Tag: low risk assets

What is Invoice Financing?

What is Invoice Financing?

A lot of loans that are uploaded on Debitum Network belong to the invoice financing category. For those, who have studied finance/economy the term means something, for those who haven’t it may be confusing. Some investors seeing the term under loan type sub-section wonder what it is, whether it is safer than consumer loans, or simply how the funding of these types of loans works. This blog post is meant to answer the questions.

How does Invoice Financing work?

In invoice financing, a borrower uses his customers’ outstanding invoices to borrow money. A lender buys those invoices. In this way, an invoice for sales becomes security for a loan. It is great because business owners who use this way of borrowing, do not risk losing equity of their company. Small business companies often use this method of funding to get cash without having to wait for payment from their customers to arrive. The payment terms can be a drag as businesses often need cash fast for their operational expenses. Invoice financing allows you to transfer payment terms to your lender and you get the necessary money immediately. The lender has invoices as collateral to get payments from the customers of the borrower. Companies who choose to use services from an invoice financing company can get up to 90% of the value of their invoices.

Advantages of Invoice Financing

Improved cash flow

Day to day expenses, salaries, lease, and other financial obligations may significantly slow down a company. Fortunately, with invoice financing, businesses do not have to wait for 60, 90 or more days for their customers to pay for invoices. Funds can be available in a matter of 72 hours, sometimes even less. So, companies can carry on doing their day to day business operations or expand without experiencing a drag from delayed payments. With our partner and loan originator Factris, borrowers can usually get cash in under 24 hours.

Easier qualification requirements

Commercial banks reject 80% of applications for a loan from small businesses. Tons of paperwork, strict collateral requirements, time-consuming process are some of the things that put small companies in a deplorable situation while waiting for the approval for a loan. Invoice factoring solves the problem as most alternative lenders will be satisfied with proof of a stable client base and revenues exceeding 50,000 euros. These and a few more requirements help alternative lenders to screen potential borrowers and select creditworthy ones.

Quick access to funding

Timing is crucial in doing business. If a company has to wait for 90, 120 days for payments to arrive before they can move on with their plans, their hands are tied and possibilities to grow remain very limited. With invoice financing, funds can arrive in a couple of days and a company will be able to function unhindered due to available cash.

Credit line increases with a company’s revenues

In invoice financing company’s credit line depends on the value and number of invoices. With the increase of revenues, amounts of invoices can grow and the company can access greater amounts from lenders. This way of funding creates possibilities to get more funds than a company can ever get from a commercial bank.

Minimum collateral requirements

As invoices serve as collateral with most lenders, companies do not usually have to pledge assets as security to get funds. This opens a door for young companies who lack assets to back up deals to get funds, which is hardly ever possible with traditional banks.

Reduction of late payments and bad debts

Late payments and bad debts can stall any business from going forward. Debt collection can be a lengthy and expensive process, which may harm a business even more. Invoice discounting will help a company to avoid that because invoice financing company will do credit analysis of the company that owes money to a business. They will also know how to deal with non paying customers and how to get back the funds.

What is special about Invoice Financing assets on Debitum Network?

Now you know most of the advantages of invoice financing loans. What else could make invoice financing loans on Debitum Network more appealing for investment? Most of the loans on our platform are short-term. We ask brokers to give assets not for the full term of the loan, but in the final stages. The logic behind that is pretty simple. If a borrower took a loan for two years and was paying off the loan for a year and a half, it is highly likely that he will also pay off the remaining part of the loan. Thus, we prefer to take the asset with that half a year tern till the repayment date, rather than the full term loan for 2 years. These short-term loans are safer, enable fast turnover of investors’ funds, and offer a possibility to make compound interest.

Low-risk assets and attractive interest rates

The vast majority of assets have a buyback guarantee, which means that if the borrower is late with the repayment by more than 90 days, the loan (with outstanding principal and interest) will be bought by the broker who issued the loan. This makes investing in the assets very low risk. The other incentive is that in the invoice financing category we have top interest rates among other platforms. Consumer loans may have higher interest rates, but they are riskier as bigger number of defaults can decrease investors’ returns. Thus, an investor on Debitum Network will be offered low-risk assets with yet attractive interest rates.

Top asset of the week

The top asset for this week comes from our partner and loan originator Factris. The borrowing company specializes in wholesale of hardware equipment, it has more than 4.1 million EUR in revenues, employs more than 25 people, and has been in business for more than 21 years. Sounds good enough? Check out the asset and if you like what you see, you can invest right away.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

A balance between risk and return in investing

A balance between risk and return in investing:

Whether you are a conservative, moderate or aggressive investor you will have to manage risk and try to achieve as high returns as possible without compromising your risk management principles. A smart investor does not have to pursue one and neglect the other. It is possible to have both: manageable risk and above-average returns. One has to find the assets that carry very little risk and has good and sustainable average returns. Let’s try to figure out how to achieve the balance of risk/reward ratio and what assets would be best for investment to meet the ratio.

Risk/return tradeoff

Risk/return tradeoff is a principle that links high risks to high returns and low risks to low returns. In other words, the higher the expected return, the higher the risks an investor will have to take to achieve it. And vice versa, the lower the expected return, the lower the risks an investor will have to take to achieve it.

High-risk assets include equities, commodities, high-yield bonds, real estate, penny stocks, currencies, and cryptocurrencies. The value of these undergoes strong volatility as they may increase/decrease in value more than 20%-50% within a short period of time.

If an investor has a big portfolio with a large variety of assets inside, and only a small percentage of high-risk assets (penny stocks, exotic currency pair, or a volatile stock) those do not cause major threat for the whole portfolio as the other assets will level off the risk that may arise to those few assets in the basket. On the other hand, a lot of assets that are highly volatile and risky in nature may cause significant threats to the whole portfolio. Only well-experienced investors/traders can carry out these kinds of investments/trades by minimizing their losses when the investments turn south or maximizing profits when the investments work out well.

The chart from Netflix (NFLX) company proves how volatile these high-risk assets can be.

Source: investing.com

On the 1st of January, 2018 the price of one share of Netflix was 195.42 (US dollars). In six and a half months, it rose to 423.21 (US dollar) – a rise of 116%. This is spectacular growth! However, within the next 5 and a half months, the price of the stock fell to 231.23 (US dollars) – a fall of 45.4%. And then, within the next 6 months, it rose again from 231.23 (US dollars) to 385.99 (US dollars) – a rise of 66.9%. Due to such high volatility, both profits and losses investing in the security could be great. Unfortunately, only investors/speculators with huge risk tolerance could withstand such sharp fluctuations in their portfolio.

The safest assets

Low-risk assets have a low probability of default (going bankrupt/completely losing value) and consequently, the profits investing in the assets will be below average. Low-risk assets include Cash Investments: (savings accounts, money markets’ accounts, and certificates of deposit (CD), U.S. Savings Bonds, U.S. Treasury bills, German bonds (other bonds with the lowest risk rating). Conservative investors who are very much risk-averse tend to invest in those and thus increase their capital bit by bit.

Investing in low-risk assets may cause you to lose money!

However, the most recent event in the financial markets proved that some of the safest assets have carried very little or no return at all. 10-year German bonds is the case of that.

Source: investing.com

Looking at the chart one may see that in July of 2016, German 10 bonds slipped into negative territory and had a negative interest of – 0.20%. It means you have to pay extra to hold the investments. The same happened at the end of March 2019, when the interest rate for the bonds slipped into negative territory again, and have stayed there since then. It is worthwhile to invest in these, safest assets? To tell the truth, it beats the purpose of investing as you hold the safest instruments that cause you to lose money. With the inflation at 2.2% (in Europe) and 4.9% (in the world), it does not make sense to invest in these types of safe assets at all as you would be slowly but surely bleeding your capital to the German government for the privilege of holding ‘safe’ investments.

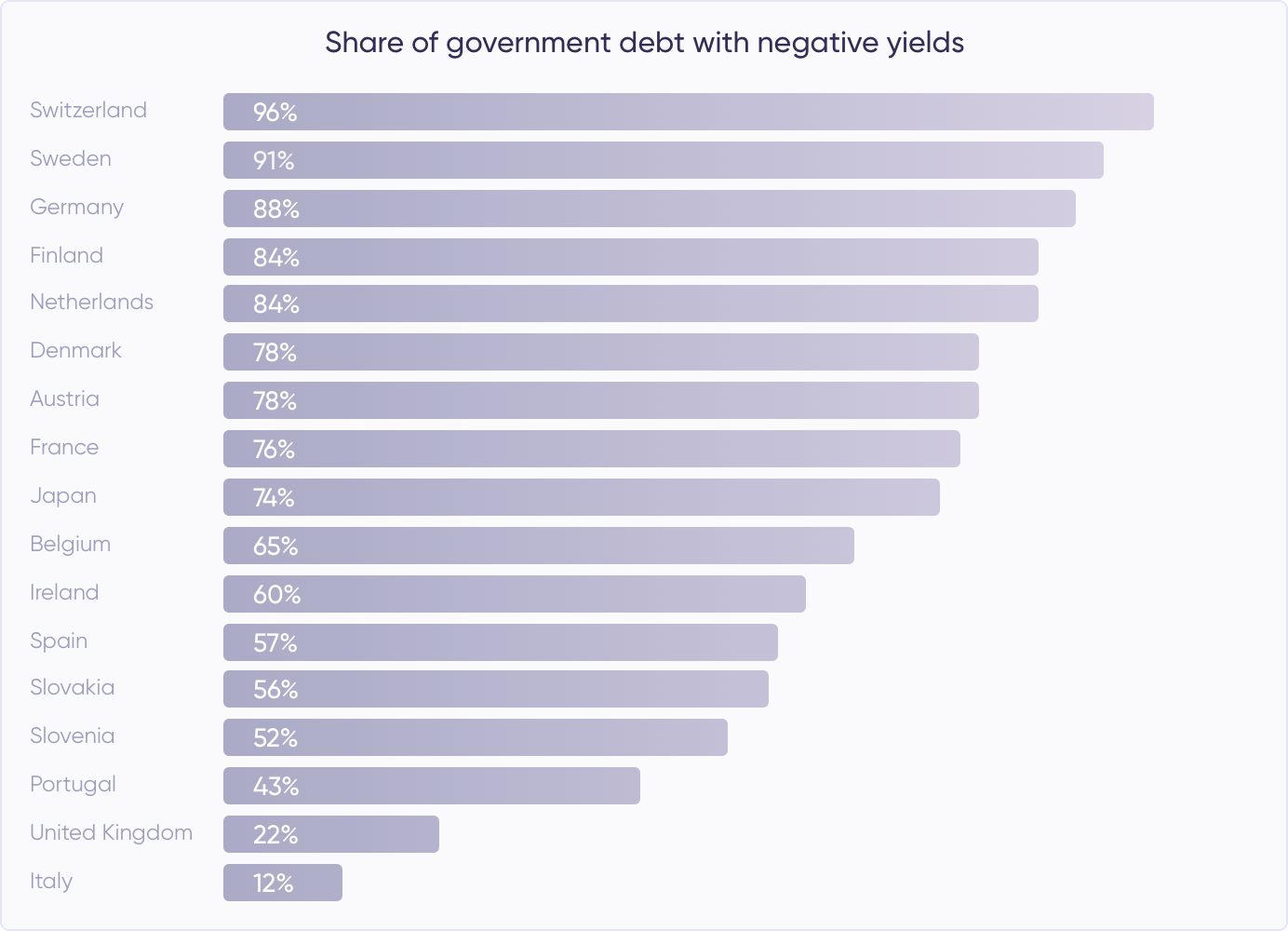

More than $12 trillion worth of government bonds have a negative yield now!

German bonds are not an exception. More than 16 governments now offer a negative yield to the holders of their bonds. Swedish 10 year bonds, briefly, slipped into negative territory for the first time in the middle of June 2019. Even the French government 10 year bonds fell below zero for the first time in history at the beginning of July 2019. With ECB (European Central Bank) hinting at the possibility of cutting interest rates and even restarting its’ quantitative easing program, the size of government bonds with a negative yield may surge. The chart below tells it all. 96% of all the bonds released by Switzerland have a negative yield!

Source: theatlas.com

Choosing “the golden middle”: low risk and above-average returns

One does not have to go to the opposite extremes of managing risk/reward ratio. Risking a lot to gain a lot, or staying safe and making nothing are not the only options on how to manage risk and make money. An investor can keep the upside and reduce the downside. There is the golden middle of managing risk/reward ratio, and make investments that carry very low risk and offer above-average returns.

The assets uploaded on Debitum Network platform fit in the category. How come? Each asset before it is uploaded is checked by an independent risk assessor (our partners risk assessors: Scorify, Crediweb, Creditinfo, Creditreform) and assigned a credit score that shows the probability of default of a business (that borrows) within the next 12 months. The vast majority of assets have B-, B+, or B- score, which means that the likelihood of a default of that specific business is extremely low.

Most of the assets (except one), have a buyback guarantee. It means that if the borrower is late with the repayment by more than 90 days, the broker who issued that specific loan will have to buy it back with the outstanding principal and interest. The guarantee radically improves the safety of investors’ funds who invest in the assets on the platform. In a period of 10 months, there have been a few assets who were bought back and investors got every cent they were due (outstanding principal and interest). These two things make the assets on our platform low risk.

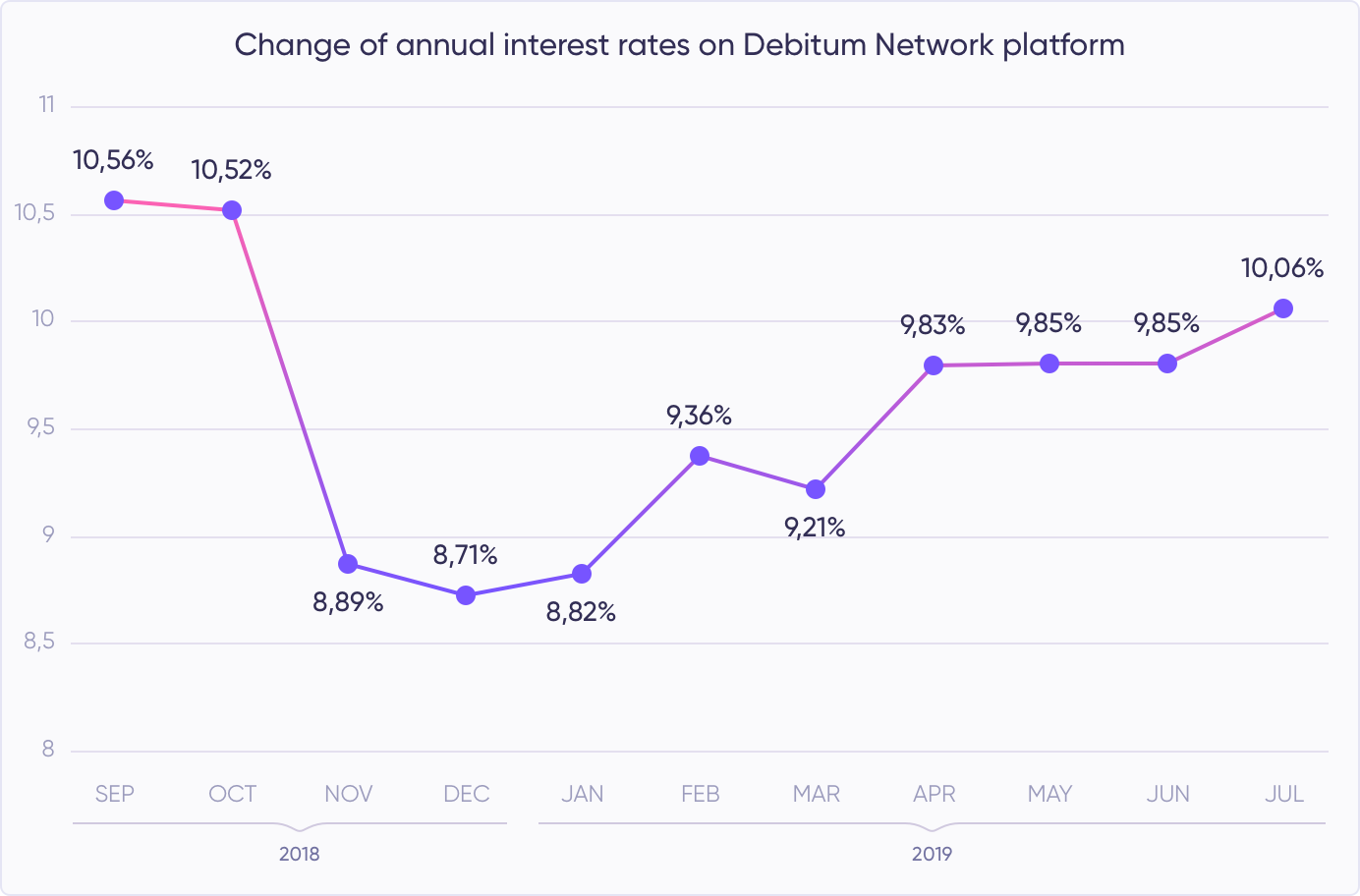

On the other hand, the interest rates of the assets are quite attractive in comparison to other traditional and safe investment options. As of now, a Lifetime Invested Interest Rate on Debitum Network platform is 10.13%. Taking into account, the level of safety of the assets and average annual inflation around the world, it is quite attractive and a fair deal to anyone who seeks above-average returns and low-risk assets for investments. With more loan originators coming to our platform, interest rates will rise and the investors will get even better returns without increased risk.

If you want to invest into balanced risk/reward ratio assets, we would recommend to register on Debitum Network platform and start investing. The minimum deposit is 50 euros, the minimum investment amount is just 10 euros. Registration is free and if you do not like it, you can leave anytime you want. We have selected a special asset for you. Take a look and if you like what you see, you can register and invest right away. Check it out.

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

Prosperitu joins Alternative Financial Services Association in Latvia

Prosperitu joins Alternative Financial Services Association in Latvia

We are happy to announce that Debitum Network platform operator ‘SIA Prosperitu’, established in the Republic of Latvia, has become a member of Latvian Non-bank association (Alternative Financial Services Association).

“To be a part of the association is another opportunity to upgrade our knowledge and offer new opportunities to our partners, investors and loan originators. Prosperitu is going to take part and give their impact working on P2P law project with other Non-bank association members” told us the director of Prosperitu Martins Perkons. For Debitum Network this also means being acknowledged as a notable player in the field of alternative finance and P2P online lending.

The mission of the association

Alternative Financial Services Association in Latvia unites providers of financial services operating outside the banking sector. Most of the members belong to financial technology or FinTech companies.

The mission of the association is the creation of a reliable and responsible sectoral practice, aimed at long-term cooperation and assessed positively by consumers and the market monitoring institutions, at the same time respecting the opportunities provided by the alternative financial services for free and ensured the development of every individual and society.

Members of the association

Members of the association come from the alternative finance industry and the following areas: leasing services, non-bank mortgages, online consumer credits, and peer-to-peer lending platforms. A lot of famous names in the P2P lending industry are members of the association such as: Mintos, Twino, or Robocash, and from now on Debitum Network is among the recognized players in P2P lending too.

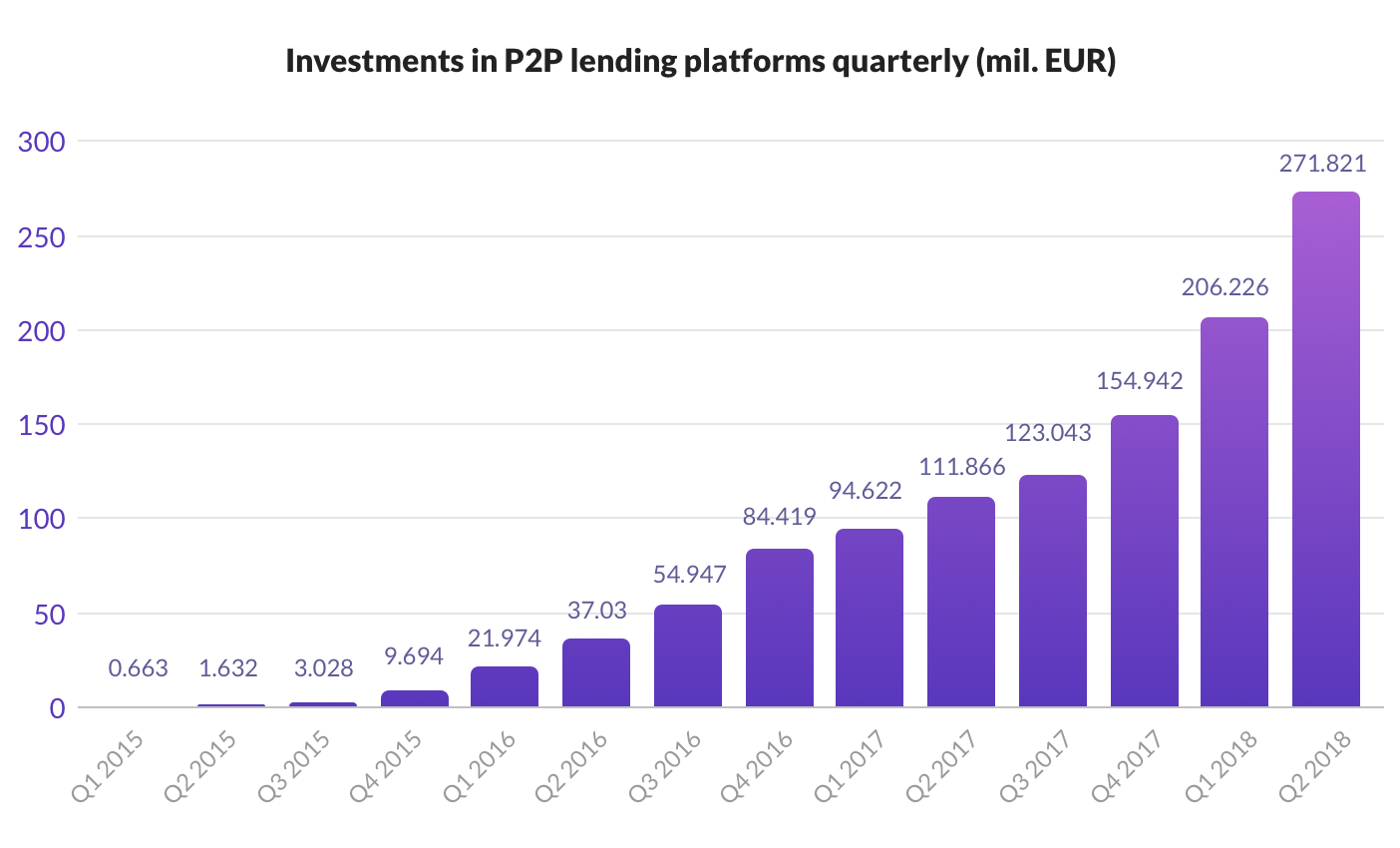

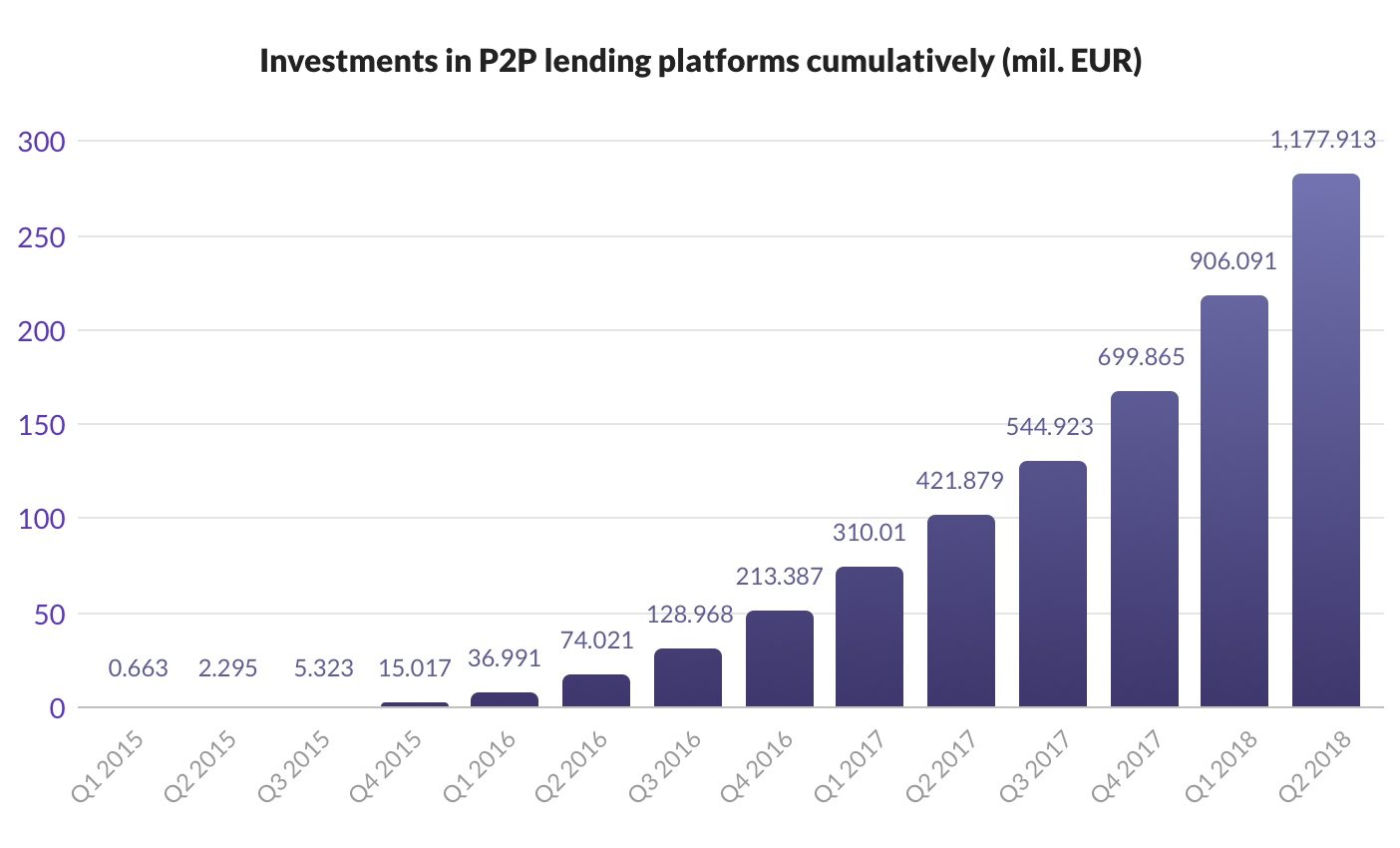

Online lending is a relatively new industry but statistics show that the interest and investments on P2P platforms have been growing by leaps and bounds in the recent years confirming we are in a competitive market with lots of opportunities ahead. Just take a look at the charts below.

Interest in Debitum Network platform on the rise

Interest in alternative investments will likely continue rising as interest rates in Europe remain close to zero. Debitum Network platform got real traction last year with multiple increases in the number of investors and investments month after month. This is likely to continue as interest rates for the assets vary from 7.5% to 11.5%, which is way above commercial banks or other traditional options of investments may offer. Just the fact should be a good incentive to join our platform and start investing.

Another incentive is that the assets are very low risk as all of them have guarantees: a buyback guarantee (it means that if the borrower is late with the repayment by more than 90 days, the loan originator will have to buy back the loan with outstanding principal and interest), collateral of physical assets (equipment, cars, warehouses and etc.) or a personal guarantee from the owners of the company that borrows. Having all of the above in mind, wouldn’t you like to try investing with us?

Disclaimer: Investments in financial products are subject to market risk and any investment should only be done with risk capital. The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.