to pay for education or starting a business

Getting education becomes more expensive every year and if you do not want to take a loan to cover the expenses for studying you should consider saving. The same is true if you intend to start a business. You will need extra funds to do that. Start-up costs may eat up quite a chunk of your savings before your business starts running successfully.

Inflation may erode all of your savings

If you do not find how to increase your savings and they grow just by means of you contributing regular amounts you will lose a significant value of your savings (and the benefits savings create) in the long run. Why? Inflation will erode some (or even big part) of it. Money loses value over the time even in such low inflationary geographical areas as Europe and in such high inflationary zones as Venezuela or Zimbabwe, not only money, but all of your savings become worthless.

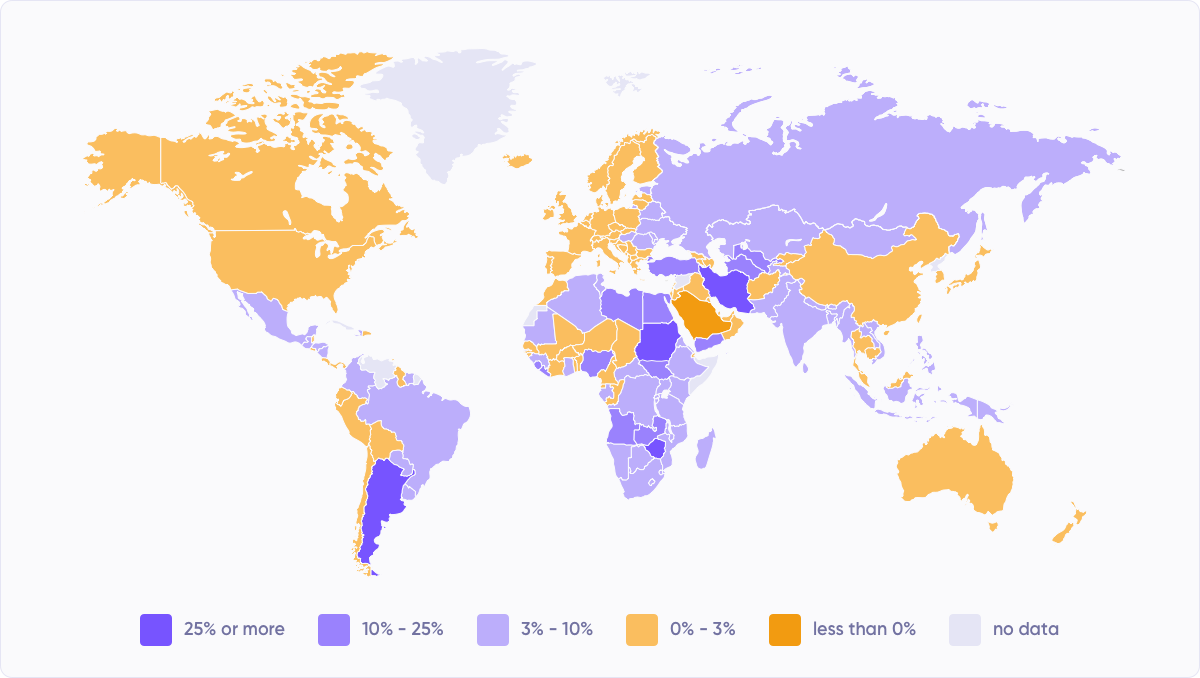

Below is the world map of inflation (from IMF – International Monetary Fund) in various geographical areas. Check out what percentage of value money loses each year in the region you live in.

Source: imf.org

While inflation in Europe is just 2.2%, it would mean that all goods should double in price every 31 years. From practice, we know it happens faster for the most commonly used goods (particularly food). Under normal circumstances, prices double every 28 years. However, various factors make inflation in different regions jump up and down (despite the fact Central banks implement their monetary policy to keep inflation under 2%). The table below is a reference of how fast prices would double in various geographical regions if inflation there stays at the current levels.

Despite the fact, Europe and North America are able to contain inflation, there always are periods of high inflation in each generation and every region/country due to systematic changes, geopolitical/financial uncertainties, crises and many more. In 1946, Germany experienced hyperinflation of 41.9 quadrillion percent (prices doubled every 15.3 hours), Argentina – 59% in 2019 (May), Ukraine – 47% in 2015, Turkey – 25% in 2018, the United States – 20% in 1917. This proves that prices for goods may double faster than is shown in the table above. Thus, savings may lose value faster than you can imagine. How to protect the value of your money and savings?

Saving to invest is the solution

Regular saving and investing are one of the best ways to preserve your capital from being eaten away by inflation. Savings accounts, unfortunately, do not serve well fighting against inflation. Even in low inflationary regions such as EU or North America, keeping money in savings accounts in the commercial banks will keep you losing money to inflation. In both the US and EU the rates for savings accounts stayed at 0.20-0.30% from 2009 to 2018. In the US, after the FED started raising rates in 2018, it gave a small boost to the rates for savings accounts, but the average rates merely keep up with the current inflation of 2.2%. In the EU, after the ECB introduced a negative interest rate investing in savings accounts remains highly unattractive (currently at 0.37%) and surely loses to inflation.

Most popular investment options in relation to inflation

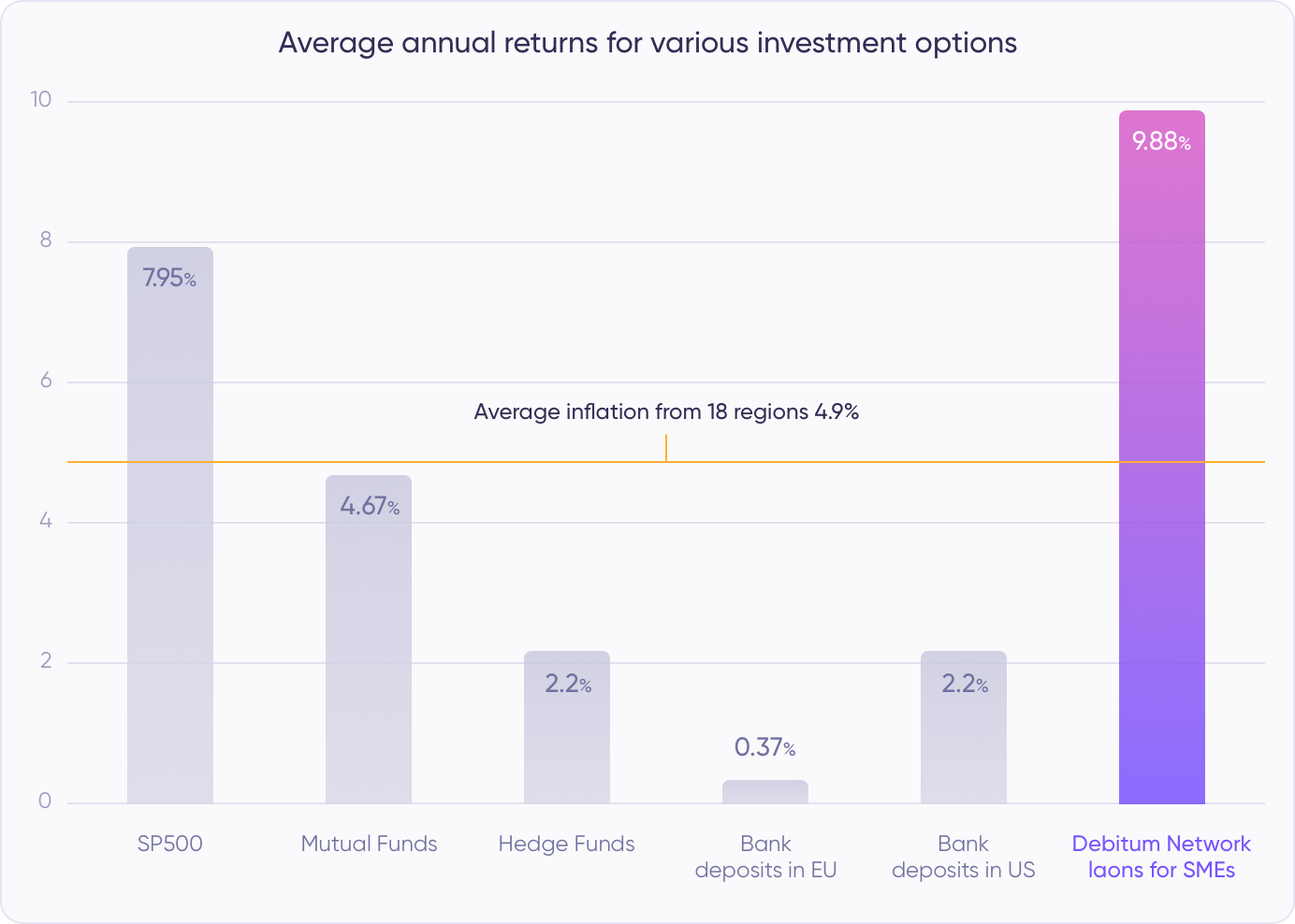

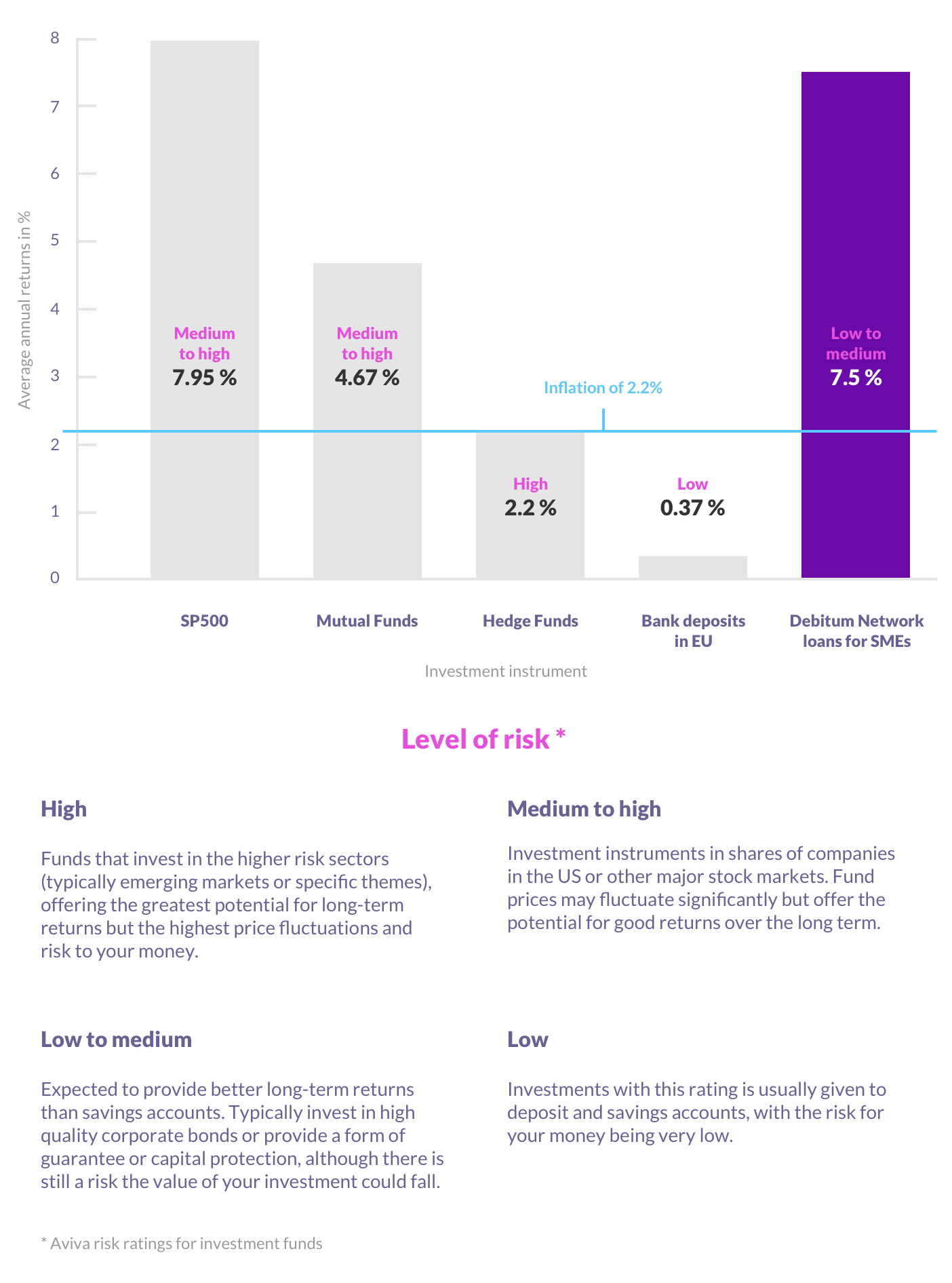

Average inflation in the world is at 4.9% now and of the selected investment options only SP500 and assets on Debitum Network help you to beat inflation and preserve your capital. Other options leave you in a deplorable position as your money and savings keep losing value every year. SP500, by the way, falls within the risk category of medium to high, which means that potential offered returns, in the long run, are good. However, prices and values of the securities or funds may fluctuate significantly and cause big swings in your portfolio, which not every investor can handle well. On the other hand, investing in Debitum Network assets falls within low to medium risk category meaning the quality of investments are higher and they provide better guarantees and capital protection than stocks or similar kind of securities. And the returns are higher than for more volatile investments in the most popular stock index in the world!

Overcome inflation investing in the assets on Debitum Network platform

The average interest rate paid to investors on Debitum Network platform is at 9.88%. This annual return will help you to stay way ahead of annual inflation in Europe and globally. Extra safety measures such as reliable risk assessing and a buyback guarantee make the investment in the assets quite a safe choice. The minimum deposit amount is just 50 EUR and the investment amount just 10 EUR. Register and start earning interest right away. We have selected an asset of the week to help you choose where to invest. Check it out.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Beating inflation with compound interest investing strategy

Beating inflation with compound interest investing strategy

Losing money to inflation?

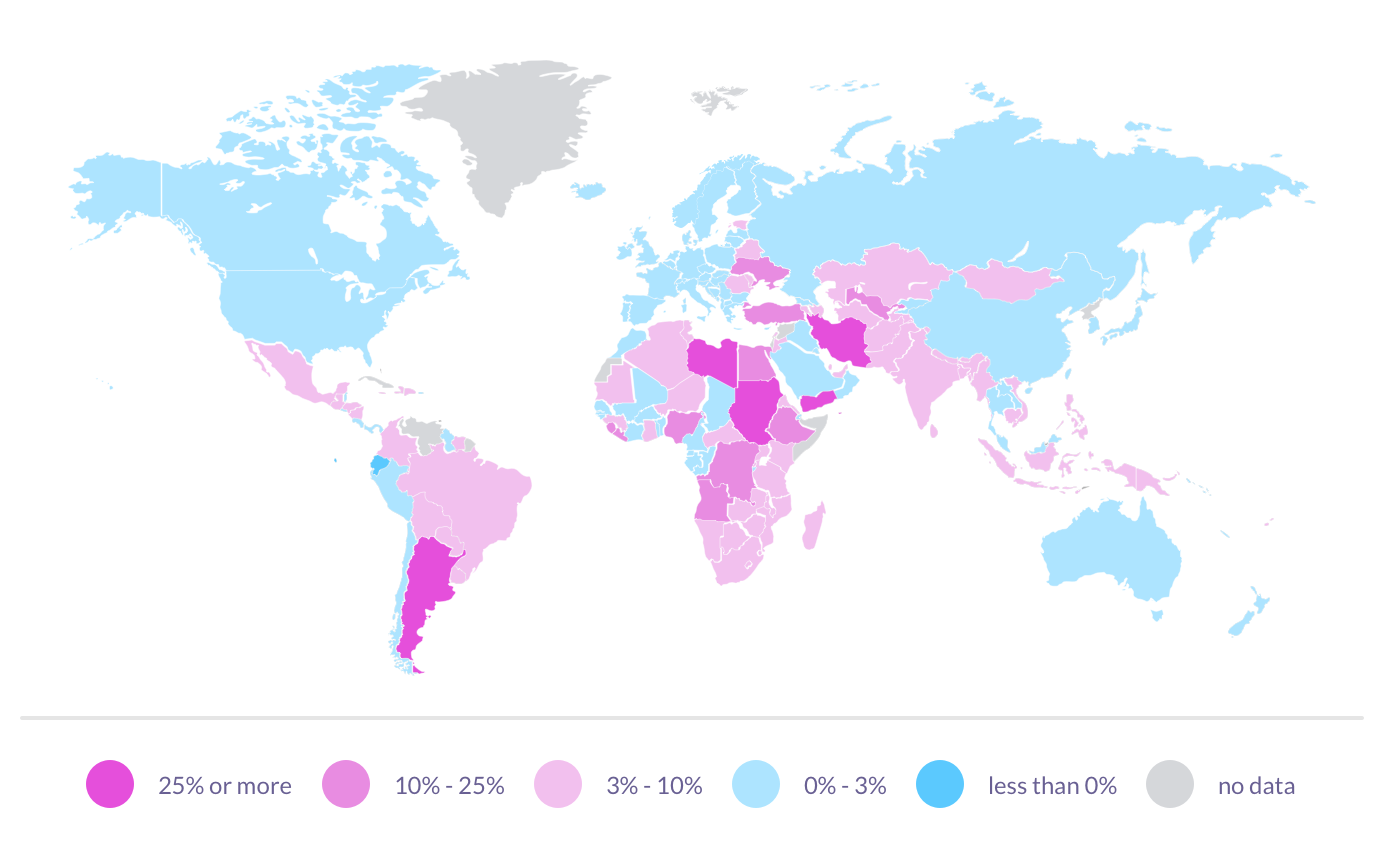

It is a proven fact that the amount of money you have today is worth more than it will be in the future and in places like Venezuela or Zimbabwe, unfortunately, your money, eventually, becomes worthless. This happens due to a process of inflation, which is a devaluation of the value of your money over the time. If not invested, your money will buy less than it can today. You do not have to be super smart to understand that as prices in shops rise sooner or later and you have to pay more for the goods you consume on a regular basis. Just to give you a current inflationary picture in different regions of the world in 2018 we have put you a world map of annual inflation from IMF (International Monetary Fund) to see how much value money loses in various parts of the world each year.

Data source: IMF DataMapper

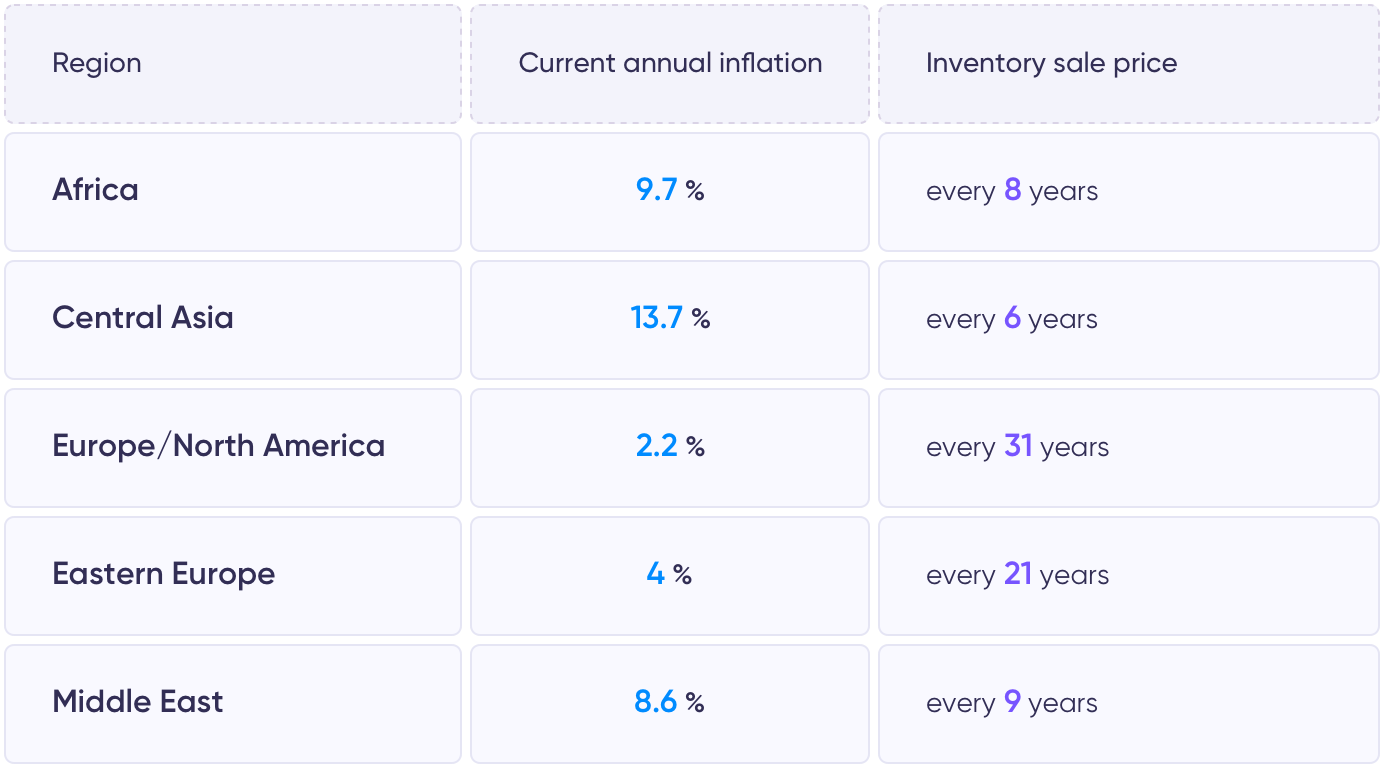

The numbers may not look alarming to you, but if you do basic calculation you will find out that if prices stay the same for a prolonged period of time, consumer goods in Central Asia and Caucasus (the highest level of inflation) will double in price every 8 years and in Europe (the lowest level of inflation) every 45 years. Despite the fact, the inflation stays low in Europe for the time being, if an average young person living in the region does not find a way to increase his income he will find his financial well-being drastically diminished by the time he reaches the age of retirement. How can we preserve our money and possibly increase it while living in an inflationary economic environment?

Investing in financial instruments with the best annual returns

Most economists and financiers agree that investing is a way to preserve your capital from losing value to inflation. Market analysts and experts try to single out the best investments out there that could beat inflation and put an investor ahead of it. For quite some time, the most popular investment options have been SP500, mutual funds and hedge funds. Let’s see how well those perform annually and also add two more investment options: average interest rates for keeping money in a bank in EU as well as investing in short-term loans at our own Debitum Network platform and we also added a risk level for each instrument (used by Aviva group to evaluate risk of investment funds). Then, let’s try to figure out how each instrument performs in relation to inflation in the least inflationary economic area the European Union where annual inflation on average is 2.2%.

Comparing the numbers in the chart with the inflation in the least inflationary region of Europe we learn the following: keeping money in savings accounts in a bank (in EU) will put you in a losing position in terms of inflation. Money invested in hedge funds will help you to stay at break-even with inflation (ironically speaking, this is the riskiest type of investment). You will be 2.6% ahead of inflationary pressure if you put your cash into mutual funds. The best performer in the basket is SP500 that puts your returns well ahead of inflation by 5.75% and the next best option is short term loans on Debitum Network platform helping you to move ahead of inflation by 5.3%.

What if you live in a more inflationary economic area such as Africa, the Middle East or Central Asia? None of the above mentioned investment options would protect your capital from being corroded by inflation. Even the best options indicated in the table above put you behind by around 5% to say nothing of the other less profitable choices like hedge funds or keeping money in a bank. Furthermore, it is obvious that inflation will not stay that low as it is now with very low base rates set by Central banks. It will pick up and an investor will have to search for extra sources to improve on the returns. What could be the best solution to improve the returns keeping risk/reward ratio tolerable? This brings us to the idea, which the legendary scientist Albert Einstein, presumably called “the most powerful force in the universe”. And that power is the ‘compounding interest’. What is it and how does it work?

Investing in financial instruments where interest compound

As opposed to simple interest rate, compound interest rate account earns money, not only on the money invested but also on the accumulated interest of the previous periods.

The formula for compound interest can be calculated in this way:

“Compound Interest = Total amount of Principal and Interest in future (or Future Value) less Principal amount at present (or Present Value) or = [P (1 + i)n] – P

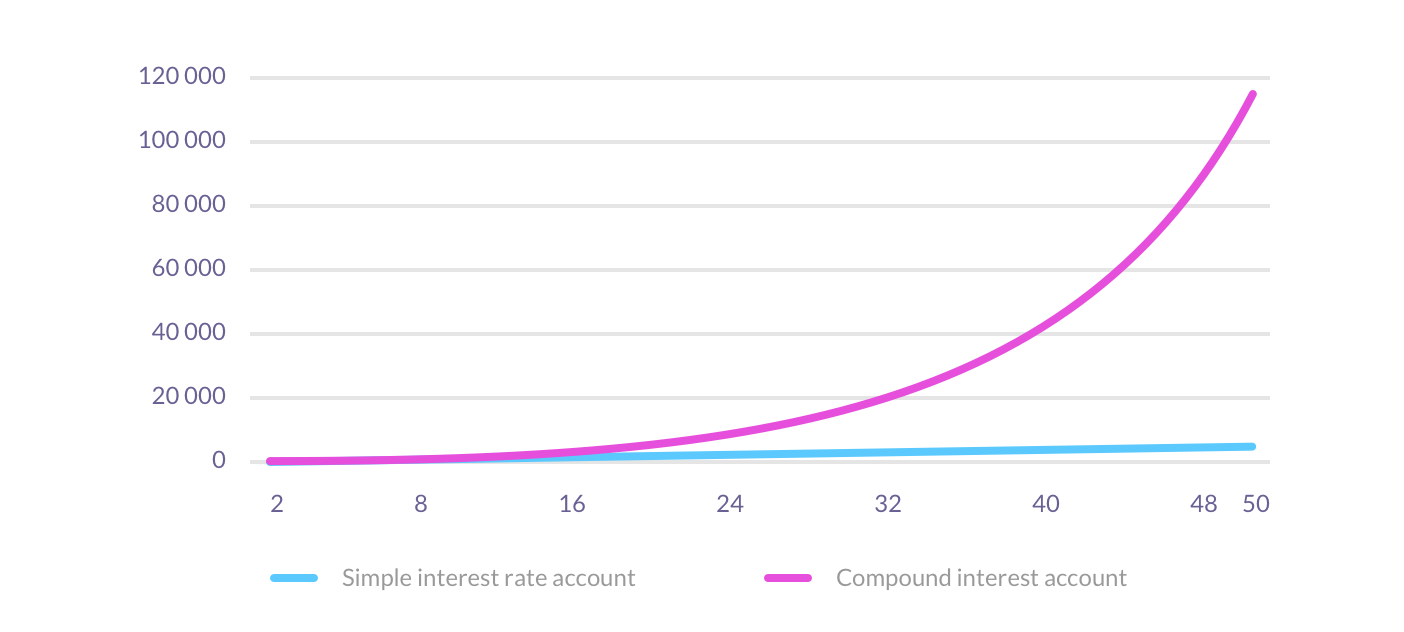

For example, you invest 1,000 Euros at an annual interest of 10% for both simple and compound interest rate (compounded once a year). At the end of the second year, you will have 1,200 Euros on a simple interest rate account and 1,210 Euros on compound interest rate account (compound interval once a year). If that does not look much, look what happens if you keep the money in the account with the same interest (compounded once a year) for 5, 10, 25 and 50 years.

The acceleration of compounding

Looking at the chart above we will arrive at a universal truth, that the sooner you start investing and the longer you do it, the better returns you will achieve due to the tremendous fact of acceleration of compounding. Initially, your simple interest rate account and compound interest rate accounts do not differ much, but as the time goes on we suddenly see a dramatic difference due to interest made on interest year after year. In the long haul, It will put you really far ahead of inflation even in if you live in high inflationary zones.

Increasing compounding intervals

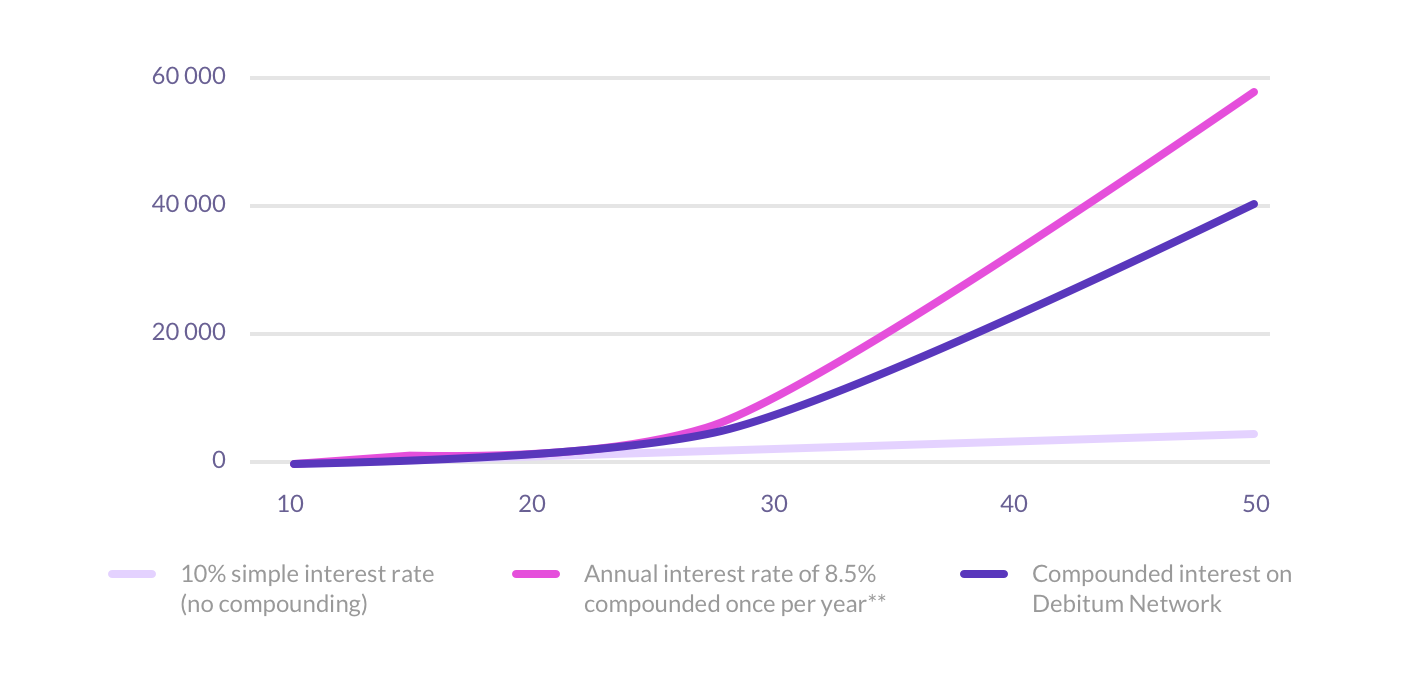

The example above was with the compounding interval once a year. We may take a step further and possibly increase the returns if the compounding interval was set to every month. If we take Debitum Network, where short-term loans are at 7.5% on average you can invest in one month loans and get compounded interest every month. In that case, you will earn an extra 0.25% on the first year of your investment. That may not seem much, but that’s very close to the annual interest rate that you will be offered for your deposit in European banks (on average).

How would you fare if you invested 1000 Euros with Debitum Network at an average 7.5% annual interest rate compounded interval every month, 8.5% compounded once a year and simply put the same amount for 10% simple interest rate into a savings account for 5, 10, 25 and 50 years respectively?

It is interesting to note, that just 1% higher interest rate (8.5%) compounded once a year with a portfolio of 1000 Euros would have done better than portfolio (same amount) with 7.5% (annual interest rate) compounded every month. This shows that the effect of compounding is more powerful over a longer period of time, not the interval of compounding. Similarly, 1% bigger interest matters a lot in the long haul. On the other hand, a portfolio with the higher simple interest rate (not compounded) over a long period of time falls extremely behind in relation to both other portfolios (compounded interest) by 8.2 and 11.6 times respectively at the end of 50 years. This, again, justifies the fact that the earlier you start and the longer you keep your money employed, the larger your portfolio grows and the best part is, that it happens exponentially. Investing in the most popular options such as stock indices, mutual funds or hedge funds does not even offer you a possibility to compound interest the way you can do it with Debitum Network.

Our platform gives you the advantage to pick loans with flexible amounts and duration. So, you can invest monthly and earn interest on both principal and previous interest of the loans, thus compounding interest bit by bit and as time goes on see how your earnings accelerate. We know that investing for 50 or 25 years with one company may seem too far-fetched, but the illustration above is given for the sake of showing you how compounding works and how returns accelerate with each consecutive year. That’s precisely why a smart investor like Warren Buffett believes that starting to invest early and keeping it doing it till you retire will create you a nest egg and make you financially prosperous due to the compounding principle.

Ready to earn compound interest?

The good news is that investing with Debitum Network, not only allows you to earn compound interest, but each loan on our platform carries an additional guarantee (personal guarantee from owners, accepted invoices from large companies or guarantee by another company or a buyback guarantee from a broker), thus making your investments with us less risky. We do believe that safer investments are possible and high returns come with time and with the help of compounding interest, but never at the expense of the safety of your money.

If you want to try our platform and see how you can compound your interest in short-term loans you are most welcome. It does not cost you anything to open an account, we do not have any hidden fees and you can stop investing any time you want.

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

How do returns in short-term loans for SMEs compare to investments

How do returns in short-term loans for SMEs compare to investments

Investors will always seek how to deploy their money and diversify them, considering risk, expected return, and available capital. Financial and investment analysts monitor various funds, indices and other investment options to figure out which investment portfolios earn the highest average throughout the years.

Investors, business people, and those, that amass considerable wealth state that they achieved it not by saving, but by investing. It is a well-confirmed fact, that saving, actually, will cause you to lose money. As annual inflation (in the World) is around 4% and keeping money in a commercial bank (at least in Europe) would not earn, but cost you money due to low-interest rates, letting your money sit in a bank, or at home in the form of cash.

This is by no means to say, that one should not save. On the contrary, we do know that overspending and excessive borrowing leads to severe economic problems on both personal and national levels. On the other hand, capital kept in a bank or in cash will lose value as time goes by.

Long-term conservative investments

Long-term investors that are more interested in a more conservative and secure way to invest, such as bonds or value stocks would be looking for a reliable mutual fund or a stock index, preferably, SP500 to open a long-term position. It is natural, that these types of investments do not usually give one high returns.

Just for the sake of comparison, we may look at what one would have averaged annually if he/she invested in SP500 index, an average mutual fund or an average hedge fund.

SP500 – 7.952%

Mutual funds – 4.67%

Hedge funds – 2.2%

As we may see, investing in the stock index of most popular US stocks would have given you the best annual return. The percentages differ very little if you take into account 10, 20 or 30-year performances. The data for hedge funds encompasses 9-year period, which means that overall return over 9 years investing in hedge funds would have averaged you 2.2 percent annually (or 22 percent in 9 years). The Omaha legend Warren Buffet placed a bet of $ 1 million that it was not possible to put up a portfolio of hedge funds that would outperform SP500 Index fund over a 10-year period. Looking at the above given numbers, it seems obvious that Warren Buffet is going to win the bet.

Aggressive and high risk/reward-based investments

Of course, if you are an insightful stock picker that may spot a growth stock which is about to soar, these percentages may not attract your attention, and you would probably be more interested in big risk/reward ratio assets. However, these require excellent analytical skills and a strong stomach to see stock soaring (making you huge profits) and then collapsing (watching those profits dwindle).

A lot of risk traders wait for strong market trends to develop and use high leverage to trade various financial instruments: stocks, commodities, currencies or other securities that offer very attractive returns with extra increased risks. When the market goes against them, they often have to cut their losses and do it fast as these savvy traders typically have a specific pre-set percentage loss of their equity when they close all open positions.

These investors also look for IPOs and Startups that would generate them hundreds, possibly thousands percentage return on the investment. As you may know, statistics show that around fifty percent of those fail within the first year and most of the rest do not generate enough profits. Just about 1-2 percent of the companies may give back the investor huge returns.

The golden middle –average risk/reward returns in short term loans

There is a middle path – alternative finance and investing in short-term loans. This is a quite attractive and moderately risk-averse type of investment. Investments in these are short-term, typically last from a few weeks to a half year. However, an investor can reinvest his money and interest earned by choosing various assets with different maturity periods. Debitum Network platform Abra 1.0 has just launched and investors can invest on an average annual interest rate of 10-15%.

Try Debitum Network platform

As one may see, there are plenty of opportunities for various types of investors in the current financial system. It does not matter, whether you are more risk averse, risk investor or fall somewhere in between. Taking aside financial markets, we want to draw your attention to the rising market of alternative lending for small businesses with Debitum Network being one of the ice-breakers in the field. Opening an account takes a few minutes and the minimum deposit is just 50 Euros. Interested?