Tag: P2P platforms

Peer-to-Peer Lending: Friend or Foe?

If you have some spare money, it may seem tempting to invest in peer-to-peer platforms. P2P lending is a type of crowdfunding that connects borrowers and lenders without the involvement of a financial institution. They’re more predictable than stocks or cryptocurrencies and seemingly require less financial knowledge. Plus, they offer decent returns. So, what’s the catch?

For one, the market still lacks regulation, creating the potential for unfair business practices. The collapse of P2P companies such as Kuetzal, Monethera, Grupeer, and Envestio makes that very clear. These platforms all offered buy-back guarantees and high yields. In the end, they all had failed business models or were outright scams. Several featured made-up projects on their platforms that an observant investor might have noticed. But they knew that the average investor lacked the know-how (and even the interest) to perform due diligence. In the end, they ran off with lots of money and left their dumbfounded investors empty-handed.

What are some of the warning signs you should look out for? A promise of unrealistically high returns is one. There’s no such thing as low risk – high return. The higher the return, the bigger the gamble. It’s always worthwhile to look past advertising catchphrases and dig deeper into the company behind the platform.

Before registering, you should make sure you’re able to find information about the platform’s owners. Make sure key management staff are not connected to money laundering scandals and that the company offers full disclosure of loan originators and borrowers. It’s also important to make sure that the buyback guarantee is not provided by a 3rd party and that the company uses a bank account from the same country that it’s registered in. The owners should be willing to share a template of the loan agreement before you sign up.

Though it might seem tempting to rely on well-written, fact-based reviews performed by 3rd parties, you should take those with a pinch of salt. Many P2P bloggers get a small sum for everyone they sign on, so they make money even if you end up losing everything. If that sounds a bit like a Ponzi scheme, that’s because it sort of, kind of, maybe, is.

If a P2P platform does seem legit and you decide to invest, be sure to check the fine print. Many of these companies lock up your money for many years, and if you want to withdraw early then you’ll lose lots of cash. Oh, and check the service fees, as those will diminish your profit. Overall, P2P platforms are risky and have some less-than-appealing terms, so maybe it’s best to just steer clear of them.

Moral debate: lending to businesses or issuing payday loans

Moral debate: lending to businesses or issuing payday loans

Lending at interest has caused lots of debates over centuries. In the middle ages, it was considered outright evil. Nobody thinks like that anymore. Lending institutions (banks) have become the largest business enterprises in the world. Borrowing and lending have become an inseparable part of business and economy growth. Both businesses and people borrow for a variety of reasons. The key question remains the same – at what price (interest rate).

In post-2009 crisis era, Central Banks have slashed interest rate close to zero. Keeping money in the savings accounts may actually cause one to lose money due to the inflationary economic environment. P2P platforms have become an attractive solution for investors that expect above-average returns on their investments. However, the issue of moral responsibility of lenders to provide qualitative services at reasonable interest rates remains of paramount importance due to a large number of online lending platforms and lack of accountability of some of them.

Payday loans and the issues connected to them

These are typically small amounts of money lent at very high-interest rates with the agreement that the money will be paid back when the borrower receives the next paycheck.

The size of a payday loan market is really huge and there is quite a large number of people who take out the loans. According to the research, around 12 million Americans take payday loans each year and spend around $7 billion on loan fees. The annual percentage rate on those fees ranges from 300% to 500%. The situation in Europe is quite similar.

In comparison, an average percentage rate on credit cards would be way smaller 15%-30% and 10%-25% on personal loans in a bank or credit union. Why would any person go to take a loan and pay such inconceivable interest rates to a payday lender? The same research shows that most customers of payday lenders are mainstream workers with the lowest annual income. Most of them do not qualify to get credit cards, have a very poor credit score, lack access to credit, and face regular financial problems. An average person in need to cover utility bills or short-term needs can use a credit card, while the people who don’t have to turn elsewhere to gain the necessary cash will go to payday lenders. Unfortunately, high-interest rates charged by payday lenders leave those people in an even worse financial situation than before the loan.

Short term repayment demands remain huge and borrowers have to return the loans within a short period of time, often cutting a huge amount of cash from their paycheck. However, there is another utility bill coming or need to buy food or pay the rent and if the borrower fails to pay off the entire amount fees, interest and penalties keep on growing, thus putting the borrower in an even more dire situation.

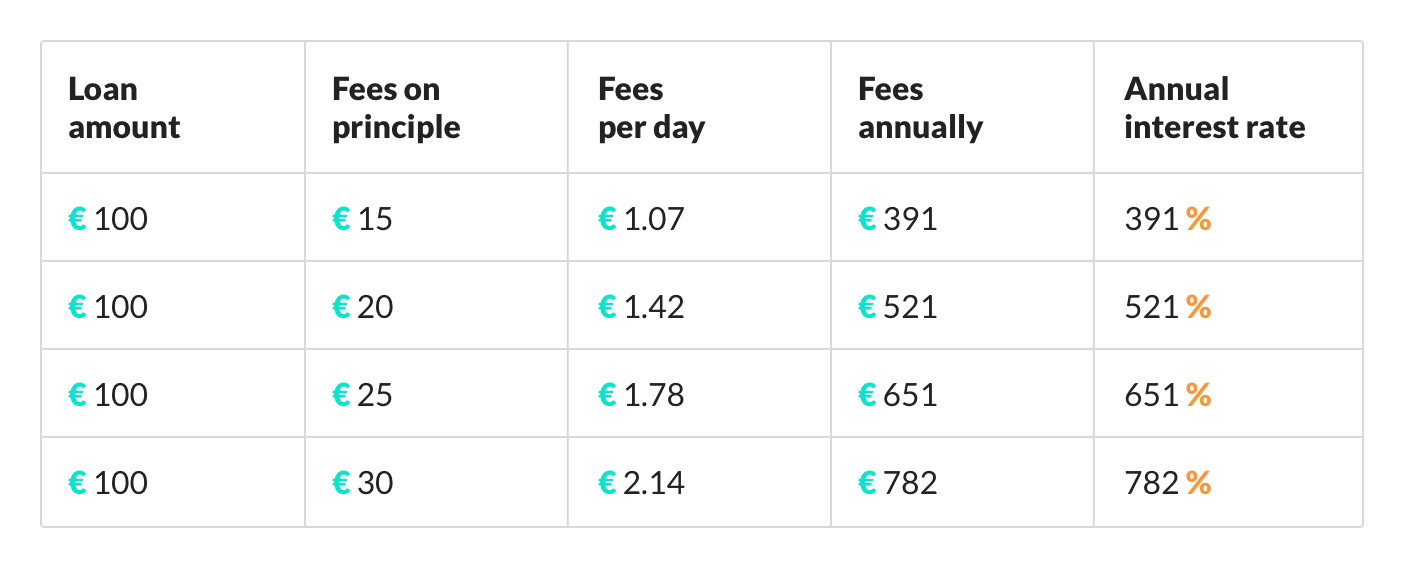

We may look at the price of a typical loan to the customer (borrower). Let’s say a short term payday loan is 100 Euros with a 10 Euros fee for 2 weeks. At the end of two weeks, a borrower will have to pay back 110 Euros to the lender. Let’s do the math and see how much it would cost a borrower to pay back the loan in a year.

EUR 10 / 14 days = EUR 0.71 per day

It does not look much, right? However, how much would you pay after a year?

EUR 0.71 x 365 days = EUR 261

Thus, apart from 100 Euros of principal, you would have to pay extra 261 Euros in fees (or interest), provided you pay off the loan in time, without delay. The annual interest for the loan would be 261%.

What if the fee is 15 Euros on 100 Euro loan, or even worse if the payday lender charges 20, 25, or 30 Euros on 100 Euro loan?

Let’s do the math and see how much it would cost a borrower to pay per day and annually.

So, if the payday loans are used often, or loans are rolled over to several terms it will become very costly to end users, who, as we have stated are cash negative. Fees grow exponentially throughout the year doubling, tripling or even increasing as many as 7 times of the original amount of a loan. Taking these type of loans may crush any borrower financially very fast. Then only short term benefit of these loans is that a borrower will cover his short term needs.

Credit gap for SMEs and advantages of lending to businesses

On the other hand, businesses around the world are always in need of funds to fuel their daily operations. In fact, according to Forbes, the most common cause for bankruptcies of companies within the first years of business is lack of access to funding. This is particularly true for small and medium-sized companies as banks are unwilling to lend to them. The gap of unfunded SMEs around the world widened from $2.6 trillion to $5.2 trillion. The reason was the main cause for the rise of alternative lending platforms such as Funding Circle, Lending Club, Mintos, Zopa, Ratesetter, Twino, Assetz Capital or our own Debitum Network.

The online p2p platforms that these companies operate have simplified lending process cutting paperwork to a minimum and reducing requirements for getting a loan. Take, for example, our partner and loan originator Debifo that puts loans (assets) on Debitum Network platform. It does not require long-term contracts or collateral and has no hidden fees. After completing a short registration form, clients can raise invoices for financing and receive the funds they need within a few days. The same procedure with the banks would take businesses 1-2 weeks. If young businesses can prove sales revenues exceeding 30 000 Euros, provide services and goods to other businesses and have been in business for at least 6 months, they would not have problems with getting funds. On the other hand, banks would not finance companies that have short business history, lack of real estate collateral or personal guarantee. Thus, a new market of alternative finance that provides necessary funds for SMEs has been growing steadily for over a decade.

Benefits gained from lending to businesses on alternative finance platforms

Lending to businesses creates far more advantages than disadvantages for companies that borrow and investors who invest in the loans (effectively becoming lenders in the process on P2P platforms) and loan originators, who can be more assured that the loan will be repaid. Here are some of the benefits of the lending process on such online platforms as Debitum Network:

As we may see from the points above, alternative finance has become not only a way of alternative lending but due to online P2P platforms – an excellent way to invest and diversify. In comparison to other traditional investment options, investing in short term loans for SMEs offers far more attractive returns than the traditional ones. You can read more about it in our blog post where we outlined all the advantages of investing in short term loans.

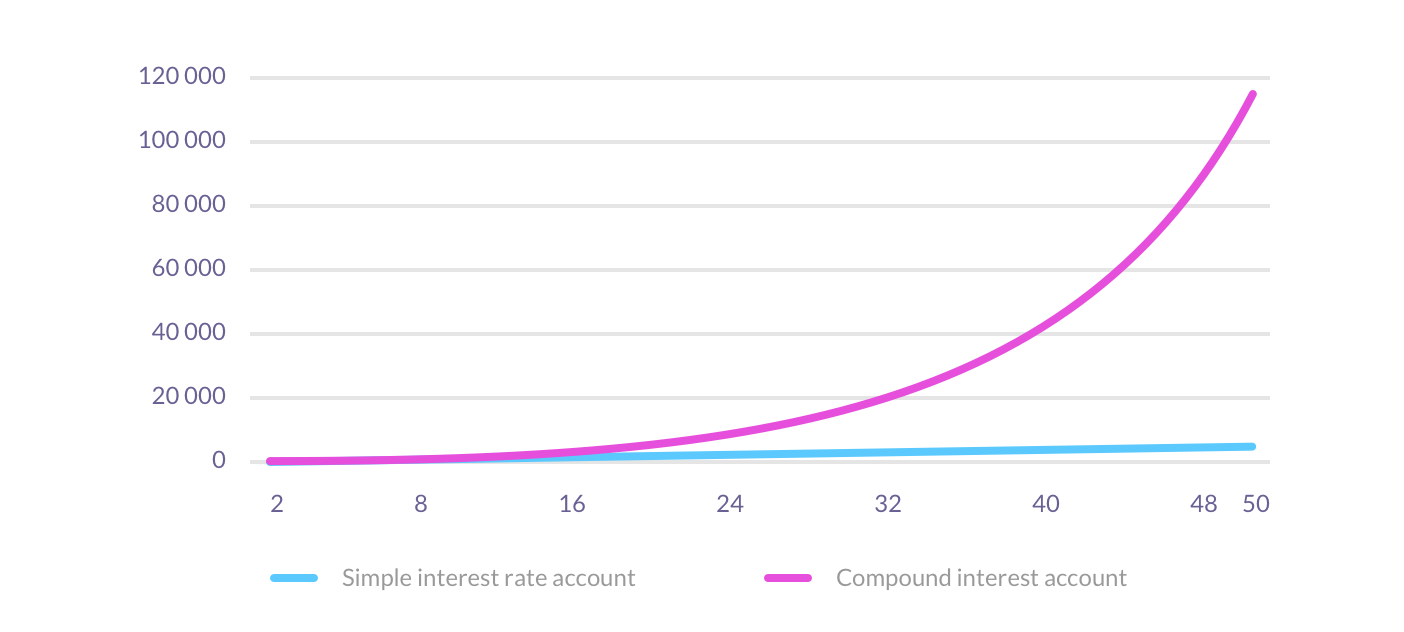

We have done calculations how much an investor can make if he invests in short term loans and reinvests the principal and interest to take advantage of the principle of compounding interest investing in loans for businesses on Debitum Network platform. More on that can be found in this blog post. However, we would like to present a couple of examples to outline profits that compile in the long run due to compounding.

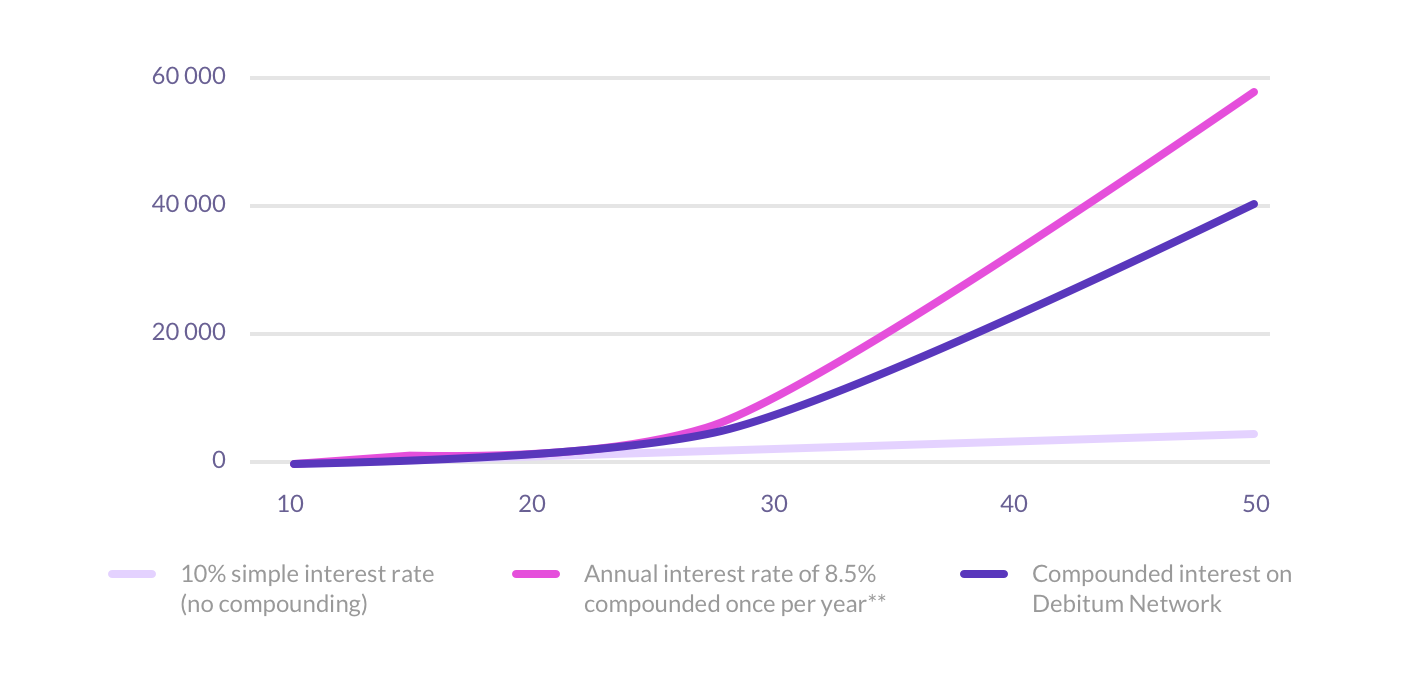

For example, you invest 1,000 Euros at an annual interest of 10% for both simple and compound interest rate (compounded once a year). At the end of the second year, you will have 1,200 Euros on a simple interest rate account and 1,210 Euros on compound interest rate account (compound interval once a year). If that does not look much, look what happens if you keep the money in the account with the same interest (compounded once a year) for 5, 10, 25 and 50 years.

How would you fare if you invested 1000 Euros with Debitum Network at an average 7.5% annual interest rate compounded interval every month, 8.5% compounded once a year and simply put the same amount for 10% simple interest rate into a savings account for 5, 10, 25 and 50 years respectively?

All participating parties benefit

The examples clearly show the lending process can be beneficial for investors. Those that invest in the loans earn exponential income over the years as the principle of compounding accelerates profits from both interest and principal. However, not only investors benefit from the process. As investors reinvest their money in short-term loans, businesses regularly get the necessary funds for functioning and can keep on borrowing. Loan originators that provide money to borrowers that are able to repay the loans have fewer defaults that those that keep on doing business with private individuals (that mostly borrow for consuming) and thus can function unobtrusively and be confident that lent funds will be returned.

Having looked through the facts regarding payday loans and lending to businesses we can clearly state that payday lending, actually, does more harm than good for those who take them. It also damages the image of lending due to extraordinarily high-interest rates and the harm it does to average borrowers. The only beneficiaries in the process are those that issue those loans – payday lenders. Unfortunately, a huge number of defaults on these type of loans may actually cause a payday lender to go bankrupt too.

On the other hand, lending to businesses at reasonable interest rates creates inherent value for all parties participating in the lending process: companies that borrow, investors that invest in the loans, loan originators that issue the loans. The process leads to job creation and growth of the economy in general too. Furthermore, it may sooner, or later become a real competitor in terms of investment to traditional ways to invest due to a quick turnaround of invested capital and the principle of compounding interest.

Ready to invest in business loans?

We want to offer everybody a possibility to take part in the lending process by investing in short term loans for SMEs. Minimum deposit is 50 Euros, minimum investment just 10 Euros. Interested?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What makes any investment safer?

What makes any investment safer?

Investing is always associated with risk. There are no 100% safe investments. An investor always looks to balance the acceptable level of risk with potential reward. Some are willing to bet on EUR/GBP exchange rate fluctuations in the face of Brexit with 20x leverage on some retail Forex platform, while others are so risk-averse that they choose to lend to Germany, while Germany 2-year bonds are still providing negative returns of -0.6%.

The rule of thumb has not changed, though – the higher the risk, the higher the expected return. However, the returns, in case of lending would be hypothetical as riskier investments will have a higher probability of default, thus bringing the overall net return down. While Germany has its risk rating at AAA (default risk too small to understand – 0.00003% in one-year period or 0.00550% in 10-year period) or has its creditworthiness even as high as 100 out of 100 (the latest rating by Trading Economics), we expect that any amount lent to Germany will be returned as promised – no real risk for an investor.

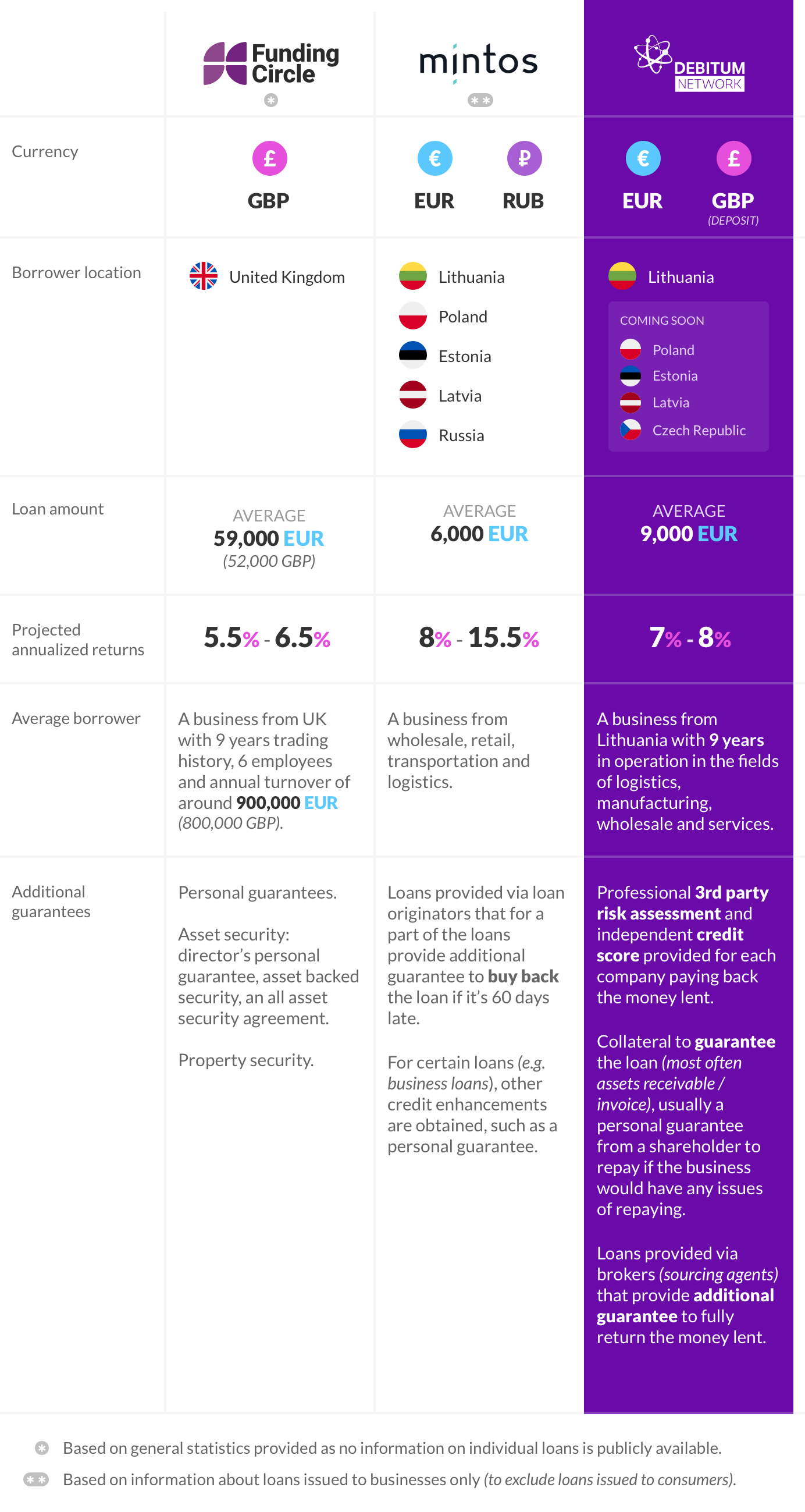

A more riskier option is investing on Peer-2-Peer or Peer-2-Business platforms with considerably higher returns. P2P or P2B solutions offer a possibility for an investor to directly lend to an individual or business that needs funding. Such solutions offer returns somewhere in the range from 5% on Funding Circle (Conservative lending option) and Debitum Network 7.3% to around 12% on Mintos (average historical return). Then, there are platforms like Bondora that offer an average interest rate of 32.5%, while the average net return is only 10.1% with 1 out of 5 investors losing money. The latter illustrates the point of a need for safer investments perfectly; as potential returns increase, so does the risk of losing one’s investment.

Safety is one of the key values at Debitum Network. When we started creating our platform, safety of investors’ funds was at the heart of it. Therefore, we chose to concentrate on loans to businesses, which have a much higher chance of repaying the loan rather lending to individuals. That allows Debitum Network to offer investment in business loans with average annual interest of 7-8%.

Let’s compare other details than interest rate for an average business loan currently available on the solutions mentioned earlier – Funding Circle, Mintos, and our own Debitum Network:

Businesses will hardly ever borrow at high interest rates that some of the Peer-2-Peer lending platforms offer. Nor will they offer extra guarantees and take risks ruining their businesses borrowing at 15-20% annually. Thus, platforms charging over 10% interest on loans will be much riskier for investors and likely attract more private individuals than businesses to borrow from. Debitum Network aims to satisfy business needs to borrow at affordable rates, as well as investors’ needs to have their invested capital safe. Which brings us to our initial position of lending exclusively to companies and at reasonable interest rates of 7-8%.

In addition to what has been said, here are a few principles, which we believe makes lending to businesses on our platform safer:

|

Professional risk assessors |

Third party services such as risk assessment single us out from other P2B platforms out there. Local professional service providers know local business specifics and therefore are better able to evaluate companies applying for a loan with much better precision than any generic risk scoring algorithm done by a single loan originator or platform itself. For Lithuanian market, Debitum Network uses Scorify, whose credit score rating system GoScore has been used to issue over 380’000 ratings. It ensures higher professional standard and more precise credit score available for a user to make a better informed investment decision.

|

Strong businesses |

Borrowers on our platform are well established SMEs and only loans handpicked by experienced loan originators such as Debifo and scored above the minimal needed credit score by independent risk assessors are placed on our platform. So far, the companies that borrow on Debitum Network platform have been in business for 9 years on average and they have borrowed and repaid the loans before. Longevity surely means better safety! Most current available assets are invoice financing loans with final payers of these invoices are mostly large companies with average revenue of 700 million EUR. They have been in business for decades and are considered key players in the economic areas of wholesale, manufacturing, logistics, and services. As the companies that actually ensure money inflow to pay back the loan are handpicked and truly strong in their respective sector and region, the risk for a loan not to be repaid and investor losing the money is reduced.

|

Guaranteed loans |

Each available loan on our platform is backed by an asset as a collateral – be it assets receivable (approved invoice for goods or services sold), variable asset (trucks, equipment and other) or fixed asset (real estate property). Often, there are also additional guarantees from company’s shareholders or another partner company’s guarantee. Moreover, our loan originators (brokers) have started offering a “buy back” of a loan being late more than 90 days. However, to make sure they can execute such an offer – we request them to put funds aside in a reserve fund as well as provide certain financial covenants towards Debitum Network.

Interested?

For many investors returns of 7-8% per annum sound really great and this is exactly what Debitum Network provides. Of course, there are ways to try earning more; however, one should always remember that in the world of investment, any type of return is associated with a certain level of risk.

As described, we, at Debitum Network work hard to ensure additional safeguards for your investment, so you can lend to businesses and earn returns with fewer worries. We believe that a loan with independent and professional 3rd party credit score and at least a few levels of payback safeguards (collateral from the business, it’s related entities and a broker that is sourcing the loan) is worth funding. Would you agree?

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Investment series: analysis of an asset on Debitum Network platform

Investment series: analysis of an asset on Debitum Network platform

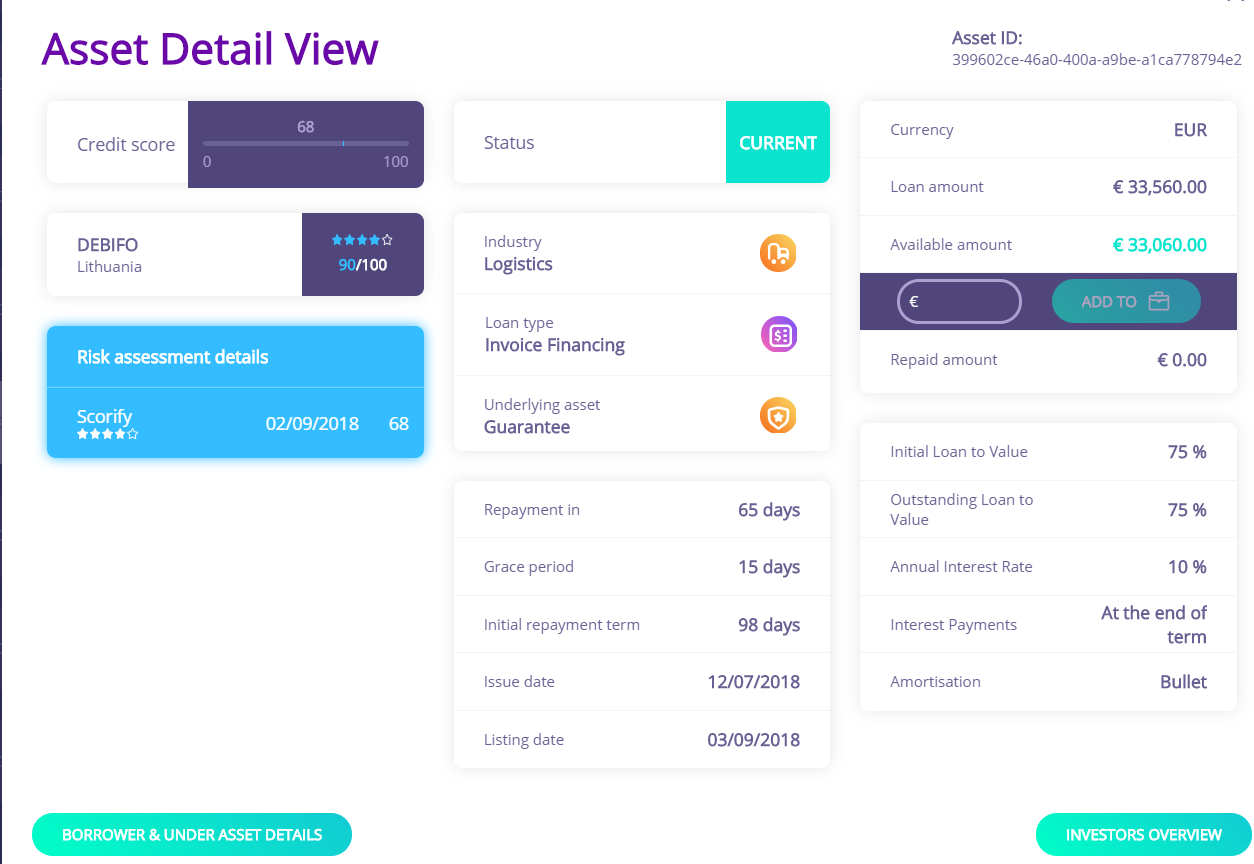

Debitum Network platform 1.0 Abra has been live for one month. Borrowers have uploaded the assets (short term loans) to be financed, a lot of investors onboarded and now anyone can participate in the funding process to help with the growth of SMEs around the world. We currently have 32 assets from various industries. You can invest in any of them. We decided to pick one asset and look at it more closely so that you could better understand what is what and how to invest in it.

This is the asset we decided to discuss. It has 65 days before the date of repayment. So, if you make up your mind to participate in the funding, you still have time.

1. The first item in the asset is an industry. Every asset is put into a specific industry category. This one belongs to logistics. Debifo (that collects invoices) told us that logistics is one of the most reliable industries and they hardly ever hesitate whether to take on an invoice from the industry.

2. The second item indicates who the broker that collects the invoice is. At the moment, the broker that puts most invoices on our platform is Debifo. It has been in invoice factoring business for over 3 years and was featured in Forbes among top five European fintech companies to watch in 2016. Another most recent partner providing invoices is Chain Finance. More partners loan originators will be soon.

3. Issue date simply states the exact date when the invoice was issued.

4. The next item is the number of days left till the repayment. This one ends in 66 days. Most loans are short-term, so you have quite limited time to consider what loans to invest in before they reach maturity term.

5. You can also see the country where the borrowing company operates. We have started our operations in Eastern Europe. This logistics company is from Lithuania.

6. Our short-term loans mostly belong to Invoice financing category. This one too. Invoice financing is a way for businesses to borrow money against the amounts due from customers. By pledging their invoices businesses can get the bulk amount much faster than they normally would.

![]()

![]()

7. Guarantee icon means, your investment is secured by a guarantee. It maybe backed by invoices, a personal guarantee from the business owner, another company or a buyback guarantee. To learn more about the specific guarantee of an asset go to next point.

![]()

8. When you press view, a pop up comes up. In it, you will see a summary with all info about the asset. Below pop up shows all the info about the asset we are talking about.

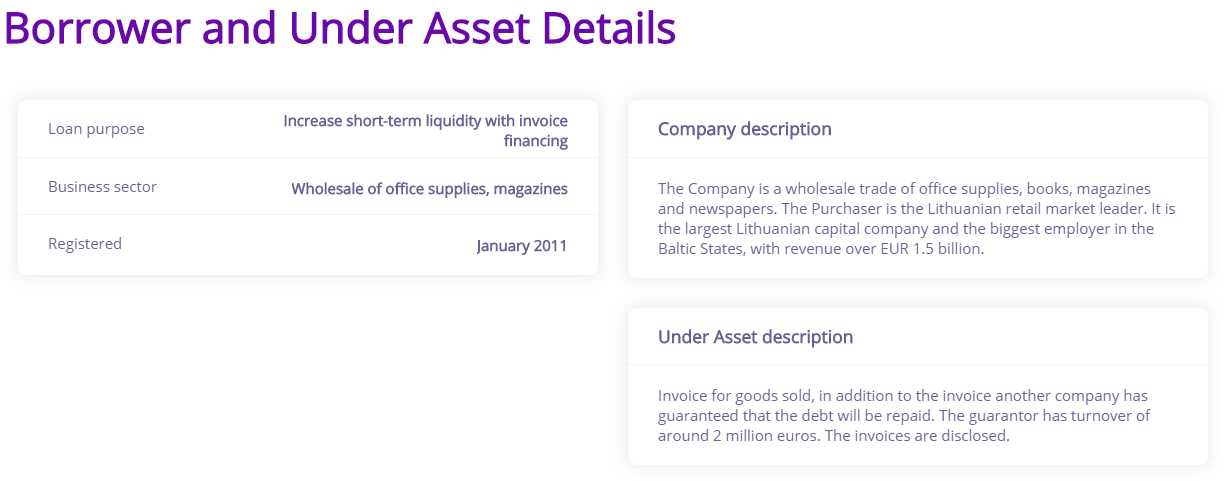

9. If you press “BORROWER & UNDER ASSET DETAILS”, you will learn more the purpose of the loan, a business sector the company is in, when it is registered, a quick description of the company and what kind of guarantee it has for the asset.

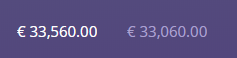

10. The next 2 items indicate the total amount of the invoice and the amount available (for investment). This one has 500 Euros covered and 33,060 Euros available for investment.

11. The percentage shows what is the annual interest rate for the asset. This one is 10%. This is how much you would earn if you kept your investment for the whole year. The number would be different as the maturity term is shorter.

12. The item below shows the credit score of a company. The higher the number, the safer the company, the lower the interest. The lower the number, the riskier the company is, the higher the interest rate. The higher is better, the lower is worse. The range for the score is from 0 to 100.

13. Below is the field where you have to enter the amount you want to invest in the asset. The amounts are flexible. The minimum is 10 Euros.

14. Add to briefcase icon is the last item on the asset. After you entered the amount you need to add it to briefcase by clicking ‘ADD TO’ briefcase. It is, then, added to your briefcase. You confirm it, and you have invested in the asset.

Ready to invest?

You can easily invest in any asset on our platform. Having chosen the asset you like, it is a matter of split seconds and you can start earning interest on that instrument.

Disclaimer: It is important to point out that the approach presented here is not necessarily suitable for everyone and is presented for information purposes only. It is not intended to be investment advice. You should seek a duly licensed professional for investment advice matching your specific situation.

Ways to get funding in alternative finance

Ways to get funding in alternative finance

Traditional way of getting a loan, that involves going to a bank and filling an application is probably the only way most people imagine. However, there are a lot of other ways to get funds for your small or medium-term business. Alternative finance p2p platforms such as our own Debitum Network or Mintos, Zopa, Funding Circle, Assetz Capital and others can offer you a few possibilities to choose from. This blog post aims at describing some of the most popular ways that alternative lenders provide funds to small businesses.

Equity crowdfunding

Equity crowdfunding is the process when, typically, a lot of people (crowd) provide money to small business in return for equity. Small businesses do it with the help of a crowdlending platform. This type of funding has been around for many years. However, in the past it would take big businesses or angel investors to provide the bulk amount of funds. In traditional IPOs, the starting sum would be $ 1 million. Nowadays, a lot of people with as little as $ 100 can participate in the funding process.

P2P lending

Peer to peer lending is online lending service that connects individual investors with borrowers and a loan is provided with an agreed fixed interest rate and maturity. Borrowers have their profiles on P2P lending platforms and investors may look at them, analyze past performance and determine whether they want to take risks lending money to that specific borrower. Borrowers can be both individuals and small businesses. An individual may provide a partial or full amount requested by a borrower. The rest money will come from other individual investors. To some extent, Debitum Network can be regarded as P2P lending platform, despite the fact that it only lends money to small and medium sized businesses, not individuals. In this regard, it is B2B (business to business) platform.

Property finance

Property finance type of funding is usually a secured business loan, where property (residential, business or property portfolio) is used as a collateral. You use the option when you want to borrow to buy property for a business or redevelop your existing property. You may also need to have a big deposit (up to 40 percent) for getting this type of loan. The benefit of that is that the bigger the deposit, the smaller the interest rates.

Invoice financing

In invoice financing a borrower uses his customers’ outstanding invoices to borrow money. A lender buys those invoices. In this way, an invoice of sales becomes a security for a loan. It has an advantage that you do not risk losing equity of your company. Small business companies often use this method of funding to get cash without waiting for the payment dates from their customers. The payment terms can be a drag as businesses often need cash fast for operational expense. Invoice financing allows you to transfer payment terms to your lender and you get the necessary money immediately. Invoice financing average return averages around 10-15% per year.

Asset based investing

Asset based lending is any kind of lending secured by an asset. When an asset is used as collateral, in case a borrower fails to repay the loan, the lender takes the asset from the borrower. This type of lending is typically used when a lender is not convinced that a company can pay the loan through its cash flows. Typically, the assets that are taken as collateral are: inventory, accounts receivable, machinery and equipment.

Register and start investing on Debitum Network platform

As you may see, there are plenty of ways to get funds for SMEs outside of traditional banking system. When Debitum Network platform launches in September, 2018 small businesses will have lots ways to get funding. There will be assets such as Factoring, Business loan, and a few more to choose from. Average expected returns for investors would be 7-11% per year and short term loans will vary from 2 weeks to 6 months. As platform is going to be global, any investor from around the World can invest in any asset with a flexible amount of capital, not necessarily full requested sum.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.